Myself

Myself My

My My Income

My Income

Article on: Family Income Benefits Insurance

| – |  | – |  |

What is a Family Income Benefits (FIB) Policy?

A ‘Family Income Benefits’ policy [FIB] is an insurance that pays upon claim a tax-free monthly income, within the agreed plan term.

Most plans also include free ‘terminal illness’ cover. The benefits could be for life insurance & you may also have the option to include critical illness cover benefit.

Note: Some FIB plans you can opt to be paid quarterly or annually at claim (rather than monthly) until the benefits cease being paid.

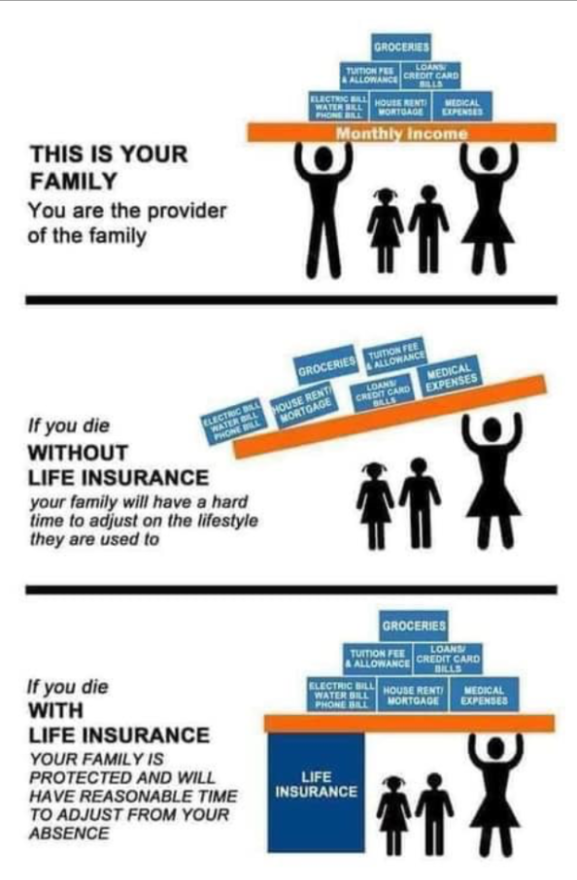

‘Family Income Benefits’ Insurance

So how does FIB work?

With a lump sum level term life insurance policy, the amount of cover remains the same from the start to the end of the plan (unless you choose inflation option). This means the payout risks to the Life Insurers remain the same from start to end.

However, with a family income benefits policy, the Insurers cover instead decreases over the time of the policy. As such, the income payout risks to the Life Insurers also continually decreases from policy start to end. In essence, it therefore works abit similar to mortgage decreasing cover.

This is probably best explained by Family Income Benefit (FIB) 3 example cases – and the effects on the Family of having some Life Insurance…

Family Income Benefit Case Study – EXAMPLE 1

- Young couple take out a joint FIB lifecover plan

- Have 2 children under age 3 & probably dependant for 20 years

- Rent a property for £1,200pm

- They look at all their normal bills & rent to decide the amount to insure

- Decide on a £2,500pm (= £30,000pa) FIB policy benefit over 20 years

- A death claim sadly comes in year 7

- So the FIB now pays £2,500pm for the remaining 13 years

- Or FIB equivalent lump sum of £390,000 ie; £30,000 x 13 years

- After 13 years payout the policy ends

Family Income Benefit Case Study – EXAMPLE 2

- Divorced parent has to take out a FIB lifecover plan

- They have to cover their child maintenance fees £1,000pm

- 1 child aged 12 but agreed legally dependant for 10 years

- Take out a £1,000pm FIB policy benefit over 10 years

- A death claim sadly comes after year 9 and 10 months

- So the FIB pays £1,000pm just for the remaining 2 months

- Afterwards the policy ends

Family Income Benefit Case Study – EXAMPLE 3

- Married woman wants to take out a FIB lifecover & critical illness

- Concerned about paying bills if critically ill or upon death

- She wants the 2 policy FIB benefits split out at any claim

- Looking to take FIB cover upto retirement age 65

- Takes out a £2,000pm FIB but split 2 policy benefits

- She wants the plan RPI index linked to offset inflation

- A critical illness claim for serious breast cancer comes in year 4

- At that point her FIB critical illness benefit is £2,185pm re RPI

- So the FIB pays £2,185pm upon critical illness for next 13 years

- By now the FIB had already paid her £340,860, excluding RPI

- However, she sadly dies age 45 & the critical illness payout ends

- Instead the Lifecover part now pays £2,985pm RPI up to age 65

- Or FIB lump sum of £716,400 (less RPI) ie; £35,820 x 20 years

- That split FIB policy had paid out over 1 million in claims

- After 20 years payout the policy ends

.

Lump Sum OR Family Income Benefits?

As Life Insurance Brokers we are often asked this question…which is better – a Lump Sums Term Life Insurance or Family Income Benefits – paying in effect a monthly pension?

Let’s examine here some of the key differences.

