Myself

Myself My

My My Income

My Income

'WHOLE OF MARKET MORTGAGE BROKERS'

England | Wales | Scotland | Northern Ireland

150+ UK Lenders >>

150+ UK Lenders >>

Article on: Whole of the Market Mortgage Brokers in the UK and England

What are 'Whole of Market Mortgage Brokers'?

People often ask us What are Whole of Market Mortgage Brokers? It means, we are able to access (as the name implies) the 'whole of market' to help get your ideal mortgage.

So we have got it covered from main High Street Lenders, Regional Building Societies to Specialist Lenders. Then also find you some whole of market Mortgage Broker only Lender deals.

This also means you can get professional advice via our whole of market mortgage broker near me services, which could potentially save you a lot of time, stress & money.

These are just some of the typical mortgage finance areas as a 'whole of the market mortgage broker' we can help assist you...

Whole of the Market Mortgage Brokers (NOT a Panel)

When searching online for 'whole of market mortgage brokers' it can get confusing. Some mortgage consultants you maybe speaking to, may state that they can access a wide range of selected mortgage products.

This can sound impressive BUT the UK market actually divides into 3 key areas here.

- 'Mortgage Broker Whole of Market'

- Mortgage Brokers - off a Selected Panel

- Direct to Lender only

Some 'UK mortgage brokers' may only be able to recommend a mortgage that are available from a selected 'panel' of lenders. So, they are NOT a whole of the market mortgage broker like we are.

How many mortgage brokers are there in the UK? Well, there are reportedly over 5,500+ so you should be able to access a 'mortgage broker near me'. The question is do they operate as whole of market or selected panel?

For example, many high street estate agents uk mortgages broker advertise they do operate this way via a selected mortgage panel eg; William H Brown, Countrywide, Reeds Rains, Spicehaart etc;

Meanwhile, remember if you go for a direct only mortgage, or just speak to the bank & building society adviser (not a broker), they can usually only recommend their own product range. eg; Nat West bank, Barclays bank, Lloyds bank, Coop bank etc; rather than speaking to a whole of market mortgage advisor.

Let's now look at the key differences between a whole market mortgage broker v bank...

'Mortgage Broker v Bank' | Pros & Cons

So....Why should you consider using a UK Mortgage Broker v Bank?

Well, the biggest debt most people have today is often their mortgage. So, for most people it must make good financial sense to get the 'best deals' on their biggest debt?

That's why people seek advice from trusted people like Martin Lewis on Mortgages, whether that is a first time mortgage, remortgage, 2nd mortgage, home mover mortgage or equity release.

Money Saving Expert (MSE) often also recommends you go talk to a uk mortgage broker for all market if unsure what best to do...

MSE says "by using one, you swiftly cover a huge slew of lenders, and get added clout with them to ease your acceptance as well as an extra layer of protection if things go wrong".

Why? well getting a mortgage is up there supposedly in one of life's most stressful situations* (according to research by habito & others).

As such, is it good business practise to seek best professional advice from independent mortgage brokers MSE thinks so.

So Martin Lewis positively comments here that 💯 "100% a good qualified Mortgage Broker is worth their weight in gold"

So whether you are looking for mortgage brokers near me like independent mortgage brokers in brighton or mortgage brokers in peterborough - we hopefully can still help you.

Whole Market Mortgage Broker in UK

'Why use Mortgage Broker'?

Well, lets now have an overview at what does a Mortgage Broker in UK generally do?

Their daily job role is to research the mortgage marketplace available for their clients, based upon their personal financial situation & then apply for the best mortgage on their behalf.

A CEMAP qualified brokers mortgage experience should help save you both the time & stress, by telling you which mortgage lenders are most likely to accept you.

They will then use their expertise to improve your chances of successful application to the lender.

A whole of the market mortgage advisor can then speed up the process by helping do all of that time consuming paperwork & those numerous telephone calls to help get you your ideal mortgage.

Paperwork such as helping you to optimize your credit file report in preparation for your mortgage application.

UK Mortgage Brokers expertise here may therefore help avoid any blemish on your credit file reports (at just the wrong time) by ensuring you get the correct mortgage provider deal.

Can Mortgage Advisors get Better Deals?

Do mortgage brokers get better rates is an often debated question? Indirectly, the answer here would be potentially yes can mortgage advisors get better deals.

It is often possible for our 'mortgage financial advisors' to get better rates than perhaps someone trying to just access the marketplace directly or via one provider.

Some providers may offer for example broker only deals that could be ideal for your situation. Let a broker scour the UK mortgage market for you, because that is their job role.

Use an independent mortgage broker v bank also if you want impartial advice. To then have access to the whole mortgage market, rather than just a panel, one bank or building society lender.

Or, alternatively you need to speak to a mortgage broker because you have a more difficult personal financial position eg; you have a poor past credit history, perhaps due to the Pandemic 2020's.

