Myself

Myself My

My My Income

My Income

How much is building insurance ? Broker helpIt's important to have sufficient buildings insurance to cover your rebuilding costs, but how much is enough?

How much Buildings Insurance do I need in 2026?

'Contents and Building Insurance'

Get Broker Only Deals

'What does Buildings Insurance cover'?

'What building insurance covers' should normally help protect you from these perils & provide peace of mind financial security;

- Damage by fire, flood, storms, subsidence, vandalism, heave, burst frozen pipes or vandalism

- It can help insure the physical structure of your building or optional any outbuildings

- ie; the roof, walls, floors and any building extensions

- Plus its fixtures & fittings ie; kitchens, bathrooms, wardrobes and other fitted furniture

If you are planning to buy your home then it is usually compulsory requirement for the mortgage finance lender. You may not be able to get one unless you take out adequate buildings insurance, unlike mortgage life protection.

So what does a home insurance cover can be either building & contents insurance separately, or as just one combined policy. Don't automatically assume if you have one, then you have the other.

Usually combined policies may include a discount for buying these 2 elements together, although this still may not be the cheapest. However, for some it can also help make life easier administration wise, should you have to claim.

How much Building Insurance do I need?

For some Insurers, you need to be able calculate the amount it may cost you to rebuild your home from scratch. This is known as the buildings ‘sum insured’. We will explain how our Broker Deals can help you here.

So you should insure your buildings for the full amount it may cost to rebuild ie; from its foundations upwards at today’s costs

Note: The cost to rebuild your property is usually less than its open market value, as it doesn’t include the value of the land it sits on.

This rebuild value should include expenses such as the surveyor's & builders professional fees, not just the cost of any materials

How much is Buildings Insurance for some insurers estimate this cost for you based on the number of bedrooms you have ie; known as a ‘bedroom-rated’ policy.

And other Insurers may simply provide an unlimited value range for their property owner insurance eg; upto say £500,000 or £1 million.

As such, you don’t need to therefore waste time trying to calculate the rebuild for how much is buildings insurance costs.

This is our preferred & simplest method as Insurance Brokers, with £1 million Buildings cover quoted as standard for underwritten insurance

What Home Insurance do I need?

Stuff to bear in mind for property owners insurance:

- Non-standard construction properties rebuilding costs can be higher eg; Thatched roofs

- Home Improvements, like extensions & conservatories will likely increase your rebuild costs

- Building inflation costs

Most Building Insurance UK policies are index-linked, meaning they adjust to reflect any inflationary increase costs. It’s important to check this when you renew your home insurance policy, to make sure you have enough cover.

Climate Change & How much is Building Insurance going to be?

As we are all aware the earth's climate is changing, you only have to watch a Sir David Attenborough documentary & regular news to understand what this could all mean.

The UK long range weather forecast is likely to be more extreme events of flash flooding or heatwaves. How much home insurance cost in the future will therefore be affects everyone looking to protect their property.

These more extreme weather conditions are set to become more common, so potentially causing more damage to our homes and contents.

What happens if you live very near to water? What if you can’t find any affordable buildings insurance or the Insurers refuse to offer acceptable terms?

As Insurance is all about managing risk, Global property insurance premiums are forecast to rise by 22% by 2040 as weather-related catastrophes become both more intense & frequent.

House Insurance Building and Contents re Climate Change

What is Accidental Damage Building Insurance?

Accidents happen, particularly if you have young ones!

Home insurance accidental damage is classed as a sudden or an unexpected damage to your buildings or contents by an outside unforeseen event, that is unintentional eg; drop or spill that bottle of red wine & stain the cream carpet.

It is usually included in buildings or contents insurance policies. On some comprehensive home insurance how much is standard or home insurance accidental damage is sold as an optional cost extra).

You can get accidental damage cover for your possessions as well as for your building. Just because you have one, don’t assume for any property owners insurance you’re covered for the other.

Buildings Insurance How Much ?

Accidental Damage Cover

Note: Without accidental damage insurance, you will have to cover the costs of any repairs needed or replacements. So home insurance with accidental damage is a valuable benefit.

How much Building Insurance Exclusions?

How much Buildings Insurance exclusions are applied can vary depending on your provider and type of policy eg; Is it a budget or comprehensive policy.

Common exclusions on property insurance policies include:

- General Wear and tear

- Damage caused by neglect

- Poor workmanship

- Storm damage to some exterior fittings

- Frost or fungal damage to outside pipes & brickwork

- Damage caused by Pets, vermin, insects or birds

- Matching sets if one part only is damaged

- Damage by any lodger or paying guest

- Building work damage from any alterations

"How much is Buildings Insurance"?