Lump Sum Life Insurance v Monthly Income FIB

Cost Benefit Differences between the 2 plans

A Family Income Benefits plan is usually cheaper, as it is a decreasing style plan. As mentioned therefore, the risks to the Insurer also decreases over time. Let’s see in practise what this means at different yearly timeline stages.

Case Study Example:

Person aged 30, non smoker, fit & healthy and looking to spend between £30-£35pm. They want family protection insurance cover over 30 years term.

They ask you what is the general Timeline benefit payout differences roughly between the 2 policies? Here are some typical broker quotes for this budget.

So they could typically get either around £1 million level term life insurance for 30 years. Or a Family Income Benefits term life insurance for 30 years £60,000pa (£60kpa ) = £5,000pm.

In this example comparison below, both £1 million level term & £60,000pa FIB plans are level ie; benefits are not inflation proofed to ease a general comparison.

With some Insurers you could commute the FIB income at claim, to give a lump sum instead (but this maybe reduced for some Insurers. It may also cause IHT issues – see our below FAQ).

| Death Claim Paid | Lump Sum Level Term | Family Income Benefits | Payout | FIB v Lump Sum Benefit | Timeline |

| * Year 1 | £1 million | £60k x 29 Years = £1.74 m | FIB = Extra £740k |

| * Year 5 | £1 million | £60k x 25 Years = £1.5 m | FIB = Extra £500k |

| * Year 10 | £1 million | £60k x 20 Years = £1.2 m | FIB = Extra £200k |

| * Year 16.6 | £1 million | £60k x 16.6 Years = £1m | FIB = Same |

| * Year 20 | £1 million | £60k x 10 Years = £600k | FIB = Less £400k |

| * Year 25 | £1 million | £60k x 5 Years = £300k | FIB = Less £700k |

So, in this above typical 30 years case study, we can see that for the first 15 years, the family income benefits plan is potentially financially better value than a £1 million lump sum.

However, from year 15 onwards, FIB gets financially worse as it continues to reduce over the time period ie; comparison shows FIB equivalent if commuted to a full lump sum at claim.

Lump Sum Invested v Monthly Income

Let’s also look however at the issues of having a lump sum payout at claim when invested, to try and give a monthly or equivalent returns. Note: Inflation may erode your capital and we are not investment advisers.

In the example below, we still follow the £1 million lump sum payout if invested v £60kpa Family Income Benefit plan like for like.

You will see that it would require an investment return of at least 6% to return £60,000pa and maintain the original capital values. Naturally, in this example if you need to only take £30,000pa then a 3% return will retain the original £1 million sum invested.

| Lump Sum Invested | 1% return | 3% return | 6% return |

| *£1k Million | £10,000pa | £30,0000pa | £60,000pa |

| V FIB £60kpa | Less £50kpa | Less £30kpa | Same as FIB |

| Time to Run Out… | 20 yrs | 33 yrs | – |

Should you opt for a lump sum life insurance versus a family income benefits, you will then have to decide at claim where best to invest your capital risk wise, to help you provide a steady monthly pension style income. Also, Govt savings tax issues could arise with any investment returns.

Naturally, if the main family breadwinner died, then this could be the last thing you would want to think about?

Ordinary People are Working Millionaires?

Ordinary People are Working Millionaires?

On the Money Saving Expert Life Insurance website, Martin Lewis on Life Insurance says for a good rule of thumb, his Best formula is ‘THE 10 x RULE’ ie; aim to cover 10 x the Annual income of the main breadwinner or highest earner until any kids have finished full-time education.

So, in this Martin Lewis formula if you earned £33,500pa then he says consider family life insurance sum for at least 10 x salary = £335,000 to insure yourself for (after any mortgages, loans & debts are repaid ie; consider cover for them seperately)

As such, you may wonder how we quoted £1 million pounds in the above FIB example above, when that sounds a fortune?

BUT following on from this simple Life Insurance coverage example formula, if you earned say £33,500pa then worked for the next 30 years until retirement, you could potentially earn over £1 million gross ie; £33,500pa x 30 years [or more with any future inflation wage rises].

Apart from losing a loved one & family breadwinner, this real hidden income threat is what could be lost if the main earner died prematurely.

How much does this all cost?

- Often average prices can start from as low as £5pm (for 1 product)

- But your monthly or annual premium costs will vary in a few ways

- Premiums will depend on your ages, health, lifestyle, amount of cover, policy term

- It could be you are offered standard costs or have to pay abit extra insurance price risk

- Eg: Extra risks if have raised BMI Kg, high blood pressure, cholesterolor Diabetic

- Any paid for extra features (like critical illness) you want will also affect the cost

- Is the cover to remain level or increasing to offset inflation rises ?

- Remember cheaper here, doesn’t necessarily mean better

Family Income Benefits Broker FAQ

Joint or 2 x single FIB Insurance plans?

The benefit of having 2 x seperate plans (known as dual life insurance) if in a relationship & one partner claims, then the surviving partner still has their own seperate FIB policy. That single life FIB insurance will cover just that 1 person only. It then pays out the chosen amount of cover if the person dies, or is terminally (or critically ill if benefit chosen) during the term of the policy.

