Myself

Myself My

My My Income

My Income

Article on: Life Insurance for Domestic Partner

Can I buy Domestic Partnership Insurance?

Yes. However, we will review here first the legality for a domestic partnership actually having Life Insurance. Then the various different types of domestic partnership for insurance that are available, from leading UK Life Insurers.

We will look at 3 different types:- Domestic Married Partnership, Unmarried Domestic Partnership, Same Sex Domestic Partnership

What’s a Domestic Partnership?

What’s a domestic partnership? Well in this article domestic partnership def can mean

- official civil domestic partner

- someone you are actually married to

- you live as domestic partnership (but not legally married to them)

- Or live with as if you are both civil partners (but no legal union with them)

As a civil partnership is a formal arrangement that gives a domestic partnership the same legal status as a married partnership.

Plenty of domestic partnerships may assume that if they have both lived together for a certain period of time, perhaps share bringing up children, step children or a mortgage, then they may all have the same legal & financial rights as married couples or civil partnerships.

However in the UK, if any relationships end or their domestic partner dies, people can often find themselves in a difficult financial situation (especially if they have not made a valid will).

Domestic Partner for Insurance & Insurable Interest?

Insurable interest means that ‘you could be adversely affected financially (not emotionally) if your domestic partner, who you are insured with died’.

The reasoning behind insurable interest, is so that the death of an insured person may not create personal financial gain (rather than loss) for a policyholder.

So, Yes you can take out a Life Insurance for domestic partner – but as mentioned rules state there must be an ‘insurable interest’ between the 2 parties involved.

Domestic Partner on Insurance | 3 Examples

Let’s look at 3 example cases in 2026. The first few, where taking out a insurance domestic partnership life policy is valid. Then, lastly an example where it probably isn’t.

Example 1: As a new same sex domestic partnership, you & your partner have not yet entered a legal civil partnership, but have taken out a new joint £225,000 mortgage together. You both want to arrange a joint £225,000 mortgage life insurance policy to help cover this joint £225,000 mortgage debt.

The reason being, if one domestic partner died first, there would now be a £225,000 financial debt that would be passed onto the other domestic partner, as you were held jointly liable.

Under the laws of insurable interest, both of you could be adversely affected financially if one died re the mortgage debt. The survivor (who may also not be the main breadwinner), could then be in financial trouble.

Also, both domestic partners must consent to this arrangement. You can’t take out a life insurance (online or not) without either knowledge, whether it is joint policy or single life.

Example 2: You are a young unmarried domestic partnership, renting a property and have just had a new baby together. The young mother is currently on maternity leave but hopes to go back to work part time afterwards.

Because of your new baby, you are now both looking to take out one joint life domestic partnership insurance policy. You would prefer this, rather than maybe the other option. being unmarried, to take out instead 2 x separate plans.

Under the laws of insurable interest, both of you could be adversely affected financially if either of the domestic partnership insured died. The survivor (who may also not be the main breadwinner) along with your new baby, could be in financial trouble.

Example 3: You are a same sex domestic partnership, both who still each live separately at your own parent’s homes. You have been together for over a year & are now thinking of entering into a civil partnership.

Once registered, you would look to both rent a property together. Instead, you have currently each started to save money for the rental deposit anyway. You are looking to take out a joint life insurance policy as a declaration of domestic partnership, as you both would be devastated if the other died, so enquire about taking out domestic partnership insurance lifecover.

At this stage, you would NOT be adversely affected financially (but certainly emotionally affected) if either who you are insured with died. Technically, right now, you should not be taking out a joint life insurance policy. Being young anyway, life insurance should probably not be a number 1 priority yet (maybe critical illness that includes some lifecover or income protection insurance instead) but your situation can be reviewed. Your circumstances may change.