How much is Building Insurance ?

'Home Insurance How much'?

How much home insurance you have will also depend on the type of property you have and the value of your contents. It will also depend on the amount of cover you need and if you add on any optional extras.

*Comprehensive Cover

Will cover your buildings & contents & include accidental damage. Home Emergency & Legal Expenses. It is likely to have a low excess eg; £50

*Budget Cover

Budget Home Insurance how much buildings & contents cover varies here but probably won't include accidental damage. It is likely to have a higher excess eg; £500

Unsure which home insurance or content and building insurance is best, then please contact us.

What does it mean if your Insurance Policy has an excess of £500?

*What is an excess?

The excess is the sum of money you must firstly pay upfront towards your home insurance how much per claim on your policy T&C's.

Your excess is usually a pre-agreed amount before any claim is paid out. Your insurer will then help contribute the rest (up to the limit of the agreed insurance cover).

There are usually 2 parts of your buildings insurance excess you may need to consider if getting any quotes for building insurance:

- Compulsory Excess (decided by the insurer & usually fixed)

- Voluntary Excess (chosen by you & so flexible on what can afford to pay & receive at claim)

So what does it mean if your Insurance Policy has an excess of £500? It means if you make a claim, your insurance provider will then deduct this £500 excess from the total payout you receive.

eg; if you have a £500 Insurance excess and make a £2,500 claim, your insurance company will then just pay £2,000 towards your claim, so you must find this £500 yourself from your savings.

However, the higher the policy excess, the cheaper the insurance premium will be. Conversely, if the policy excess was only say £50, then the premium would be higher, as the Insurers risk is now higher.

Your Home maybe your most Valuable Possession after your Loved Ones ?

Top 7 Home Insurance Claims*

- Escape of water 25%

- Fire & explosion 20%

- Theft 15%

- Domestic subsidence 5%

- Accidental damage 10%

- Weather 10%

- Other domestic claims 15%

How much is Building Insurance & Home Insurance Statistics*

- UK Insurers pay out average £8m daily for both home insurance & commercial claims

- Over 1.2 million buildings insurance claims are made daily

- Buildings Insurance UK claims have average 80% acceptance rate

- Zurich & Aviva average claims payout ratio is 96%

- The average UK buildings & contents insurance policy is £160

Building Insurance for Mortgage

building insurance best

'Mortgage Building Insurance' & 'Building Insurance Exchange'

Your mortgage lender will legally require you to have adequate for 'mortgage buildings insurance' in place, as soon as you exchange contracts on a property.

At that stage (not completion...as some people think) you’re then legally responsible for the property re building insurance house exchange & so how much is building insurance in place.

Even if you don’t have mortgage or its repaid, it is still advisable to maintain a buildings insurance policy. Unsure which home insurance or 'quotes for building insurance' are best, then please contact us.

If you’re just renting the property, you won’t need buildings insurance. However, it will be up to your landlord to have sufficient home insurance how much cover adequately protects you eg; fire in your rental property leaving you homeless.

How much Building Insurance for Extension?

Costs for building insurance for extension may vary. Some Buildings Insurance may automatically include coverage for an extension up to say £75,000 as standard.

This means you maybe covered for both your existing property, plus the new structure, materials & liabilities. We strongly recommend you talk to your existing Insurers & advise them of your building extension anyway ie; never assume you are insured.

Note therefore further buildings Insurance will need to be added if your providers request it.

Building Insurance for New Build

Building insurance for new build is different than building insurance when buying a house that already has been built ie; you are now the first person to make that house your home.

You may have just bought a new build house from say some of the top 10 UK house builders like...

- Barratts

- Persimmon

- Bellway Plc

- Taylor Wimpey

- Berkeley Group

- Redrow Group

- Vistry Group

- Bloor Homes

- Countryside Properties

- Cala Group

This could mean it is harder for some to easily get online quotes home insurance new build no postcode as yet known.

Many Mortgage finance providers may not lend on any new build property unless there is a NHBC Buildmark warranty in place.

Note ideally most new build homes should therefore be legally protected against any structural damage for up to 10 years.

UK House builders that are registered with the NHBC must comply with certain building standards for their work to be covered by the 10 years Buildmark warranty.

However, this 10 year structural warranty is usually split up into 2 periods.

