Myself

Myself My

My My Income

My Income

Life Insurance what? We discuss what 2 main types of life insurance what you may want to get.

What Life Insurance Plans are best? We Compare Leading Uk Life Insurers. Deals from £5pm. Broker help

We will now look into what’s a life insurance policy re disclosure & what isn’t.

Definition of Insurance ie; ‘What’s a Life Insurance’?

We will now go onto to explain What is a Life Insurance and those legal implications for both parties involved.

The definition of insurance is best explained as a legally binding contract between an insurance company (insurer) and the policyholder (insured).

Under this contract the insurer promises to pay a specific sum of money (also known as “Sum Assured” or “Cover Amount”) to the insured individual’s family upon their death (or the insured, if terminal illness/critical illness is also included).

This amount is in exchange for a specific amount of premiums, being paid by the policyholder during the policy lifetime.

Life Insurance how does it work?

For the Insurers contract to be legally enforceable under their definition of insurance, the application must clearly & layout accurately all those Insurers questions & their policy terms.

The insured or policyholder in return, now needs to ‘honestly & fully disclose’ all their current & past health, lifestyle and any family risks.

Once done, the Insurance Company will underwrite the application. Based upon this risk assessment, the Insurer may then offer terms, which need to be accepted by both parties to proceed.

If accepted, the 2 parties then enter in this legal insurance contract which continues under the terms of the policy.

A contract is then validated via the premium amount or money you pay to the Insurer, in exchange for your policy cover. It can either be a regular monthly, annual or sometimes one-time payment and is usually paid by direct debit.

So when clients ask on life insurance how does it work …The contracts offered should be clear, fair and not misleading.

Life insurance how does it work in days gone by are different than today, due to modern banking methods & the internet.

In days gone by, a kindly Agent would come to collect the regular insurance premiums, often in cash, by visiting their customers. These old paper plans were also known as ‘penny policies’. They would regularly visit people, knocking on door to door, and stamping up their insurance premium receipt book each week, when they collected your regular premiums (after a chat and cup of tea & biscuit).

Key Facts

- Life Insurance explained as legally binding contracts, that pays a death benefit to the policyholder (or their estate) when the insured person dies

- For a policy to remain in force, the policyholder or owner must pay any premiums as requested

- When the insured dies, the Insurers will need a death certificate and will then investigate the validity of their claim

- Once approved, the policy holder’s estate, any named beneficiaries or trustees may receive the policy’s death benefit

What Life Insurance Cover?

Let’s discuss the Main types of Life Insurance What Is available in the UK marketplace today. We will look at What Life Insurance Cover deals could be best for situation.

We will now look at 4 different Options. Term life insurance what is level, increasing, decreasing or income cover types usually available.

‘Types of Insurance Life’ What Life Insurance Cover?

There are 2 main different types of what Life Insurance cover is available in the UK marketplace; Term Life Insurance & Whole of Life Assurance.

*Term Life Insurance what is?

Term insurance is a specific types of insurance life cover that pays out a cash sum BUT only if you die during the time your policy runs for.

This sum upon death is paid out tax free on claim and also usually has no cash in surrender values. This means that there is no investment savings element.

The policy can be chosen as term life insurance level cover. In this instance, both the premiums & cover remains level or the same through out the whole term.

Or, if worried about rising costs post pandemic 2020’s, then consider instead term life cover index linked. In this instance, both the premiums & life cover will increase yearly to offset inflation.

NOTE: You can take out term life insurance that lasts up to age 90. However, the longer the term life policy runs, then the more expensive it is ie; you are more likely to claim on the policy before age 89, than before age 49?

As a general rule of thumb, a life policy for a 40 years term, maybe more than double the cost than a policy for 20 years.

There are several sub types of term life cover – either being paid out as a lump sum or income. They can typically protect the needs for either families or mortgages ie; you can take out more than 1 policy.

- Level Cover > Families

- Increasing > Families

- Decreasing > Mortgages

- Income > Families

*Whole Life Insurance what is?

Whole of life cover as the name implies continues the whole of life ie; whenever the insured person dies, stops paying premiums, or cashes in early.