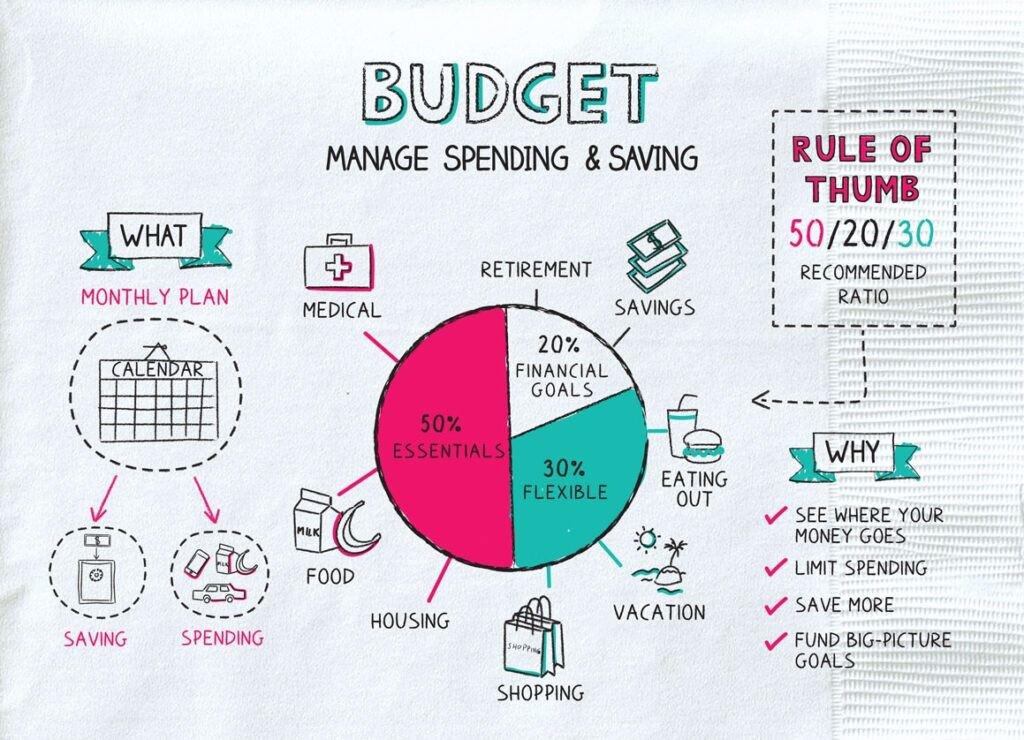

Financial Planning for a New Domestic Partnership

- Organise & Record your Domestic Partnership Finances

- Prepare a strict Monthly Budget

- What benefits does your work employment provide

- Only consider joint bank accounts if the time feels right

- Check out any available State Benefits if on low incomes

- Setup tax efficient savings plans & pensions

- Budget for Life Insurance, Critical Illness, Income Protection

So what do you need insurance for domestic partner policy for? Here are some typical examples.

- You are going to have a baby or adopt

- In a civil partnership

- Repay joint debts & loans

- Cover joint monthly rent & ongoing joint bills

- Insure new joint mortgage & bills

Note: You don’t have to take out a joint life policy at this stage. You could consider 2 x seperate plans instead. The best time to take out any domestic partnership for insurance cover, is when you are both fit and healthy. So consider also life cover and critical illness plus income protection.

2 main types of Life Cover

- Term Insurance

- Whole of Life Cover

Term insurance is a specific type of cover that pays out a cash sum BUT usually only if one of you died during the time your policy runs for.

This sum for death insurance is paid out tax free on claim and also usually has no cash in surrender values. This means that there is no investment savings element.

The term policy can be chosen as life insurance level term cover. The premiums & cover remains level or the same through out the whole term.

Or, if worried about rising costs post pandemic 2020’s, then consider instead term life cover index linked. The premiums & life cover will increase yearly to offset inflation.

NOTE: You can take out term life insurance that lasts up to age 90. However, the longer the term life policy runs, then the more expensive it is ie; you are more likely to claim on the policy before age 89, than before age 49?

As a general rule of thumb, a life policy for a 40 years term, maybe more than double the cost than a policy for 20 years.

There are several sub types of term life cover – either being paid out as Lump Sums or Family Income Benefits options. They can typically protect the needs for either family or mortgages ie; you can take out more than 1 policy.