Period 1

- This initial 1st period lasts for 2 years

- Your builder must correct any issues that arise during this time

- These could include your windows leaking or your heating system breaking down

Period 2

- The 2nd period then lasts from years 3 upto 10

- During this period, your builder or developer is then only obliged to rectify major structural problems

- These include the foundations of your new property, any external rendering, load bearing floors & walls, plus your roof

- If any smaller complications arise during this time, eg; issues with fixtures & fittings, guttering etc; you may need to fix these yourself

- The same goes for any problems occurring due to normal wear & tear, weather damage, or any lack of normal maintenance.

Generally though if looking for home insurance for new build properties it is often a little bit cheaper compared to an older property, with the same number of bedrooms.

Why? Well that is because, more often than not, new builds come with brand-new plumbing, electrics & roof fittings etc; so Insurers note you should be less likely to make a claim on your buildings insurance.

Also, higher standard safety features may mean that any break-in is less likely. All of this can result in generally cheaper 'building insurance new home' premium costs.

However, people searching on the web for building insurance new build could also mean they are building that house themselves from scratch on a new or existing plot of land ie; self build insurance.

'Self Build Insurance'

Self build insurance is a specialist buildings insurance that protects your new property whilst that building is still under construction.

If you are building a brand new property then any standard buildings insurance for new build policy may not be enough to fully insure you.

Any building sites will naturally come with extra insurance risks, so you will need the correct insurance cover to stay protected.

'Self build insurance' will help protect you against damage to your new property whilst under construction plus cover tools & equipment used, alongside plus public & employer’s liability.

Check your buildings insurance policy if you are covered for a self build garden room or self build garden office. Unsure do you need building insurance for a new build or when to get home insurance on a new build?

Compare broker new & self build 'quotes for building insurance' please contact us.

What does Martin Lewis say about Home Insurance?

What's Martin Lewis say on Home Insurance? Well here are Martin Lewis home insurance 8 top tips:

- Never auto renew your Buildings Insurance (shop around)

- The cheapest time to renew (start looking around 21 days beforehand)

- Save & switch midstream (but factor in cancellation costs)

- Cover re buildings insurance costs only (not home market value)

- Invest in better locks & security (may reduce premiums)

- Check out multi-policies (save on both home & car insurance)

- For cheapest buildings & contents cover (pay annually)

- Check if quote includes add-ons (did you want legal cover)

In conclusion, consider what does Martin Lewis say about quitting Home Insurance before taking any action. Always speak to a broker if unsure which home insurance best for you.

'Martin Lewis Home Insurance' on Rules Change 2022

Martin Lewis home insurance changes comments from 2022 that new FCA insurance rules aim to end the No Loyalty premium.

This meant those who renewed their loyally insurance each year, then payed more than new customers who switched as they are offered cheap home insurance prices to do so.

UK Insurers must now prove, on aggregate, they charge both new & existing customers getting insurance via the same 'channel' very similar price, including any voucher deals or cashback.

Martin Lewis contents insurance home or buildings cover annual renewals says this is ideal for those customers who do not want to switch, or do, but do not want the hassle.

In conclusion, home insurance Martin Lewis MSE expert always says shop around. Unsure which 'property owners insurance' is best for you, then please contact us.

'House Insurance after Death of Policyholder UK'

It is important to be aware what happens to 'house insurance after death of policyholder uk'?

Buildings insurance & contents are often immediately invalid after the death of the main policy holder. Therefore, even if you are a named person on a buildings insurance policy, often you will not be fully covered now on house insurance unoccupied owner deceased terms.

Please contact the buildings insurance company to make temporary arrangements. This could be until you maybe in a better position to make longer term insurance unoccupied house owner deceased decisions.

You will also need to tell the insurance company if a property will then become empty (see below re house insurance for unoccupied properties).

It is often best to remove any easily portable valuables from the buildings for safe-keeping elsewhere? This may also mean that you must inform your own buildings insurance company if you are looking after any valuable items now in your own home.

Unfortunately, if someone dies there is alot of paperwork to now do & things to arrange, and notifying Insurers & unoccupied house buildings insurance is just one of them.

'Probate Insurance' & Home Insurance for Executors

Probate House Insurance UK cover is designed for that period when a person has died & their house legally is being dealt with under probate.

As mentioned above, most standard household insurance policies will probably be voided if you leave a home empty & unoccupied for more than 30 days or more.

This could make it unsuitable for correct cover during any long & any lengthy complicated legal probate proceedings re home insurance for executors.