So it will pay out a lump sum upon death, tax free on claim, to your family whenever you die eg; age 190. Whole Life is unlike the above various types of insurance life term cover, which only pays out if you died during the ‘set term’ the policy runs for.

Generally, whole life insurance explained uk plans are much more expensive than term cover, as they offer much less cover pound for pound, as it will payout. Consider carefully if you really need life cover beyond age 90?

In conclusion, only use whole life insurance what is available to your family needs.

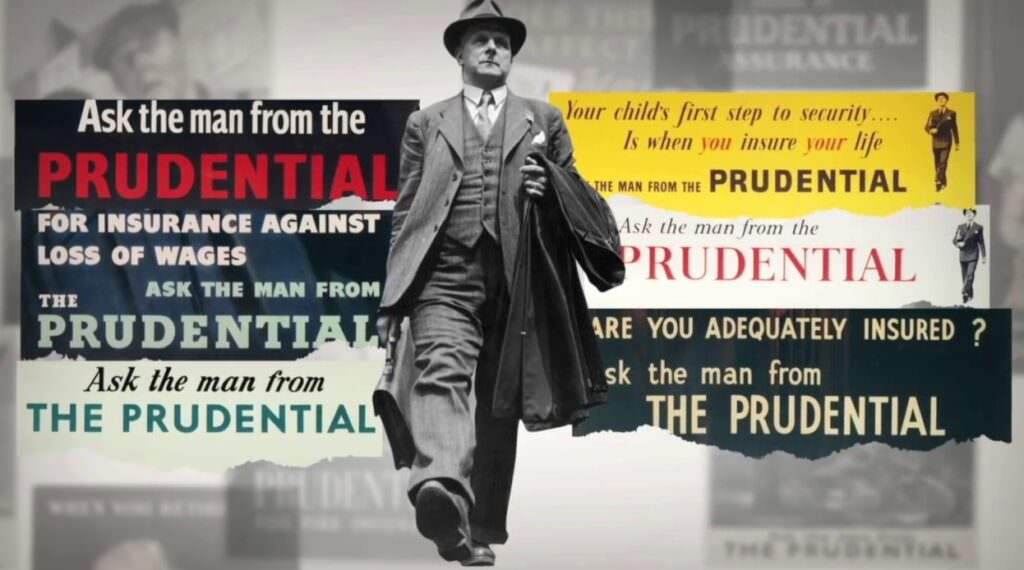

How do Life Insurance work?

The simple reality when explaining how do life insurance work, is at the worst possible time, it can help reduce the financial impact a persons death could have on their family or business.

It can help offer Peace of Mind ![]() at the worst possible time.

at the worst possible time.

- It can help repay a mortgage or loan debt.

- Alternatively it could help cover ongoing household bills, for parents childcare costs or rental payments.

- It can also be known as life cover, death insurance or referred to as life assurance (ie; whole of life insurance).

- You can choose the amount of cover you need or how long you need it for

- If you want the policy to be level or inflation proofed

- Whether you want a policy on single life, seperate lives or a joint life policy

- Paid out as a Lump sum or regular Income

Let’s now look into Life Insurance what do I need, and the amounts of life cover you should consider & for how long…

‘Life Insurance what do I need’?

When looking to what insurance cover do I need, then the Martin Lewis life insurance formula is 10 x Main breadwinner’s salary. Martin’s Money Saving Expert calculation is a basic rule of thumb guidance only.

Using that principle, if you earned £25,000pa gross, Martin says you should maybe consider insuring yourself (after any mortgage, loans & debts are fully repaid) for say £250,000 life insurance (ie; 10 x the annual gross income).

Following on from this simple Martin Lewis example formula above, if you then worked for the next 40 years until state retirement, you could potentially earn over £1 million gross ie; £25,000pa x 40 years = £1 million [or more with any future inflationary wage rises].