In this instance, your own bank may not be the best people to directly approach therefore. Your regular banking profile may clearly show you may have adverse money problems & so perhaps your bank don't want your risk.

So, let's now look at some key reasons to consider why to use our mortgage broker uk versus bank for your best mortgage deals.

So whether you are looking for the best mortgage brokers near me like independent mortgage brokers in ipswich or mortgage brokers in essex - we hopefully can still help you.

Can Mortgage Brokers get you a bigger mortgage?

Often people enquire whether it is possible can mortgage brokers get you a bigger mortgage? Indirectly, the answer here would be yes.

The reason being is a 'whole market mortgage broker' can have access to a whole range of mortgage lenders that may offer perhaps a bigger mortgage, than just approaching one or few providers.

This could be the case, if for example you're self employed with trading accounts & are looking to increase or maximise the amounts you can borrow for the mortgage.

NOTE: Be aware of the longer term financial commitment pressure issues you could face into the future however if trying to supersize your mortgage eg; rising interest rates, change of job conditions and lower salaries etc;

Top 5 differences of Mortgage with Broker vs Bank?

Put simply, our 'Brokers for Mortgages' intermediary may give you.....

- Choice of 150+ lenders

- Wide choice & range of mortgages

- Brokers Mortgage exclusive only deals

- All Credit Status considered - good or bad

- Access across the whole mortgage marketplace

Whereas a Bank may just give you...

- Single institution deals

- Simplicity not choice

- Convenience for you

- Strong existing banking relationship

- Not bothered about limited mortgage options

In conclusion here, in today's competitive mortgage market accessing the expertise of that mortgage broker versus bank, may help you to find that your best deals.

You pays your money & takes your choice to access the mortgage broker v bank uk fees.

Fees for Mortgage Brokers

Fees for Mortgage Brokers are often fixed but may vary for some, all dependent on the amount of work involved in arranging the mortgage for you.

Typically, if you look online for some independent mortgage advisers near me, they may offer their initial basic mortgage consultation & quotes for free (with no obligation at that stage).

They would then advise you what their costs maybe, based on the amount of work they envisage could be involved to get your mortgage & toward your dream home move.

Why 'does Mortgage Broker charge fees'?

Why do mortgage brokers charge a fee uk? How much does a mortgage broker cost uk? Or free mortgage brokers near me?

All these are typical popular google searches when researching online why does mortgage broker charge fees.

Each broker for mortgage will vary their own reasons as to why they charge a broker fee for their professional time, knowledge & expertise.

For example, sometimes a mortgage deal can appear to start off simply...but then get much more complicated as the deal progresses onwards.

The time spent involved by that mortgage broker that they calculated to be a set number of hours initially to help you, is now double that time involved. Do they now charge you double, or just take it on the chin?

The main reason you look to use any brokers mortgage or indeed life insurance brokers is to get their professional experience, advice & guidance.

So whether you are looking for a mortgage broker near.me like independent mortgage brokers in leicester or mortgage brokers in sheffield - we hopefully can still help you.

| Example Case UK Property Value £275,000 | Typical Fees Charged |

| High Street Estate Agent Fee - 1.42% inc VAT sole agency | £3,905 |

| Buying a house - The average conveyancing legal fees | £2,239 |

| Selling a house - The average conveyancing legal fees | £1,690 |

| Home Removal Local - Company Transport Fees | £1,181 |

| Mortgage Broker Fee average - To help arrange your deal | £395 |

Questions to ask a Mortgage Broker near. me

How much does a Mortgage Broker cost UK?

How much is mortgage broker fee? Well, if you applied for a standard rate mortgage or remortgage, often advisers may charge you fixed uk mortgage broker fees of £395.

Note: Some brokers may charge typically up to 0.5% of the mortgage balance eg; For a £100,000 mortgage broker fee is £500.

Given the above example case study chart, in the scheme of property purchase agents costs, that fee may actually appear reasonable for a whole of market mortgage broker uk?

Some 'Brokers for Mortgages' that do charge fees may usually cost this by either...

- Fixed price rate

- Hourly price rate

- Percentage deal rate

- Combination above rate

Note: Independent mortgage brokers fee are usually only payable when you receive the mortgage offer from the lender.

There are also some 'whole of the market mortgage broker' business that state they don't charge an upfront broker fee (but naturally no successful business works entirely for free).

How much is mortgage broker fee here is then potentially costed by the fact that they will still get paid % of the overall mortgage deal direct by the lenders.

So 5 factors to consider when how to choose Mortgage Broker...

- Check what is included in the services they may offer?

- Do they handle all that mortgage paperwork?

- Will they chase up lenders, solicitors, surveyors, estate agents?

- When are they available to help you?

- Office hours 9-5 only...or also after work hours?

In conclusion here & when looking up how to choose mortgage broker, we suggest that you need a company that will go that extra mile for you. One that will help you get that mortgage deal, to help you secure your dream home.

