Myself

Myself My

My My Income

My Income

Article on Life Cover and Critical Illness

Critical Illness Life Cover

Life cover and Critical lllness. Broker help.

Why get Life Cover and Critical Illness Insurance?

Critical Illness Life cover is an insurance policy that pays a tax-free sum – if diagnosed with an Insurers specified conditions or death.

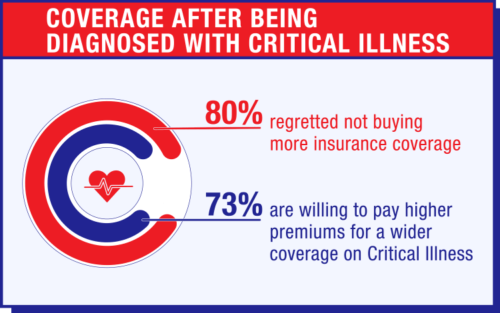

Sadly, the chances of you or me needing to make a claim are quite high in our working lifetime and maybe before retirement.

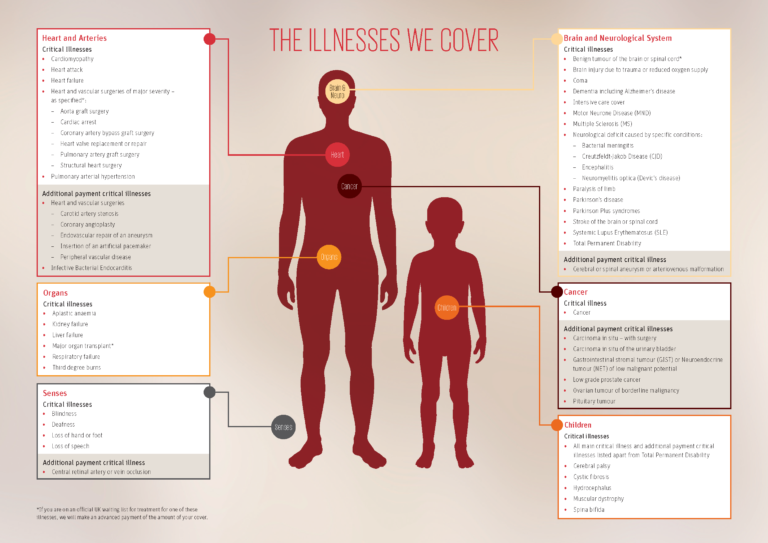

The Top 3 Enemies

Someone’s Life may change in just a Few Seconds…..

Someone’s Life may change in just a Few Seconds…..

* Timeline stats

Every few seconds, someone in UK is sadly diagnosed with 1 of these 3 health issues.

Most Insurers therefore base their life cover & critical illness insurance plan benefits around the severity of these top 3 claims.

Main Types of Critical Illness Policy

All Uk Insurers do vary their critical illness plan terms ie; shop around when doing ‘life and critical illness insurance quotes’ as cheaper may not mean better

- Basic plans covering just 1 area like cancer eg; well woman cancer

- Or just the 3 core conditions – cancer, heart disease & stroke

- More comprehensive plans covering 40 + illnesses or 60+ illnesses or 100 + illnesses

- Plans that may enable just 1 main claim and then end

- Or Severity % based enabling multiple part payments upon diagnosis

- Fixed Premiums or Reviewable Premiums plans

- Lump Sums or Family Income Benefits option

- Plans that include free child cover or a paid for extra

- Ignore Life Insurance with Free Gifts deals, their critical illness plans are basic

- Generally these could also be £1,000’s more lifetime expensive

As such, please speak to our Professional Brokers before you consider taking out new cover to get your ideal life and body cover insurance plan (or indeed trying to replace another).

Chances of you needing to make a Claim?

- Life Cover 1 in 10

- Critical Illness 1 in 3

- Income Protection 1 in 4

- Total Permanent Disablement 1 in 20

During the Pandemic, those life cover and critical illness insurance statistics were naturally re-adjusting daily…Unfortunately, not for the better ![]()

3 Options | Life Cover with Critical Illness

1] Life Cover AND Critical Illness

(2 Seperate Plans)

When considering “life cover and critical illness” insurance, you need to understand your insurance risks. As you can see above, your chances of being critically ill first are quite high.

Therefore the chances are you are more likely to be diagnosed critically ill first in your lifetime, than you are to die from say an accident.

As such, the cost of Critical Illness is much more expensive than the price of life cover alone. So for example, if £100,000 lifecover only was £10pm, then having £100,000 critical cover could now cost £40pm ie; Typically 4 x the price.

Check out your Broker personalized deals and costs: Online Critical Illness Life Cover Quotes

*Critical illness claim first, what happens then?

In the event of a critical illness claim first, it is more than likely an Insurer could then refuse to offer you anymore affordable underwritten insurance life cover.

They would consider you to be too much of an insurance risk for the short term future and then either decline or postpone offering you anymore protection cover terms.