As such, unlike the 10 x £25,000 gross salary life insurance example above – you could instead protect your family with either;

- Income = £2,083pm or £25,000pa family income benefit lifecover policy

- Lump sums = £1 million level term life insurance policy [if invested @2.5% = £25,000pa]

- Or a mixture of the 2 policy types over the next 35 years – all dependant on your family circumstances.

Neither takes into account repaying any mortgages, loans or debts.

- You can decide wether you want the cover to be level or inflation linked

- Single plan | 2 x seperate plans | or Joint life insurance 1’st claim

However, as Financial Advisers we are not saying his ‘Money Saving Expert formula’ 10 x salary is therefore a 100% what a life insurance fits all cases scenario ie; not applicable for everyone’s own personal situation.

So, I would re-summarize Martin’s formula as Brokers & maybe suggest instead this simple formula.

- LUMP SUM > Repay any mortgage & debts, cover funeral costs

- INCOME > Help to cover your monthly bills

- LUMP SUM > Back up for holidays, education, emergencies

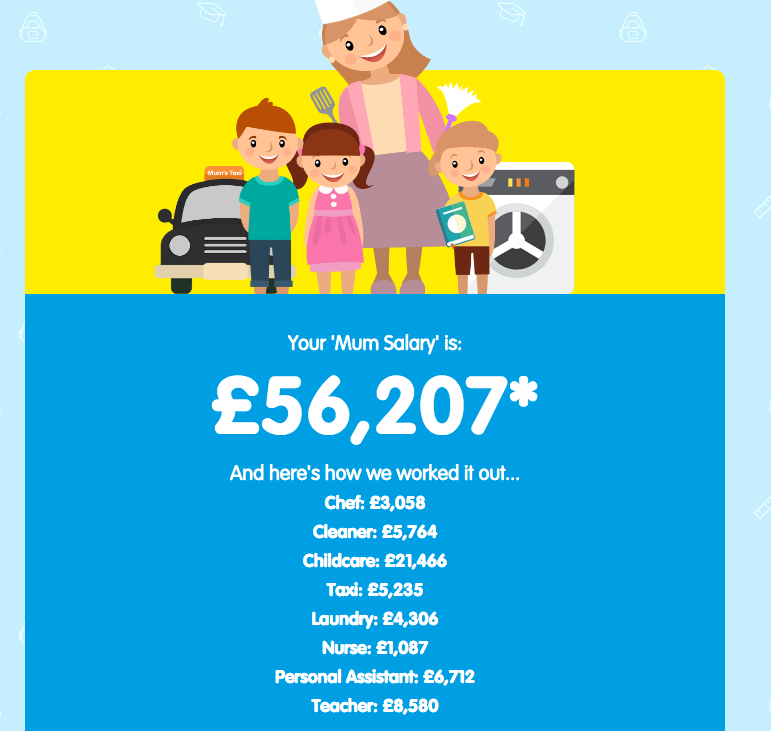

Example: How do you value cover for a ‘Stay at Home Mum’ if calculating women’s life insurance ie; What’s a ‘Mum Salary’ worth ? Sun Life Insurance came up with £56,207pa*

Apart from the grief of losing a loved one, a real hidden financial threat is what could be lost if that Key Family member (working or not) died prematurely.

Review your financial resilience?

Unsure if you now need a protection insurance policy? The following 5 key questions & in no particular order should help you assess your own families financial resilience.

- If you were unable to work, would your family be concerned about your ability to make any debt repayments on time e.g. loans, credit cards, car finance etc?

- How long could you continue to pay your mortgage/rent and other regular essential expenses if you lost your income?

- Would you and your families own lifestyle have to immediately change if you couldn’t work?

- Do you have any money left over for any savings at the end of the month?

- Would you find it difficult to pay any unexpected bills?

If, after thinking through these above scenarios, you do have concerns about your ability to pay any essential expenses and debts if you couldn’t work, then it is highly advisable to have a protection policy in place.

‘Is Life Insurance’ costly?

With rising monthly household bills & pressed family budgets in this Post Pandemic 2020’s, many people are naturally looking to save money where they can. This is understandable ![]()

What a Life Insurance Deal is good value? Well, we compare here online quotes from Leading UK Insurers with plans starting from £5pm.