- Level Term > Family

- Increasing > Family

- Decreasing > Mortgages

- Income > Family

Whole of life cover as the name implies continues the whole of life ie; whenever the insured person dies, stops paying premiums, or cashes in early. It tends to be generally taken out by older people.

So it will pay out a lump sum upon death, tax free on claim, to your family whenever you die eg; died age 190. This is unlike term life insurance, which only pays out if you died during the set term the policy runs for.

Generally whole life cover plans are much more expensive than term cover, as they offer much less cover pound for pound, as it will payout. Consider carefully if you really do need life cover beyond age 90?

How much Domestic Partnership Insurance?

As Life Insurance Brokers in an ideal world – we suggest this simple formula.

- LUMP SUM > Repay any mortgage & debts, cover funeral costs

- INCOME > Help cover your monthly bills

- LUMP SUM > Back up for holidays, education, emergencies

Martin Lewis Best Life Insurance formula is to aim to cover 10 x the Annual Income of the Highest Earner or Main Breadwinner until any kids have finished full-time education.

Using that principle, if you earned £28,000pa gross, Martin says you should maybe consider insuring yourself (after any mortgage, loans, credit card debts are repaid) for £280,000 life insurance (ie; 10 x the annual gross income).

Interestingly, he simply recommends insuring your gross income of £28,000pa – but not net after tax income in this Martin Lewis 10 x rule domestic partnership insurance example.

Following on from this simple Martin Lewis example formula above, if you then worked for the next 36 years until state retirement, you could potentially earn over £1 million gross ie; £28,000pa x 36 years = £1 million [or more with any future inflationary wage rises].

As such, unlike the 10 x £28,000 gross salary life insurance example above – you could instead protect each other with either;

- Income = £2,333pm or £28,000pa family income benefit lifecover policy

- Lump sum = £1 million level term life insurance policy [if invested @2.8% = £25,000pa]

- Or a mixture of the 2 policy types over the next 36 years – all dependant on your family circumstances

Neither takes into account repaying any mortgages, loans or debts.

- You can decide wether you want the cover to be level or inflation linked

- 2 x seperate plans | or Joint life insurance 1’st claim

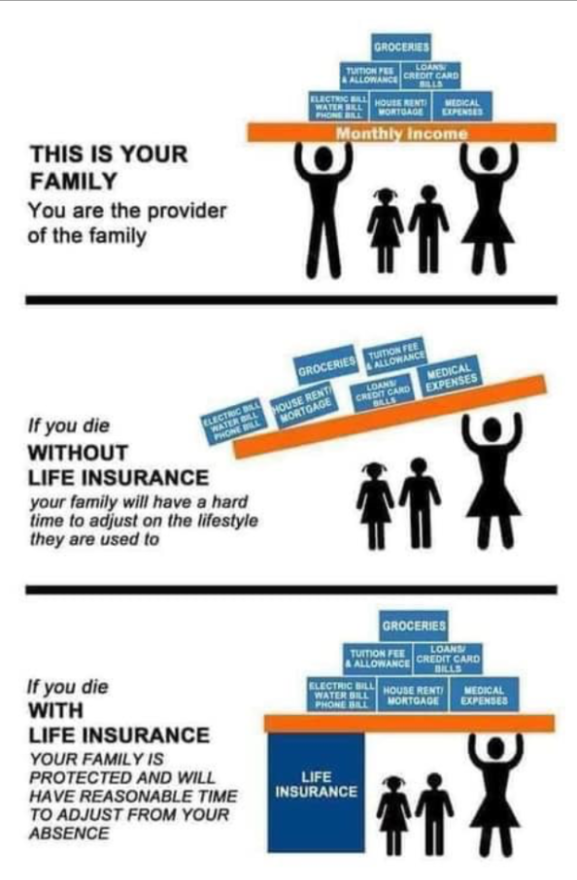

Apart from losing a loved one, this real hidden income threat is what could be lost if one of a partnerships main breadwinner died prematurely.

How much does this all cost?