Without getting specialist probate house insurance cover, any empty property naturally could be leaving that building incorrectly protected against any damage or vandalism.

This could then risk your probate job role further from any estate claim costs & complications and as discussed in probate insurance money saving expert forums.

Probate insurance property cover is designed to help whether you are a named legal executor or other professional, making it easy to keep unoccupied homes protected.

Insurance for Unoccupied Buildings

If your property is left unoccupied for any extended time period, you often must let your Insurance provider know re any insurance for unoccupied houses.

It is something people often forget to do re advising building insurance empty property insurers, if they are going abroad say for a long break.

However, any best insurance for unoccupied properties uk deals was a hot topic for discussions especially during the recent Pandemic ie; people may have been unable to return to their home.

Insurers may need to adjust to insurance for unoccupied buildings & there could be some restrictions put onto how much building insurance for unoccupied homes is allowable.

Most insurers will cover your home re any 'unoccupied home insurance' on the condition that it may not be left unoccupied or unattended for usually no more than 30 consecutive days. So if you have gone away on holiday for longer than this, then it could they void any unoccupied house insurance T&C's.

Often during the winter, some Insurers note on building insurance unoccupied due to higher risks of colder temperatures on burst pipes etc; They may also even reduce the number of days you can leave your home empty for, down to say a couple of weeks or lower.

Need broker help - Looking for house insurance for an empty property?

Home Insurance 90 days unoccupied

Some insurers may offer 'home insurance 90 days unoccupied', rather than the usual 30/60 days in their house insurance uk unoccupied T&C's.

However, as brokers we could access more specialist home insurance available that may provide extended covers for these longer time unoccupied risks.

So any existing home insurance provider may be able to provide some cover while the property is unoccupied upto 90 days, but beyond that you may need to seek out buildings insurance cover elsewhere.

Need broker help - Looking for home insurance on empty properties?

House Insurance Empty

Martin Lewis Unoccupied House Insurance

In many Insurers T&C's, MSE 'Martin Lewis house insurance' hints & tips mentions they could state you should also keep your heating & water on at a minimum required temperature for example (even during cost of living crisis).

The reason being here MSE Martin Lewis unoccupied house insurance says is to reduce the incidence of any burst pipes and the damage claims this may then cause.

So if you intend to go away for that post pandemic trip of a lifetime to Australia for several months, be sure to notify your Insurers to switch over to unoccupied buildings insurance.

Should you be away for longer, or someone has died (see above re unoccupied property home insurance) then notify insurance companies how much time the building will likely be unoccupied for. This will ensure you have a correct 'buildings insurance unoccupied' terms.

Martin Lewis home insurance claim says leaving it empty for long periods Insurers would state makes you more at risk of burglary, and so the cost of any claims greater as any damage can be left undetected for weeks on empty house buildings insurance.

Need broker help - Looking for home insurance for an empty house?

What Landlord Insurance do I need?

Landlord insurance is designed to protect both your rental property & contents. Also alternative accommodation for tenants if they cannot stay in your property. Private Landlords and Lettings Agents can also protect their rental income against a tenant failing to pay their rent.

How much does Contents Insurance cost?

How much does contents insurance cost will naturally vary - dependant upon the value of your contents.

It will also depend on whether it is combined with 'building insurance home' also (so you may receive a multi-plan discount on how much does building and contents insurance compare cost together).

Or, alternatively a standalone policy (so maybe more expensive) will affect the average price for contents insurance.

A recent survey done by Admiral Home Insurance revealed that both UK homeowners and renters may be undervaluing their contents insurance.

When they asked 1,000 people to estimate the total value of all their contents within their property, the average figure came out at £18,333.

However, Admiral point out that is £16,667 less than the average house contents value of £35,000*.

Their survey states that. 2 bed flat average contents value = £27,956. 3 bed house average contents value = £41,056. Bungalow average contents value = £44,158

So the 'average contents insurance cost' will depend on Insurers & property type.

How much Building Insurance Cover for Contents?

Like how much building insurance is needed, it's probably just as important you correctly estimate how much your contents could be worth.

If you ever have to replace them, you should have enough contents insurance to fully cover your losses.

Which home insurance you choose will ask this question both at application & claim.

Home Insurance how much Contents Valuation?

- Make a list of items in every room of your home, including the attic and garage

- Work out how much roughly it would cost to replace each item with a new one

- Tot up the full cost of all your items to get your total estimate

- Contents are all items that if your turned house upside down would then fall out

Note: Valuables like antiques or jewellery may require a professional valuation. At the point of claim, Insurers may require proof of purchase or valuation.