But ultimately we would recommend you ideally use a 'whole of the market mortgage brokers' rather than someone who is tied to say one company or can only access a more limited range of mortgage products.

So whether you are looking for a mortgage broker near. me like independent mortgage brokers in colchester or mortgage brokers in norwich - we hopefully can still help you.

How does Mortgaging work?

How does Mortgaging work?

'What is Mortgaging' = a Big Loan to help you buy a House / Property

- Apply for a mortgage loan > via a bank, building society, credit union or other finance lender

- Firstly you need to save up money as your deposit (most lenders will expect some deposit)

- Example > £100,000 property less £25,000 deposit = £75,000 mortgage loan needed

- Lender % interest rate may depend on amount borrowed, term, credit history & mortgage type

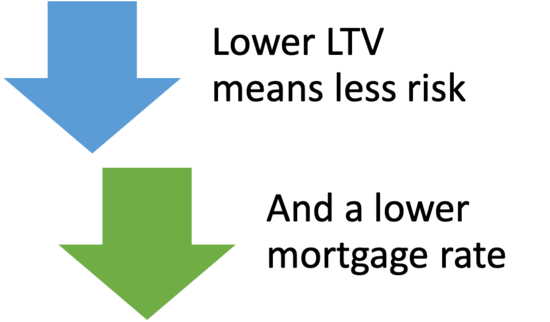

- Bigger deposit = better mortgage interest rate deal - as less risk to Lender (loan to value)

- Smaller deposit = worse mortgage interest rate - as higher risk to Lender (if property values drop)

- Mortgage is repaid monthly over a set number of years or mortgage term (max usually 40 years)

- Longer term = lower monthly costs but higher overall interest paid

- Example > £100,000 repaid over 30 years at 5% fixed = £537pm (total cost with interest £193,338)

- But £100,000 repaid over 20 years at 5% fixed = £660pm (total cost with interest £158,437)

- So how does mortgage work = quicker you repay the mortgage = less total interest you pay

- Interest rate you choose can be fixed for a term or it vary (affected by Bank of England)

Unsure and need mortgage advisers uk mortgage advice, then speak to our UK 'Brokers for Mortgages'.

So whether you are looking for a mortgage broker near me like independent mortgage brokers in chester or mortgage brokers in northampton - we hopefully can still help you.

Please contact us to access whole of market mortgage network & 'mortgage advisers near me' >

Calculate: UK Mortgage Payments >

10 Keys to Application Success - How does the Mortgage work?

Firstly, do you actually want to buy a house? Are you okay to commit yourself and maybe your partner to a long term mortgage over say 20 years plus?

If so, how does the mortgage work uk typical application process...

- Save towards your deposit down payment (for your dream home)

- Set Budget how much can you afford every month

- Check your credit file is okay & on voters register

- Contact a mortgage broker in UK or go direct to lender

- Calculate how much can you actually borrow

- Get a mortgage agreed in principle & apply for it

- Find the dream property you want or can afford

- Have a home valuation done + appoint solicitors

- Get the mortgage offer agreed on the house

- Insurances in place & complete new property deal

Buying your new dream home is not a 1 minute wonder...it could be a lengthy process before you finally exchange contracts & at last get the keys to your dream home.

Like finding your ideal partner for life, there maybe lots of property viewings, lots of paperwork & perhaps lots of hassle & stress.

As such, we would always recommend you speak to a professional broker mortgage uk qualified, someone who is used to dealing with these situations.

'What does a Mortgage Advisor do'?

So finally 'what does a mortgage advisor do'...Our mortgage finance advisor will do the following before you apply for a mortgage:

- Thoroughly explore your personal circumstances

- Explain what different mortgage deals are available

- What types of mortgage there are that could match your situation

- Advise you on which ones they feel meet those needs

- Give you good, clear, fair & not misleading reasons for their advice

- Finally, why they are recommending a particular mortgage deal

Unsure about which UK Mortgage Advisors to help you, then please speak to our UK Brokers for Mortgages.

So whether you are looking for a mortgage broker near. me like an independent mortgage advisor birmingham or an independent mortgage advisor belfast - we hopefully can still help you.

Please contact us: access whole market mortgage network & 'mortgage advisers near me' >

UK Mortgage Brokers for Expats

UK Mortgage for Expat

As mortgage broker UK expat specialists, we can help you to take out a mortgage on a UK property that you are intent on buying (whilst you are still a UK expat).

UK Expat mortgage lenders currently deem someone is an expat who is UK national living & residing abroad or working in another country than the UK ...but they are not a national of that country.

As UK Mortgage Brokers for Expats we can clarify that this is different from buying a property abroad & taking out a mortgage for that overseas property.

Note: UK domicile rules & non domicile for tax purposes are different for lending mortgage uk expat purposes.