- Often average prices can start from as low as £5pm (for 1 product)

- But your monthly or annual cost will vary in a few ways

- Premiums will depend on your ages, health, lifestyle, amount of cover, policy term and type

- It could be you are offered standard costs or have to pay abit extra insurance price risk

- Any paid for extra features (like critical illness) you want will also affect the cost

- Is the cover to remain level or increasing to offset inflation ?

- Remember cheaper here, doesn’t necessarily mean better

- Joint domestic partners insurance cover is cheaper than 2 x seperate plans but will only pay out once

- Some insurers may also give you a discounted price if buying 2 x individual policies

- Is partner life insurance deductible? No is the answer for personal cover

Add Critical Illness Cover?

Critical Illness insurance is a policy that pays out a tax-free sum to protect you (or domestic partner) should you become critically ill during the policy term. The 3 main claims in today’s world, relate to types of cancer, heart disease & stroke. The chances of a claim are fairly high in working lifetime.![]() This additional critical illness benefit is well worth considering. However, if this is added to a joint policy, it means upon the 1’st to claim, the whole policy may then end.

This additional critical illness benefit is well worth considering. However, if this is added to a joint policy, it means upon the 1’st to claim, the whole policy may then end.

We recommend also that any individual partners Life Insurance policy is put into a Trust from outset (especially if you have not yet made a legal will, in a civil partnership).

This means simply when a ‘life policy is in trust’, the payouts could go direct to your intended beneficiaries and with potentially less complications, if you sadly died. Most life insurers provide free protection trust forms. Note: If you should ever split up, dependant on the type of trust used, it may require all the trustees to then agree to any changes made.

What is Civil Partnership in UK?

What is civil partnership in uk? It is a legally binding relationship which can be registered by 2 people who are committing to each other & are not related to each other.

Registering your civil partnership will give your domestic relationship legal recognition. This will give you added legal rights, as well as responsibilities.

Civil partnerships are available to both opposite-sex couples & same-sex couples.

To register a civil partnership, you & your domestic partner must sign a legal civil partnership document in front of at least 2 witnesses and a registrar.

In some situations, domestic partners who have not registered a civil partnership will have the same legal rights & responsibilities as those who have registered a civil partnership. This will be the case, for example, when working out your entitlement to welfare benefits and tax credits.

There are 2 main steps needed to register your domestic partnership now as a civil partnership.

1] Give notice of your intention to register

2] Actually register the civil partnership

Civil Partnership Insurance

The UK Marriage Equality Act gives same sex partners life insurance (wether male or female) the same rights as married heterosexual couples. However, it does not apply to anyone living with someone, but neither yet married (even if engaged) nor yet official legal civil partners.

Getting same sex life insurance therefore in the 2020’s, fortunately can be hopefully no different from standard life insurance rates. However, the rules of insurable interest still apply (as mentioned above).

Financially, if one of the partners died prematurely, could the survivor help then cover their ongoing bills & costs? The reasons for a life insurance couple policy could be….

- Repay joint debts & loans

- Cover joint monthly rent & ongoing bills

- Insure new joint mortgage & bills

Married Domestic Partnership Insurance

Part of the marriage ceremony vows can be legally stating… you will both stay together as a domestic partnership “Til Death Do Us Part”.

At some stage, once life has calmed down abit, you will both start discussing about having a family? Or joint financial products together eg; joint bank accounts, maybe joint savings, investments & mortgage.

Likewise, seeing as you both probably legally said these actual words at your wedding, about discussing again that dreadful word death. So, now is a good a time as any to also talk about life insurance. It could start by seeing an advert on TV, Website or Radio.

One of you maybe the main breadwinner & the other now a ‘stay at home mum’ or domestic partner for insurance. The main breadwinner may feel they should be the main one that’s insured as the other is not earning. This can be a big mistake especially if you have dependants, young or old.

But life cover can help ensure that you…

- Continue to live in your home

- Make ongoing mortgage or rental payments

- Plan for your future

So, the same way you just discussed joint bank accounts & savings, perhaps you should now discuss life insurance cover at a similar time. Ideally, we suggest you discuss this in the same ‘matter of fact’ manner. Remember, you probably said these exact words at your wedding.