The Insurers decision stance may only possibly change several years down the line. If so, they then only offer very ‘heavily health rated insurance terms’ eg; Was £25pm but now £100+pm.

So by having to buy a separate critical illness policy plus standalone life insurance, you avoid this dilemma. Should you unfortunately now make a claim, you still have peace of mind of your back up plan life cover to rely on. Many Insurers also offer a multi-policy discount, so this 2 plan approach can work out a little less expensive.

Also for administrative and claim purposes, it sometimes makes sense to have all policies under one Insurers roof in the event of a claim, rather than via different Insurers.

If you are married or living together, you may even decide to each have 4 x separate life cover and critical illness insurance policies instead. Consider this if doing ‘life and critical illness insurance quotes’ here.

Conclusion

As you probably guessed, by going down this route it is more beneficial to you in the event of a critical illness claim but also more expensive.

2] Life WITH Critical Illness Cover

*(One combined plan)

You may decide for budget reasons that the above options are not suitable for your situation. eg; You are protecting your mortgage and feel that a ‘one off payment’ is enough.

It means potentially any payout would be on a 1’st claim basis. If you are critically ill first, then you may have no cover afterwards.

This is known as ‘accelerated cover’ rather than ‘additional cover’. However, all is not lost given the type of critical illness plan you take out.

As mentioned, a cheaper budget life and critical illness insurance plan may just payout upon a claim and then end. A more comprehensive plan with serious illness cover enables potentially multiple claims.

Note: You can also buy standalone critical illness cover only – that doesn’t include any lifecover eg; single with no dependants.

For example, you take out policy cover for £100,000. You are then diagnosed with a low grade non-invasive cancer and the Insurers pays you out £25,000.

Unfortunately, several years later on this now turns into invasive grade cancer. The Insurers now may either payout £75,000 ie; the balance, or some may payout the full £100,000.

For most Insurers (around the world) it is for human’s Top 3 Enemies ie; specified cancer, stroke and heart attack happens more often than you think.* (Vitality Stats)

3] Critical Illness and Life Cover

*(Buy Back Option)

In this scenario, should you make a critical claim first, instead some Life Insurers allow you to ‘buy back your lifecover’. Note: This is a paid for policy benefit and must be done from outset.

This means rather than having 2 x separate life and critical illness insurance plans from outset, you choose at time of need and without further no medical underwriting, wether to now buy a new lifecover policy. This initially sounds like it could be the cheaper route ?

However, when you take out the new policy, it will be based upon your age at that time ie; likely more expensive at that time, as you are say 25 years older.

Martin Lewis on critical illness suggest consider as a rule of thumb ’10 Year Rule’ of Annual Salary.

Conclusion

This route might be preferable and still offering you peace of mind when doing life and critical illness insurance quotes. Particularly if you feel your circumstances will still need another life insurance in the future but don’t want 2 separate plans now.

Critical Illness and Life Cover for Mortgage

So having established your 3 different options above, which critical illness and life cover for mortgage is your preferred repayment protection option?

Option 1: Critical illness and life cover for Mortgage (2 x seperate plans) would allow you to use some, or 100% of the money, to repay the whole mortgage if diagnosed with a critical illness. You could then be left with a mortgage life insurance that maybe a decreasing policy and no mortgage now, or perhaps a much smaller mortgage.

The Importance of Split Trusts?

Writing a policy in trust is good way to help protect your family’s future in the event of your death. By putting the life insurance part of the plan in trust helps ensure your family or other beneficiaries receive their due inheritance.

Example: You sadly died in an accident first, rather than making a critical illness claim.

However, this specific type of trust also splits out the critical illness cover first for your own personal benefit (which is why it’s called a Split Trust).

It also ensures any remaining death benefits are held in trust for their beneficiaries if you died first.

Trusts are an acknowledged HMRC legal arrangement. The trust should be managed by ideally more than one trustee eg; direct family member, friends, or a legal professional.

The benefits of writing Life Insurance in Trust?

- Protect your beneficiaries from potential Inheritance Tax IHT

- This ensures it should go direct to you nominated beneficiaries via the trustees

- It may also help to avoid probate delays & inheritance tax – by falling outside your estate

- This applies even if you have made a valid up to date uk will

- Without a suitable protection trust, the life policy could fall back into your estate

- Choose who you want the lifecover part of the plan to go to

Child Critical illness cover

We don’t want to think about our children sadly suffering a serious illness or worse. As such, most Insurers now include child cover within an adult plan (but most not as a stand alone plan) for a child meeting the Insurers definition.

However, an eligible claim by a child will not affect an adult policy claim during their plan term. Ask us about this if doing comparison life and critical illness insurance quotes.

Some UK Insurers have child cover benefits free inclusive and others you can be paid for ie; not being charged extra if you have no children.

Any benefit paid out will allow you the parent to take any time off of work to help care for them. It may also allow you to get more treatment options that are not covered by the NHS, or allow your family or hopefully on recovery, take a precious family holiday.