Mortgage Broker UK Expat

Often mainstream high street providers do not offer this service to their clients, pointing instead to a more specialist mortgage broker uk expat deals.

Some of the reasons perhaps also any local mortgage broker near.me may not be able to help includes they are not geared up for dealing with...

- Offshore investments

- Family income trusts

- International income money currency

- None uk credit profile

With access to over 35+ expat mortgages in the uk lenders, our 'whole of the market mortgage brokers' have in house uk expat mortgage broker specialists.

As such, our Mortgage Brokerage is well placed to help you. Unlike any independent mortgage advisor near me, they may not have the expertise in this particular expat area.

Expat Mortgage Broker 'UK Mortgage Advice' options...

- Access to Whole of Market-Leading Expat mortgage rates

- Residential mortgages > up to 90% LTV

- 'Expat buy to let mortgage' > up to 75% LTV

- Loans from £25,000+ with no maximum limit

- Interest only options

- Fixed & variable rates

- Light adverse credit

UK Expat Mortgages Broker help

- Expats that reside in a range of different countries

- Expats that are either Self Employed or Employed

- Mortgage Broker expat options if buying through a limited company

- Expats that no longer have a UK bank account

- Buying a UK investment property for their kids to live in whilst at university

- Expat 1'st Time Buyers

- Professional or 1'st Time Landlords

So whether you are looking for a mortgage broker near.me like independent mortgage brokers in reading or mortgage brokers in kent - we hopefully can still help you.

Please contact us: access whole of market mortgage network & expat 'mortgage advisor near me' >

*UK Mortgage Broker FAQ:

How long does a Mortgage Application take?

* How long does a Mortgage Application take to be approved?

The speed of approval can depend on a large number of factors. Here are some average timescales for the mortgage application process...

Remember though, if you try and rush & pressurize this process to go quicker, then professional mistakes can sometimes happen![]()

This could be the most expensive purchase you ever make, so accuracy is critical & all parties involved need to be onboard to help you.

Whether you use independent mortgage advisors near me or not - the process is similar

- Make an appointment to see or speak to someone [1/2 weeks ahead]

- Relevant documents in order if needed? (popular topic in money savings expert forums)

- 6 months bank statements, proof of income wage slips or self employed accounts okay?

- ID verification in order? eg; passport, driving license, national insurance or recent council tax etc;

- On top of any paperwork as requested by broker or lenders? [a few days if not]

- Proof of your deposit? (money laundering checks)

- Your credit ratings all okay or not?

- Income & affordability assessment checks? [a few days if not]

- Making a decision on the mortgage deal? [we will think about it...& take weeks to decide]

- Mortgage offer to finally arrive? [2/6 weeks & then valid for upto 6 months]

- Do you want a standard home buyers report or a full structural survey? [2/3 weeks]

- Results of that mortgage valuation survey? [2/3 weeks]

- Has survey produced more queries, issues & problems or it's all okay?

- Valuation to offer assuming no problems? [a few days to a few weeks]

- Preparation toward exchange of legal contracts conveyancing? [2 months]

- Completion & assuming no part of deal has caused problems? [1 month]

So whether you are looking for a mortgage broker near.me like an independent 'cardiff mortgage broker' or a 'newcastle mortgage broker' - we hopefully can still help you.

Terms of Mortgage | 'UK Mortgage Brokers' Jargon

It is easy whenever you do your own job, to fall into that easy mistake of speaking to someone else (not in your line of work) in your professional work jargon.

As such, they may not understand what you mean as they talk this foreign mortgage language. Don't be too embarrassed to ask ....what is say a flexible term mortgage, or what is freehold or leasehold difference re your collateral?

Naturally, when it comes to the biggest financial decisions you could make, it therefore helps if you know what the mortgage broker or lender is talking about to you.

So, we have now included below various Terms of Mortgage glossary as a helpful guide...

Terms of Mortgage Glossary

- Agreement in Principle (AIP); Or mortgage agreement decision in principle = how much you can borrow. Proof to show estate agents, sellers or other relevant parties

- APR: Annual percentage rate of charge = total cost of the mortgage loan as an annual percentage. APR can help you compare different mortgage offers

- Bank Base Rate: Rate of interest = set by the Bank of England (BoE) and which a lenders standard variable rates may follow

- Bridging Loan: Short term loan = bridge or plug gap funding until your property is sold or work to be done completed

- Buildings Insurance: Usually a legal requirement for the lender to have adequate buildings insurance cover in place ideally from exchange of contracts

- Building Survey: Structural survey level 3 = in depth comprehensive residential property inspection to provide a detailed evaluation of a property's condition

- Buy to Let: Purchase of property by a landlord = to rent out to tenants as a longer term investment for income or capital growth

- Capital & Interest Mortgage: Your monthly mortgage repayment = covers both the interest & reduces the total capital balance outstanding