A ‘joint’ names Family income benefits policy means it jointly covers 2 lives but crucially then pays out on ‘1st death or claim’ basis. This means once the chosen amount of cover is paid, the FIB policy benefits would then end. This is usually the cheaper option for Insurers (as it only pays benefits once) but conversely leaving the surviving partner without any cover. You pays your money & takes your choice.

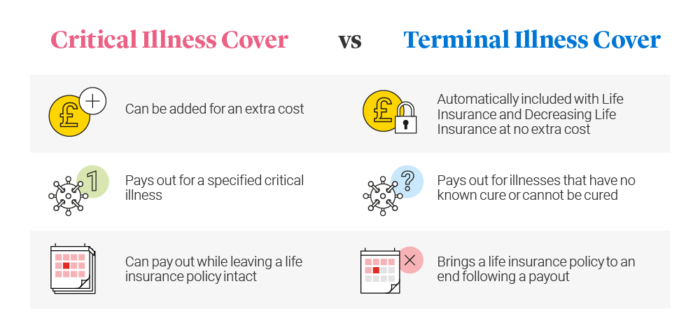

Critical Illness vs Terminal Illness Cover

Critical Illness is a special insurance benefit that helps protect you if you are diagnosed critically ill (as specified by Insurers) during the policy term. The top 3 benefits most Uk Insurers cover are for types of cancer, heart disease & stroke* ABI.

It pays out a tax-free sum that you can use, however. To help repay the mortgage, cover monthly expenses, health-related costs, lost income while you recover (although income protection maybe a better longer term policy in that respect).

- Critical Illness may pay out claims crucially upon ‘diagnosis and survival of the specified illness’

- So Critical Illness means you may live, survive & claim

- Critical Illness coverage may also provide some cover for your children

- Terminal Illness is often included for ‘free’ as part of a Family Income Benefits plan

- It usually means a GP consultant has advised you could have less than 12 months to live ie; incurable illness

- Terminal Illness means you will not survive long term after a claim

- Once agreed by Insurers, they may then payout this policy death claim but in advance

- Note:lifecover and critical illness plans are often combined anyway

What does putting a Family Income Benefits Into Trust mean?

- It tells the Life Insurance Company who you want to get the money if you sadly died

- Ensures it should go direct to you nominated beneficiaries via the trustees

- Putting your policy into ‘trust’ may also help to avoid probate delays & inheritance tax

- Without a trust the policy could fall back into your estate

- This applies even if you have made a valid will

- Most Insurers do supply free a good range of generic life insurance trusts, ideal for many client situations

Opting for a regular income paid to your partner or spouse is potentially more Inheritance Tax (IHT) efficient than a lump sum. However, should you choose to take the lump sum commute option that some Insurers offer (but perhaps at a reduced amount), then it may well increase the value of the estate for IHT. In this instance, placing the plan into trust could avoid any potential tax traps and also importantly probate delays.

Importance of Disclosure & Claims?

All Insurers are in business to protect, insure & payout. Lifecover is therefore based on your full disclosure at the time you take the original policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying.

The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless manner when applying. If so, it may not payout ! eg; Just socially smoking, then you must tell them you are smoker (even if it costs more).

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details.

They will then assess if your insurance claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers – not 100%).

Family Income Benefits v Sickpay Income Benefits

Sickpay Income Benefits Insurance (Income Protection Insurance PHI) provides a tax free income if you are unable to work through accident, illness or injury to help cover your regular bills & outgoings. Check the PHI wordings are ideally for ‘own occupation’.

Unlike, if you include critical illness within your family income benefits, it doesn’t just cover specified listed critical events diagnosed. Ideally, you should consider both policies & budgets permitting. see the chances of claim below.

Family Income Benefits & Govt Low Family Income Benefits

The hard facts why some families may consider family income benefits insurance cover, is to help avoid being on Uk government low family income benefits, if the worst should happen.

Looking at the above chance of claim statistics, it is a ‘back up plan’ for those whose lifestyle & income could sadly change for the worst, without any financial support. In today’s 2020’s rising bills, for many it could be lifeline away from this.

What if health or lifestyle changes after starting a FIB Insurance?

Any health or lifestyle changes since, usually does not void your existing family income benefits policy, if it wasn’t relevant at that time of initial underwritten insurance application. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your application what you initially disclosed to the Insurers, as this information then stands now and in the future. Please check your original T&C’s.

Conclusion

I hope that gives a generic background to a Family Income Benefits policy. As Financial Advisers, we recommend to ideally ‘Protect 3 Things’…

- LUMP SUM > Repay any mortgage & debts, cover funeral costs

- INCOME > Help cover all your monthly bills

- LUMP SUM > Back up for holidays, education, emergencies

This basic formula is naturally dependant on wether you are married or cohabiting, have young or older dependants, retired or both working still. Have sufficient backup already in your savings & investments.

Please check out & Compare Online Broker only deals here to decide how much these may cost.

If you have dependant family members on you, then you know it makes good sense ![]()

Article on ‘Family Income Benefits’ by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women – we review many of the best Life Insurers UK selling Family Income Benefits Life Insurance in United Kingdom (inc NI)