Life Cover and CriticalIllness

Typical Child Eligibility | Key Facts

- Natural, legally adopted or stepchildren, plus any children you may have in the future

- The child is covered from 30 days old up to their 18th birthday (21st birthday if in full time education)

- Diagnosed with one of their specified illnesses during the term and survive for 14 days after their date of diagnosis

- Only one claim can be made per child with maximum 2 children

- £30,000 or 50% of your amount of adult cover, whichever is lowest

- Child Accident Hospitalisation Benefit due to physical injuries

- Family Accommodation Benefit paid whilst the child recovers £100 per night to £1,000 maximum

- If a parent, makes a valid claim, they will receive up to £1000 towards childcare costs whilst in recovery

- Child Funeral Benefit £5,000

- Exclusions – Usually the child’s condition is present at birth ie; pre-existing condition

Life and Body Cover Insurance

Sorting out your ideal life & critical illness insurance cover may sometimes seem a difficult task, so don’t do it alone.

It’s always a good idea to get professional advice from an expert if looking at life and body cover insurance – we’re here to help.

‘Life Cover and Critical Illness’ Article by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women – we review many of the best brands selling Life Insurance in UK (inc NI)

Check out these helpful Guides & Blog

‘BMI Calculator in KG’ (2026) High BMI Life Insurance >

Compare Broker High BMI Life Insurance Deals: August 2026 > Article on: Who BMI Calculator in KG BMI Calculator in KG | Calculator for Weight ‘BMI for Women Chart | BMI for Men Chart‘ BMI Calculator in KG. Calculator for Weight. BMI for Women Chart. BMI for Men Chart. Compare BMI and impact on Life […]

‘Buildings Insurance for Landlord’ (2026) Broker Deals >

Article on: buildings insurance landlord ‘Buildings Insurance for Landlord’ Buildings insurance for landlords helps you cover against damage to your building ‘bricks & mortar’ rental property (or multi properties) plus any fixtures or fittings for your tenants in 2026. Accidents & natural events can happen, so you the need peace of mind coverage for landlords […]

‘How much is Buildings Insurance’ & Contents? 2026 Broker Deals >

How much is building insurance ? Broker helpIt’s important to have sufficient buildings insurance to cover your rebuilding costs, but how much is enough? How much Buildings Insurance do I need in 2026? ‘What does Buildings Insurance cover’? ‘What building insurance covers’ should normally help protect you from these perils & provide peace of mind […]

‘Inheritance Tax in UK’ *IHT Life Insurance Best Broker Deals > (2026)

Broker IHT Inheritance Tax and Life Insurance UK Deals: 08/2026 > Article on: IHT Inheritance Tax in UK Life Insurance Inheritance Tax Uk . In this article, we will look at Inheritance Tax in the UK (IHT) rules and how you can use Life Insurance for Inheritance Tax purposes. You will see that there are […]

‘Life Insurance vs Life Assurance’ (2026) Broker Deals>

Compare Broker Life Insurance vs Life Assurance deals: August 2026 > Article on: life insurance vs life assurance Life Insurance vs Life Assurance …VS… Difference between Life Assurance and Life Insurance? As Life Insurance Brokers, we are often asked ‘what’s the difference between life assurance and life insurance‘. Back in the 1500’s, the word ensurance was contrived […]

‘Lump Sums’ Life Insurance Types? 2026 Broker Deals >

Compare Broker Lump Sums Life Insurance & Critical Illness Deals: 08 / 2026 > Article on: lump sums Meaning of Lump Sum? The meaning of lump sum with a life insurance policy, differs dependant on the types of policy. In this article, we will look at the benefits of 4 different types of life insurance […]

‘Underwriting for Insurance’ (2026) UK Broker Life Quotes > in Secs*

Compare Underwriting for Insurance Broker Best Deals: August 2026 > Article on: underwriting in Insurance What is Underwriting Insurance? What is underwriting Insurance? In short, ‘underwriting for insurance’ is all about calculating or balancing the risks of an exposure loss against making a profit for the insurance company. From this risk calculation, the insurance company […]

‘What is Life Insurance’? Compare Best Broker Deals >> Secs (2026)*

Compare What is Life Insurance Deals: 08/2026 > Life Insurance what? We discuss what 2 main types of life insurance what you may want to get. What Life Insurance Plans are best? We Compare Leading Uk Life Insurers. Deals from £5pm. Broker help We will now look into what’s a life insurance policy re disclosure […]

Average Life Expectancy UK? Calculate Best Life Insurance Deals >

Many People search ‘Average UK Life Expectancy 2026‘ out of curiosity… Lowest Ages: Men 73 vs Highest Age: Women 86 THE REAL QUESTION IS:“Would your Own Family be 💯 100% Financially Secure IF something Unexpected Happened?” *1/2 get Cancer in their Lifetime *500+ Parents still die every week *1/5 Men will Die = Before Age […]