- Capped Mortgage: Have an interest rate ceiling limit = over which your interest rate cannot rise above

- Collateral: Usually your home = used by the lender to secure against when you out a mortgage ie; you fail to repay so they retake your property as collateral

- Conveyancer: Legal solicitor or specialist-licensed person = who can process the buying & selling of property

- Deeds: Title legal deeds documents = records ownership of a property bricks & mortar and surrounding land

- Deposit: Amount of savings = down payment needed towards purchasing total property cost. May vary from mortgage product & provider

- Discount Mortgage: Pay a fixed discount version of your lender’s standard variable rate = reduction applies whether this rate increases or decreases

- Early Repayment Charge (ERC) A fee charged = should you repay the mortgage early. This may vary, so check your terms & conditions

- Equity: The difference between = current value of your property minus any outstanding secured mortgage or home equity loan

- Equity Release: You raise a sum of money with rolled up interest = from your property & repaid when the homeowners pass away

- Finance Broker: Person or Company = Finance Brokers match up people with their personal or business funding requirements to sources of finance

- Fixed Rate Mortgage: The mortgage interest rate = fixed for a specific time period ie; 1/2/5/10 years even if the lenders base rate changes

- Flexible Mortgage: Flexible options = could allow you to have payment holidays, make overpayments or underpayments

- Freehold: Person or organisation has outright ownership = forever of any property & the land onto which it is built

So whether you are looking for mortgage brokers near.me like an independent 'birmingham mortgage broker' or a 'bristol mortgage broker' - we hopefully can still help you.

'Whole Market Mortgage Broker' Terms Glossary

- Gazumping: Seller reneges = Goes back on original agreed deal ie; accepts a higher offer from somebody else or raises their asking price

- Gazundering: Buyer lowers their offer at the last minute = Goes back on original agreed deal eg; just before contracts are exchanged

- Gifted Deposit: Deposit gift from a 3rd party = Provides some or all funds towards mortgage deposit eg; parents or other family

- Guarantor: Legal agreement via a 3rd party = Help meet your mortgage repayments if you are unable to eg; parent, family or guardians

- Help to Buy: Government assisted purchase scheme = help people buy their own home but scheme ends in 2023

- High Lending Charge (HLC): Amount borrowed exceeds a certain % percentage of the property value = Protects lender against mortgage defaults

- Homeowner Loan: A loan secured on property to borrow money against your property which is collateral

- Homebuyer Survey: Inspection of the property’s condition level 2 = identify any structural problems, concerns & then provide suggestions for repairs

- Joint Mortgage: Property ownership = equally held between 2 people so if one person dies, ownership then passes over to the owner

- Land Registry: Government body = registers the ownership of land and property in England & Wales

- Leasehold: Own the property for a specific number of years = but not the land on which it is built eg; Flats often sold on leasehold basis

- LTV (Loan to Value): Percentage value = mortgage loan outstanding minus value of your property eg; £275,000 mortgage left & your home is worth £375,000 (LTV is 73%)

- Maturity Date: Mortgage date = when it must be repaid in full or any agreement ends eg; 5 year fixed rate mortgage maturity date

- Mortgage Illustration: Quote illustration = key facts about your mortgage shown before you finalize a mortgage application ie; costs & fees, APR, monthly payments

- Mortgage Finance Advisors: Specialist 'uk mortgage advisor' helping you research the whole market to find and arrange your best mortgage broker deal

- Mortgage Offer: Guarantee to a formal offer = after mortgage is approved ie; sets out all your T&CS's

- Mortgage Overpayment: Pay extra amounts = one off sums or regular amounts above your usual monthly mortgage payments ie; shorten your mortgage term & interest

- Mortgage Period (Term): Period of time = you repay your mortgage over eg; 35 years

- Mortgage Protection: Life Insurance, Critical Illness or Income cover = protects your mortgage if you die, seriously ill or off accident or illness

So whether you are looking for mortgage broker near me like an independent 'york mortgage broker' or a 'london mortgage broker' - we hopefully can still help you.

'Whole Market Mortgage Brokers' Terms Glossary

- Negative Equity: Valuation of your property = falls below the mortgage outstanding eg; £275,000 mortgage left but your home is worth £270,000 (LTV is negative)

- 95% Mortgage: Borrow up to 95% of the mortgage loan amount = Have just a 5% deposit ie; property loan to value ratio (LTV) = 95%

- Offset Mortgage: Link both your mortgage & savings together = benefit is it reduces the overall amount of interest you maybe charged

- Payment Holiday: Period of time = you make no payments on your mortgage but interest still be charged

- Portability: Existing mortgage terms = transferred or ported across properties if you move home

- Product Fees: Initial set up fees = for your mortgage deal & terms which may vary between providers (so shop around)

- Product Transfer: Switch your mortgage deal to another = via same provider eg; product transfer with same lender to a fixed rate deal