- Monthly or annual premiums will vary in a few ways

- Gender no longer affects prices since 2012

- They will depend instead on your age, health, lifestyle, amount of cover, policy term and type

- It could be you are offered standard costs or have to pay an extra risk premium

- Any paid for extra feature you want will also affect the overall cost eg; lifecover and critical illness.

- Is the cover to remain level or increasing to offset inflation

To best explain life cover that is ideal to your own situation, we recommend you talk to a Professional Broker ![]()

‘What is a Life Insurance’ | Broker FAQ

What is Life Insured?

What is life insured = person insured on the life policy & relates to Insurable interest. This means that ‘you could be adversely affected financially (not emotionally) if your partner, who you are insured with died’.

The reasoning behind insurable interest, is so that the death of a life insured may not create personal financial gain (rather than loss) for a policyholder.

Example: As a young couple or (lives insured), you both take out a new joint £177,000 mortgage together. You then both arrange a joint £177,000 mortgage life insurance policy to help cover this joint £177,000 mortgage debt.

The reason being, if one of you sadly died first, there would now be a £177,000 financial debt that would be passed onto each other, as you were held jointly liable.

Under the laws of insurable interest, both life insured could be adversely affected financially if one died re this mortgage debt. The surviving life insured (who may also not be the main breadwinner), could then be in financial trouble.

Also, both parties must consent to this arrangement. You can’t take out a life policy for this (online or not) without the other’s knowledge, whether it is joint policy or single life.

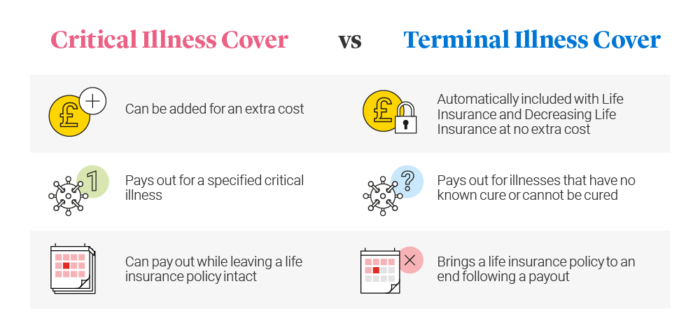

Critical Illness vs Terminal Illness Cover

Critical Illness is a special insurance policy that helps protect you if you are diagnosed critically ill (as specified by Insurers) during the policy term. The top 3 benefits most Uk Insurers cover are for types of cancer, heart disease & stroke* ABI.

It pays out a tax-free lump sum that you can use, however. To help repay the mortgage? cover monthly expenses? health-related costs? or toward lost income while you recover (although income protection maybe a better longer term policy in that respect).

- Critical Illness as explained, may pay out claims crucially upon diagnosis and survival of the specified illness

- So Critical Illness means you may live, survive & claim.

- Critical Illness cover may also provide some cover for your children

- Terminal Illness is often included for ‘free’ as part of a life cover.

- It usually means a GP consultant has advised you could have less than 12 months to live

- Terminal Illness means you will not survive long term after a claim

- Once agreed by Insurers, they may then payout this policy death claim but in advance

- Note: critical illness and life cover plans are often combined anyway

What does putting a Policy Into Trust mean?

- It tells the Insurance Company who you want to get the money if you sadly died & who will deal with the paperwork.

- Putting your policy into ‘trust’ may also help to avoid probate delays & Inheritance Tax IHT

- Without a suitable trust the lump sums policy could fall back into your estate

- This ensures it should go direct to you nominated beneficiaries via the trustees

- This applies even if you have made a valid up to date uk will

- Most Insurers do supply free a good range of generic life protection trusts, ideal for many client situations

Importance of Disclosure & Claims?

All Insurers are in business to protect, insure & payout. Lifecover is therefore based on your full disclosure at the time you take the original policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying.

The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless manner when applying. If so, it may not payout ! eg; If you vape, then you must tell them you are smoker (even if it costs more).

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details.

They will then assess if your insurance claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers – not 100%).