Domestic Partners & Broker FAQ

Domestic Partnership Health Insurance

Domestic partnership health insurance can cover you and your partner under one joint policy. It may give you fast access to specialist treatment plus 24/7 advice and medical health support. You may pay a monthly subscription that covers the cost of any treatment either of you may need but for conditions that develop after your policy has begun.

Providing you and your partner both live at the same address, you can be covered under a joint domestic partnership health insurance policy.

If you currently live separately, some insurers may give you a discounted domestic partners insurance price, when compared to buying 2 x individual policies. Ask us for advice here.

Private Health Insurers may offer 2 types of domestic partnership health insurance plans

- Option is for those who are happy to be diagnosed by the NHS (plus any associated delays) but would like to receive treatment privately

- Instead get a private diagnosis, treatment and aftercare for all your eligible medical needs

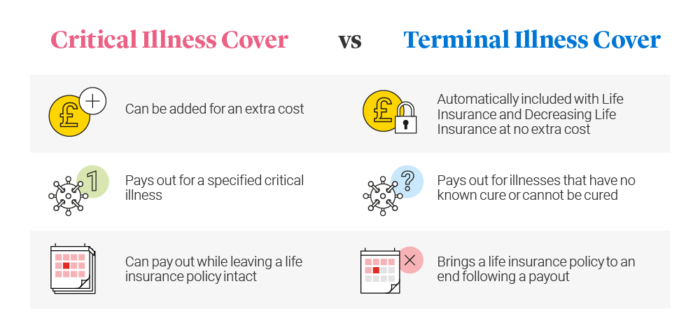

Critical Illness vs Terminal Illness Cover

Critical Illness is an underwritten insurance policy, that helps protect you if you are diagnosed critically ill (as specified by Insurers) during the policy term. The top 3 benefits most Uk Insurers cover are for types of cancer, heart disease & stroke* ABI.

It pays out a tax-free sum that you can use, however. To help repay the mortgage, cover monthly expenses, health-related costs, lost income while you recover (although income protection maybe a better longer term policy in that respect).

- Critical Illness as explained, may pay out claims crucially upon ‘diagnosis and survival of the specified illness’

- So Critical Illness means you may live, survive & claim

- Critical Illness cover may also provide some cover for your children

- Terminal Illness is often included for ‘free’ as part of a life cover

- It usually means a GP consultant has advised you could have less than 12 months to live ie; incurable illness

- Terminal Illness means you will not survive long term after a claim

- Once agreed by Insurers, they may then payout this policy death claim but in advance

- Note:lifecover and critical illness plans are often combined anyway

What does putting a Policy Into Trust mean?

- It tells the Insurance Company who you want to get the money if you sadly died

- Ensures it should go direct to you nominated beneficiaries via the trustees

- Putting your policy into ‘trust’ may also help to avoid probate delays & inheritance tax

- Without a trust the policy could fall back into your estate,This applies even if you have made a valid will

- Most Insurers do supply free a good range of generic life insurance trusts, ideal for many client situations

Importance of Disclosure & Claims?

All Insurers are in business to protect, insure & payout. Lifecover is therefore based on your full disclosure at the time you take the original policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying.

The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless manner when applying. If so, it may not payout ! eg; If you vape, then you must tell them you are still smoking or a familial history of blood pressure or cholesterol (even if it costs more).

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details.

They will then assess if your insurance claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers – not 100%).

What if health changes after starting a joint Domestic Partnership Insurance?

Any health or lifestyle changes since, usually does not void your existing joint life policy, if it wasn’t relevant at that time of initial underwritten insurance application. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your application what you initially disclosed to the Insurers, as this information then stands now and in the future. Please check your original T&C’s.

Domestic Partner Insurance – Conclusion

I hope that gives a brief background as to what is insurance for a domestic partner and why you should consider taking one out. Please check out & Compare Online Broker only deals here.

If family members are also dependant on you both as a domestic partnership, then you know it makes good sense ![]()

Article on ‘Domestic Partnership for Insurance’ by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women – we review many of the best Life Insurers selling Life Insurance in UK (inc NI)