- Remortgage: Transfer your mortgage deal = from one provider to another eg; Take deal to another lender to get better interest rate terms

- Right to Buy: Existing tenants of council or housing association houses = allowed to buy property they may currently rent but at a discounted market price

- Second Mortgage: A 2nd charge on mortgage alongside the main mortgage = allows you to use any remaining equity you have in your home as security

- Service Fees: Charge made by a lender = covers their admin costs eg; request previous mortgage lender details & with your consent

- Specialist Mortgage: One that maybe doesn't fit into the 'mainstream norm' mortgage providers = had bad credit or bankrupt, expats, offshore contractors, new builds

- Stamp Duty: Tax charged = when you buy a property ie; the tax you pay for a new property increases based as a percentage of the purchase price

- Standard Variable Rate (SVR): Providers default mortgage interest rate = standard mortgage rate terms without any special rates, discounts or deals

- Tracker Mortgage: Mortgage interest rate will rise & fall in line = but set at fixed percentage above the Bank of England (BoE) base rate

- Valuation: Proof that the property exists and is worth the amount you want to borrow = required by mortgage lenders

So whether you are looking for mortgage brokers near me like an independent mortgage broker yorkshire or an independent mortgage broker manchester - we hopefully can still help you.

*How long does it take to move houses?

According to a survey by comparemymove* how long does it take to move house on average, this process may take between 3 > 6 months from start to finish.

In the scheme of things, how long do mortgage brokers take at 18 > 40 days in their survey is a fair average, assuming no complications.

Here is their breakdown of how long does it take to move house uk survey article.

| HOW LONG DOES IT TAKE TO MOVE HOUSES? | TIME |

| |

| Finding your ideal home | 10 >12 weeks |

| Getting suitable mortgage | 18 > 40 days |

| Legal Conveyancer | 8 > 12 weeks |

| Property Surveyor | 2 > 3 weeks |

| Exchange Contracts | After 8 weeks |

| Completing the Sale | 7 > 28 days |

| Moving Home Day | 1 > 2 days |

How long for a mortgage application to be approved time taken can include the property specifics you have viewed & now putting an offer on, alongside details on that property sellers estate agent.

Is this a standard property deal, with the new property & surrounding land all in good order?

Or, simply now how long does a mortgage take to be approved becomes more complicated because the deal for example involves a flying freehold property?

So whether you are looking for a mortgage broker near.me like an independent mortgage broker london or an independent mortgage advisor glasgow - we hopefully can still help you.

Please contact us to access whole of market mortgage network & a 'mortgage advisor independent' >

'Phil Spencer Location Location Location' House Survey Tips

* How long for Mortgage offer after valuation?

How long for mortgage offer after valuation will depend on if your mortgage application has been completed and signed off to date.

If so, then here are some average timescales for the mortgage offer after valuation. Note: This valuation as mentioned could be a standard home buyers report (for benefit of lender) or upto a more in-depth building full structural survey (more for your benefit) .

Once any valuation is received from the surveyors it should be checked immediately by the lenders. The longer & more detailed the report, the longer the assessment timescales.

Assuming there are no structural or technical issues eg; japanese knotweed issues...then a fair property valuation = fair to purchase price being made.

Watch the above video by property guru phil spencer location location location helpful check list on importance of different survey types.

This is then sent off for a final check through. If all okay, then a mortgage offer will be produced.

So how long for mortgage offer after valuation should be received could be within a week if the valuation survey is all fine & naturally longer if not.

As a 'broker for mortgage' we are used to dealing with these situations & will chat you through the likely timescales and issues raised.

As such, all the best mortgage brokers in the uk will try to update you each step of the process & keep you in the loop.

So whether you are looking for mortgage brokers near me like an independent mortgage advisor london or an independent mortgage advisor liverpool - we hopefully can still help you.

Please contact us to access whole of market mortgage network & a 'mortgage advisor independent' >

Kirstie Allsopp & Phil Spencer 'Location Location Location'

Mortgage Broker FAQ: Importance of Location Location Location?

The importance when buying a new home as the name of their shows proudly states is 'location location location'.

They also have a newer spin off show called 'love it or list it' which they chat about on ITV's Good Morning Britain.

Or in other words, the old adage they would always say is compare buying longer term the worst house on the best street...Rather than the best house on the worst street.

The location of your property can have a big impact on whether or not you may enjoy living there? Also, secondary for some, number 1 for others... is if it then ends up being a worthwhile long term investment.

Of course, you may have your own property location location location wish list. Here are a few pointers to consider and in no particular order.

However, if you asked the best mortgage brokers in uk for their guidance (rather than the estate agent trying to just sell you the housing stock they have). Note: none of these involve the property style, or interior size etc;

So we recommend you perhaps make a list of your top 10 priorities when it comes to deciding what makes a good home location for you.

For example....