What if my health or lifestyle changes after I have taken the Life policy out?

Any health or lifestyle changes since, usually does not void your existing life policy, if it wasn’t relevant at that time of initial underwritten insurance application eg; diagnosed high cholesterol or heart disease. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your application what you initially disclosed to the Insurers, as this information then stands now and in the future. Please check your original T&C’s.

Is Life Insurance a Waste of Money?

As brokers below are collectively some of the top 10 reasons (or excuses) given to us over the years why some people think life insurance is a waste of money, and in no particular order;

- Life Insurance Companies don’t payout

- Cannot afford it – Too expensive

- I don’t believe in Life Insurance

- The ‘Other Half’ works. They could Remarry or cope

- No intention of dying just yet. Not made a will either

- I am probably uninsurable anyway (then laughs)

- We have some Savings so don’t need any thank you

- I am young, free & single, no debts or dependants

- Life Insurance has no benefit to me if I die

- The Government will help provide

You may insure your car, your home, your pet, your mobile phone & gadgets …BUT why not more importantly properly insure the person and family who pays all those bills ‘YOU

Conclusion

This gives a brief background for the definition of insurance as to “What’s a Life Insurance” policy and also why you should take one out. Please check out & Compare Online Broker only deals here.

If family members are dependant on you, then you know it makes good financial & emotional sense ![]()

‘What’s a Life Insurance’ Article by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women – we review many of the best brands selling Life Insurance in UK (inc NI)

Case Studies

Check out these helpful Insurance Case Studies below…

is life insurance

‘Critical Illness Definitions’ | Case Study: Gordon & Sarah

Compare Broker Critical Illness Definitions & Life Insurance Deals: August 2026 > Critical Illness Definitions explained. Article on: ‘Critical Illness Definitions’ Background: ‘Critical Illness Definitions’ Case Study Critical Illness Definitions Typical Case Study: Gordon is age 32, an Architect on £35,000pa salary. He is married to wife Sarah age 30, a part time Teacher on […]

‘Joint Names Insurance’ | Case Study: Donna & Dave

Compare Broker Joint Names Insurance Deals: August 2026 > ‘joint names insurance’ case study Background: Joint Names Life Insurance | Case Study: Joint names insurance typical case study: Dave is age 47, a self employed Builder on £40,000pa salary. His partner Donna is age 43 and she owns a hairdressers on £28,000pa. The unmarried couple […]

‘Over 50 Life Insurance Comparison’ Case Study | Mike & Sue

Broker Over 50 Life Insurance Comparison Deals: August 2026 > ‘Over 50 Life Insurance Comparison’ Case Study’ Over 50 Life Insurance Comparison: Background | Typical Case Study Over 50 Life Insurance Comparison Case Study: Mike is age 73 and a retired COOP Milkman on £12,250pa pension. His wife Sue is age 70, a retired clerk […]

‘Whole Life Insurance Explained’ | Case Study: Phil & Jen

Compare Whole Life Insurance Explained Broker Deals August 2026> whole of life insurance explained ‘Whole of Life Insurance Explained’ Background: ‘Whole of Life Insurance Explained’ | Typical Case Study Philip & Jennifer have been married for over 50 years. Phil is age 76, a retired GP on £58,000pa pension and his wife Jen age 72 […]

Income Protection Case Study | Jeffrey

Compare Broker Income Protection Insurance Deals: August 2026 > Income Protection Case Study: Jeffrey Income Protection Case Study Jeffrey Background: Income Protection | Typical Case Study Income Protection Case Study: Jeffrey is age 38, a Chemist, non smoker & earns £48,000pa salary (around £3,000pm after tax). He is married with 2 children & the main […]

Mortgage Protection Case Study | Alexandra

Compare Broker Mortgage Protection Insurance Deals: August 2026 > Background: Mortgage Protection | Typical Case Study Mortgage Protection Case Study: Alexandra is age 38, a Business Consultant on £45,000pa salary. She is divorced & has 2 children under age 10. Alexandra is due to sell her existing property & exchange contracts shortly on a £235,000 […]