Most content home insurance uk policies have limits on how much you may claim per single item.

You may need to add extra cover for any items that exceed this limit or take away from home.

What is Home Insurance Coverage FAQ

*Does Home Insurance cover structural problems?

'Does home insurance cover structural problems'? If your home has suffered any structural damage or movement, it then means either the walls, foundations, roofs, floors have been compromised and so becomes unstable.

Problems like ground settlement, heave or subsidence can especially affect building foundations and walls.

So does Buildings Insurance cover subsidence?

Subsistence often usually occurs when the ground beneath a building sinks, pulling that property’s foundations down with it. It happens when the ground loses moisture and so shrinks due to prolonged dry spells, or the presence of trees and shrubs which cause the soil to lose its moisture.

So does home insurance cover subsidence? Insurers may cover you for accidents like fires & floods, as well as subsidence and ground heave.

However, often settlement however is a different matter. It is not usually covered as standard building insurance feature, nor any long-term structural damage that has been developing for some time ie; you are aware & have not maintained your property accordingly.

10 warning signs of impending structural damage

- Wall cracks

- Lintel cracks

- Window sill cracks

- Wall gaps

- Floor gaps

- Bowed bulging walls

- Nail pulls

- Doors sticking

- Windows stick

- Woodworm

*Does Home Insurance cover roof leaks?

'Does home insurance cover roof leaks'? Your buildings insurance may cover you but usually only if that leak was say caused by say strong winds, rain or storm damage to your roof.

As such, you may expect to see signs of damage to the roof eg; lots of missing roof tiles. If that is the case, you may be covered by your buildings insurance policy (after the Insurer has fully checked your claim).

However, if it is just a few slipping tiles (caused say by birds) and that you have not dealt with accordingly over time, and so then your roof is now letting in water. That means it is unlikely your home insurance covers roof leaks, as this is due to more common wear & tear, so you will have to pay for any repairs yourself.

*Does Contents Insurance cover leaks?

'Does Contents Insurance cover leaks'? Yes, many Contents insurance policies will help cover damage caused by a leak from say a fixed appliance tank or pipe to your items ie; leaks onto curtains, carpets or sofas.

More comprehensive Buildings Insurance will also help cover the costs of removing or replacing any part of the structure of your home to find the source of a water leak so repairs can be carried out.

Check this out and ask our brokers the question when doing insurance home and contents comparison.

*Will Home Insurance cover Water Damage?

So Will home insurance cover water damage or will home insurance cover water leaks?

Water damage to your buildings is often covered as a standard feature within a buildings insurance policy T&C's. However as always, check what your plan does & doesn't cover

In the insurers T&C's it is often referred to as an ‘escape of water’. This can be caused by several issues, from an overflowing or blocked loo, burst pipes due to freezing winter temperatures or a leaking dishwasher.

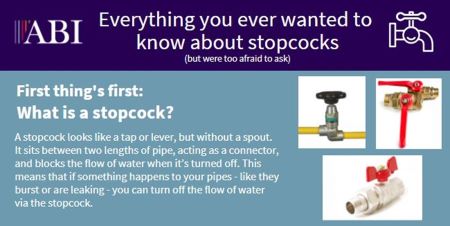

Escape of water damage or water leaks according to the ABI one of the most common types of domestic property damage insurers claims. They state that typical payouts are around £1.8 million daily.

The ABI advise some of the following tips to help avoid this via a professional plumber...

- Consider them fitting a leak detection device to check Stopcocks & Pipes

- Consider what you are putting down your drains

- Check regularly for leaks from taps, toilets, sinks, baths & showers

The bottom line they state is don't ignore any early warning signs & use your water meter to check for trace and access for leaks (if you can easily find it).

*What is 'Trace and Access' Insurance?

'What is trace and access cover' on buildings insurance? Trace & access is a term used by insurance companies to help cover (as the name implies) the costs of tracing and accessing any hidden water leaks.

This is never easy, as water often has its own way of finding where to go ie; a leak may be traced onto the right side of the property but its source maybe on the left & well hidden away from any easy access.

Some trace and access insurance policies cover the full cost of repairing the water leak, other trace and access cover plans may contribute towards any overall trace and access cost.

If you live in hard water areas, this can be a common issue so insurance trace and access could be harder to get.

It would then require a specialist trace and access plumber to come out to do full trace and access leak detection, which can be time consuming & costly.