- Ease of Parking

- Council tax banding

- Good Transport links

- School catchment area

- Buzz & feel of the place

- Access to local amenities

- Local green spaces & areas

- Sense of a good local community spirit

- The local buildings architecture and surrounding area

- Close to traffic noise, cars, trains, planes or busy roads

So ask your local mortgage brokers in the UK based questions about this also perhaps (you are paying for their knowledge) & rather than just talk about the best mortgage deals & rates. If they are local, they should be able to give you some good hints & tips.

What would your ideal home also look like eg; 3 bedroom semi detached or 2 bed flat, new build or older property, small or large garden? etc;

Think ahead if say you were looking to start a family in the future, so may need more space. Or conversely, you may need the house to be more accessible as you get older.

So whether you are looking for a mortgage broker near.me like an independent mortgage advisor cardiff or an independent mortgage advisor leeds - we hopefully can still help you.

'Chain Property' what is it?

What is a 'chain property'? It is where you are buying a property...but behind it (or ahead of it) are small or large group of home sellers & buyers all interlinked in that property chain.

So, if you want to buy a new house, but then have to wait until your seller buys their next house, then you are buying a chain property.

As such, this could mean that moving homes could be abit more complicated & therefore take a bit longer. Patience is the key when dealing with this for most Mortgage Brokers in the UK.

The more people in a property chain, the more likely it is that something may unfortunately go wrong ie; the purchase or sale of your house may fall through.

Talk this through with your 'uk mortgage advisor', with regards to the timescales your mortgage deal is approved for, should this chain property deal go on for months.

Mortgage Broker Questions | Average Property Chain Length UK?

Our mortgage brokers online uk search to see what is an average property chain length uk was inconclusive in these Post Pandemic 2020's.

Some say the Average Property Chain Length UK can vary anywhere from as little as 3 properties right up to 10+ properties. As an independent broker for mortgage we see this figure can be affected by various delays.

These unfortunately are a regular occurrence during the 'chain property' buying process & there are numerous factors that can contribute to these delays.

Even the best mortgage broker in uk would always highlight the chance of having chain property problems to consider:

- A seller or buyer decides no longer want to proceed

- Someone's property survey reveals unknown problems so the buyer withdraws

- Legal teams are slow in processing & requesting conveyancing information

- One of the chain property buyers has problems getting a mortgage

- A seller or buyer attempts to renegotiate their property deal

- Unforeseen events like accident, sickness or Covid 19

- Gazumping or Gazundering

So whether you are looking for a mortgage broker near.me like an independent mortgage broker york or an independent mortgage broker in coventry - we hopefully can still help you.

Please contact us if unsure which mortgage advisor to use to access whole of market mortgage network & a mortgage adviser independent deal >

UK Mortgage Broker FAQ | 'Checklist for Moving Home'

After many weeks of dreaming about buying your new home, it's getting nearer that time. Hopefully, which ever 'mortgage brokers in the uk' you have used here, they have also now helped you to arrange things into order and its all good news.

So it's now all green lights & its your count down to you making a 'when moving house checklist'

Top 10 People to notify when moving to house checklist....

- Financial institutions

- Insurance companies

- Local Government

- Utility Gas & Electric

- Phone & Broadband

- Bills regular

- Health services

- Work office

- Education

- Family & Leisure

Courtesy of 123 infographic - here is their helpful to do 'checklist when moving home'...

So whether you are looking for mortgage brokers near. me like an independent mortgage advisor glasgow or an independent mortgage advisor edinburgh - we hopefully can still help you.

Please contact us to access whole of market mortgage network & mortgage broker near. me for 'independent mortgage advisors' deals >

Mortgage Brokers in England, Scotland, Wales & NI

Top 10 'Mortgage Lenders in UK'

The Top 10 Mortgage Lenders in UK* in order of gross value lending size in the 2020's are;

- Lloyds Banking Group

- Nat West Group

- Nationwide BS

- Santander UK

- Barclays

- HSBC

- Coventry BS

- Yorkshire BS

- Virgin Money

- TSB

According to this Mortgage Introducer survey, they state that ‘The Big Six’ of Best Mortgage Lenders in UK currently have around 65% of the total market share as at 2022.

These UK largest mortgage lender stats are similar to but not the same figures also as the total value of UK mortgages outstanding with all 'Mortgage Lenders in the UK'.

However, what it does not do is highlight or point out the importance of another very large and missing UK top 10 lender. "The Bank of Mum and Dad"

The bank of mum and dad mortgage power going forwards their Mortgage Introducer survey says could help to fund around a 1/4 of all UK property transactions. Over 40% will also get help from friends & family.

As mentioned, as an 'independent mortgage broker' who can access the whole market, we can source these & also many more of the best mortgage lenders in UK.

Let's now briefly look at the various mortgage insurances you may need & how as a 'mortgage broker in the uk' we can also help.

All may help you to decide on which mortgage brokers best fit into your own circumstances.

Mortgage Broker Insurance

Mortgage Brokers & Mortgage Protection

Your home is probably going to be the biggest purchase you may ever make & your mortgage probably your biggest debt. So the right decisions need to be made when considering insurance.

Having the correct mortgage insurance cover is therefore your essential safety net, your peace of mind back up plan, if things do go wrong over say a 20/25/30 years timescale.

Some specialist mortgage providers may still make it a condition to get some type of mortgage protection insurance. But generally nowadays this is no longer the case.

So when looking for a mortgage and insurance broker, note generally who ever you are now taking out a new mortgage broker deal with, they should not make you take their mortgage life cover insurance out via their company only.

Mortgage Decreasing Life Cover may help protect a repayment style mortgage over its term. You can also include critical illness cover on your mortgage protection, which helps protect you should you be diagnosed with a specified serious critical illness like cancer, heart disease or stroke.

Mortgage Level Term Life Insurance policy may help protect an interest only style mortgage, but only over its term. Mortgage Whole of Life Assurance may also help protect an interest only style mortgage.

Mortgage Payments Protection (MPPI) is a shorter term mortgage protection cover, usually for 1/2 years only. It helps you to cover usually just your mortgage payments (perhaps a bit extra for a some bills) if you are unable to work due to accident, sickness or unemployment.

Income Protection (PHI) alternatively is a more comprehensive longer term benefit, that helps cover your income, not just your mortgage payments alone.

Note for mortgage broker insurance requirements: Some maybe a 'whole of market mortgage broker' BUT then not give you access to a wide range of the life insurance market. Martin Lewis on Life Insurance points this factor out when choosing average life insurance mortgage protection cover.

This can appear confusing if comparing a mortgage broker vs insurance broker, as you may imagine if they are a mortgage broker whole of market, that should also be the same as being life insurance brokers.

It can be important for example if the lenders mortgage insurance declined you due to say raised BMI KG & you are now looking for alternative insurance. Get a broker Mortgage Protection quote > 15 secs

Mortgage House Insurance

Mortgage House Insurance may not a legal requirement for some, but most mortgage lenders insist that you do have buildings insurance in place when you exchange contracts.

This is when you take over legal ownership of a freehold property, and are then responsible for the building bricks & mortar. It makes good business sense.

Worst case scenario, mortgage house insurance helps protect you against those costs of having to repair or rebuild your home from scratch.

If however you are buying a leasehold property or flat, you may not need to arrange this yourself but you will still need some form of mortgage house insurance.

This insurance responsibility usually now lies with the landlords' insurance who may own the freehold. But please check with your solicitors, estate agents etc; who is responsible for insuring that building as this is not always the case.

Buildings insurance typically covers you for...

- Buildings structure

- Your permanent fixtures & fittings eg; kitchen, toilet & bathroom

- Any outside buildings eg; garage & garden shed

Don't forget your contents insurance also. If you had a fire, the emotional impact damage & financial replacement costs to all your goods & belongings could be catastrophic, after the fire brigade have finally put out the fire.

Talk to our 'UK Mortgage Advisor' about some of the best broker deals here.

Conclusion | Whole Market Mortgage Broker UK

So we have looked at what are the key differences between why use a Mortgage Broker v Bank. Why use independent mortgage brokers that are a whole market mortgage brokers v panel only mortgage brokers UK.

Explaining the fees for an independent mortgage advisor v other agents involved in the house buying process. How does mortgaging work v how long does a mortgage application take. Various terms of mortgage jargon typically used by Mortgage Brokers in the UK.

How long does it take to move houses v how long for mortgage offer after valuation. The importance of 'Location Location Location' & Phil Spencer and Kirstie Allsop. What is a 'Chain Property' v Average Property Chain Length UK.

Your checklists for moving home and finally how as mortgage brokers in the UK insurance re types of mortgage & property protection. All may help you to decide on which mortgage brokers best fit your circumstances.

So whether you are looking for any mortgage broker near. me or an independent mortgage advisor bristol or an independent mortgage advisor york - hopefully can still help you with our nationwide 'mortgage broker independent' support.

Article on ‘Mortgage Brokers in the UK’ and England by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women - we also review many of the best brands selling Family, Mortgage, Home Loans & Business Life Insurance in UK (inc NI)

'Brokers for Mortgages' UK Quotes >

England | Wales | Scotland | Northern Ireland

|  | | |

Confidential Enquiry | 'Whole Market Mortgage Brokers' UK | 150+ Lenders

NOTE: YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE OR ANY OTHER DEBTS SECURED ON IT.

*For products with any investment element we may introduce you to an FCA authorised adviser after any further review. We may also introduce you to other selected professional partners for other protection, finance (such as a whole of market mortgage broker) or legal products as deemed appropriate. By completing our enquiry form you ‘may be introduced to another lender/provider’.