Again it often boils down to good home maintenance & wear and tear as to whether any trace and access claim refused by Insurers.

*Does Home Insurance cover Cracked Render?

Rendering is the process of applying a cement coat to the external walls of a property to make them either smooth or textured as desired. Rendering helps make a wall more durable by making it water repellent.

The difference between plastering & rendering is that plastering involves the interior walls & rendering involves the exterior walls.

So Does home insurance cover cracked render? Most Insurers may just class this as wear & tear and you can't claim for damage caused by every day wear and tear. As such, fill or replace any faulty render.

*Does Home Insurance cover boiler?

'Does Home Insurance cover boiler' is an often asked question because a boiler is an expensive item to replace.

A boiler is often one of the most used appliances in your home, like your fridge, freezer and kettle. However, a domestic Boilers lifespan is not indefinate and so may last 10 years+ only if well maintained & serviced.

In many cases, a home insurance will not cover the costs of fixing a broken boiler or replacing it. Boiler breakdown is very common thus affecting most home insurance company T&C's.

Plus due to the ongoing cost of living crisis, this is often due to lack of regular maintenance. So naturally many building & contents insurers are concerned about offering standard cover for insuring against repair, replacement or breakdown.

However, Insurers may pay instead for any damage caused by the boiler eg; damage caused by leaks from a boiler.

Note; You may be able to take out seperate cover with your home insurance provider that does cover things like your boiler ie; under their ‘emergency home cover’.

Emergency Cover Insurance for Home

'What is Home Emergency Cover'?

'What is Home Emergency Cover'? It covers you for any immediate urgent issues with any services that supply your property eg; electricity, water or gas.

Some homeowners insurance plans offer this optional benefit into their buildings & contents cover

- It usually covers your central heating & boilers, electrics, security, roof, pests or plumbing

- eg boiler breakdowns, blocked drains, burst pipes, electrical failures

- Policies may also include cost of any call outs fees, repairs, parts and labour

- 24/7 service for help when you need it

- Home emergency cover may not cover any cost of repairing the damage caused but just fixing the problems (that other part should be covered under your main policy)

So what is home emergency cover on home insurance will vary between insurers. This benefit can a very useful way of you accessing a tradesman via the Insurers, rather than calling round locally.

As always, check what is & isn't covered here on how much is buildings insurance, if also asking do I need home emergency cover on home insurance?

Note: Some banks or building societies may offer emergency cover insurance for home as a rider on their upgraded packaged current accounts ie; check you are not doubly insuring yourself on any homeowners insurance.

Does Home Insurance cover Mobile Phones?

Does Home Insurance cover Mobile Phones? As the majority of us now use & rely 100% on their phone, naturally if you lost it or it got damaged, you may query if your home insurance cover mobile phone.

As the price of the latest mobile phones are often into the £100's (often sold on contracts) the cost of replacing any broken or damaged phone can be expensive.

Most home contents insurance will cover your mobile phone - but only when it is in your own home, just like your other personal valuables & belongings.

Unless you have away from home contents cover, this could be an issue especially if it was lost, dropped, stolen or damaged whilst out and about, as many carry our phones with us 24/7.

However, most standard contents policy will also apply an excess & perhaps if are trying to save money, this excess could be higher than the phones value?

If you are on a phone contract, then it would be worth investigating if that specialist mobile phone insurance terms & excess could be more beneficial.

CONCLUSION How much is Buildings Insurance?

We have therefore examined why home insurance is important as more than anything else it helps protect the roof above our heads. We all need somewhere to live.

In conclusion, 'How much is Buildings Insurance' is not always simple to price and quote for due to the number of options & rider variations as to which home insurance company is the best.

As you can see, what home insurance covers like any type of insurance, then usually you get what you pay for.

If your policy is budget cheap but not cheerful, then often the buildings or contents coverage can be very basic. So bear this in mind when doing any comparison building and contents insurance quote.

Unsure? Then let us shop around the market for your ideal building insurance comparing best 'home insurance with contents' broker deals.

'How much is Building Insurance' Article by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women average cost - we review many of the best brands selling Buildings Insurance & Life Insurance in UK (inc NI)

|  |  | ||

|  |  |

QUOTE For: Contents and Buildings Insurance | Landlords & Trades

*For products with any investment element we may introduce you to an FCA authorised adviser after any further review. We may also introduce you to other selected professional partners for other protection, finance (such as a whole of market mortgage broker) or legal products as deemed appropriate. By completing our enquiry form you ‘may be introduced to another lender/provider’.