Myself

Myself My

My My Income

My Income

Martin Lewis Best Life Insurance for Over 60's?

MSE Review: 08/2026

*5 Mins Read

Article: MSE Money Saving Expert Martin Lewis on Over 60 Life Insurance Guide

In this "Over 60 Life Insurance Martin Lewis" MSE review guide we will look at whether 🔸 Money Saving Expert thinks Over 60's Life Insurance is worth it? 🔸 How much Over 60 Insurance Life cover you need? 🔸 Broker Top Tips re Over 60's Life Insurance Money Saving Expert...

What Does Martin Lewis say on Over 60 Life Insurance?

Well firstly YES, Money Saving Expert Martin Lewis does overall '💯 100% recommend Life Insurance', especially if you still have any dependant's reliant upon you financially (whether they are old or young).

On the main 'Money Saving Expert Life Insurance' website section, Martin Lewis is then generally asked How much life insurance do I need? He doesn't put any age limits caveat upon this ie; whether a 60 year old or over after life insurance cover etc;

In their MSE review, we will therefore look at their overall guide on Best Life Insurance for Over 60's from several perspectives. Firstly, IF you still have "Financial Dependents".

Alternatively, perhaps any large debts that you wished help covering - like say Mortgage Protection still or an Equity Release lifetime mortgages, or for Inheritance Tax IHT? OR lastly, you perhaps only just want to provide a lump sum towards any final expenses costs?

Martin Lewis Life Insurance For Over 60s Guide

Looking for advice to help get the best Over 60's Life Insurance in 2026? If so, you do have a choice of seniors life protection options that Money Saving Expert have reviewed.

Firstly, from those over sixties british seniors being in overall good health still, then to those who have unfortunately poor health issues & so maybe reduced life expectancy.

Some UK Life Insurers in the last few years have therefore started to approach 💯 100% the Over 60's guaranteed life insurance marketplace, as the UK population are now living overall for longer.

Interestingly, the Money Saving Expert on over 60 life insurance Martin Lewis hasn't commented yet on specific age-related or branded over sixties life insurance products.

MSE in depth reviews are instead mainly focused on the very similar 'no medicals' Over-50's life insurance cover, which generally are more heavily marketed plans.

Or, they have provided guides instead on various term life insurance types, or basic reviews on whole of life insurance policy options.

All life cover products that are available to the Over 60's are designed to helping protect yourself, or those who are still financially dependant upon you.

The Money Expert says YES "Life Insurance is a Cheap Financial Lifeline" SO the ultimate choice is always yours, if the monthly cost's worth it to you & your family.

*MSE Guaranteed Over 60's Life Insurance No Medicals

Previously there was no UK life cover no medical questions products marketed specifically for the Over Sixty Life Insurance marketplace. But as mentioned, times are changing for Insurers looking to target both the over 50 & over 60's silver surfers.

So several Providers & Banks are now therefore offering to relevant customers direct, their Guaranteed Sixty-Plus Life Insurance deals.

These are promoted as an 'easy, low-cost way to guarantee a cash lump sum when you die' with 'No medical questions and no examination required'.

Targeting those who for whatever reasons, don't want any hassle in getting their life insurance in their sixties...

Note: These seniors Over 60 life insurance guaranteed plans are often just re-branded Over 50's lifecover - of which Martin Lewis is a 💯 '100% Fan...IF You've Poor Health & Life Expectancy' BUT not so, IF you have Good Health.

Martin Lewis on Over 60s Life Insurance

Many of these no medical over sixties seniors plans are usually sold direct, meaning therefore no advice as to whether it is or isn't the best life insurance deal for you (ie; dependant on your overall health & lifestyle).

MoneySavingExpert also doesn't really go in depth review into alternative Over 60's insurance cover options like fully underwritten whole of life assurance, other than to say these plans are often (but not always) investment-linked life policies.

Mainly MSE says whole life cover policies are used to mainly help mitigate inheritance tax, as the policy runs out when you die, instead of after a fixed time frame.

Which as brokers we would only agree to some extent, as they can have far more uses than just that eg; leave a legacy, help to cover funeral costs, protect those with interest only style mortgages etc;

Due to this, the Money Saving Expert website does point out generally whole of life cover plans are usually a more expensive option, which we will touch on further.

As such, as we get older there are still plenty of people always looking for any Martin Lewis over 60 life insurance cover advice here. So this is also an active topic in the Money Saving Expert website forum discussions.

We will look here therefore at some of your main Over Sixty insurance options. Then combine their various MSE life insurance guides & website tips, in this Martin Lewis best life insurance for over 60s review.

Martin Lewis on Life Insurance generally says for a good 100% rule of thumb in 2026, his Best Over 60's Formula is "NEVER BLINDLY BUY DIRECT" expensive policy offers via your Bank or one Insurer direct ie; Shop around or use a Broker.

Who's Martin Lewis - Money Saving Expert?

Background: Who is the highly respected Martin Lewis Lewis OBE & CBE? He is a very successful Financial Reporter & Money Expert, and the founder of the well known UK consumer website Money Saving Expert.

He also has his own current affairs TV Money Show on ITV. This was all initially broadcast after all the London Olympics back in autumn 2012.

Martin Lewis is now often seen on TV commenting on current financial matters & affairs. Or daytime TV like This Morning Martin Lewis being the popular go to person for sound advice.

In 2012, his popular Money Saving Expert website was sold to The Money Supermarket.Com group for reportedly £87 million. Since 2015, Martin Lewis remains executive chairman and in these challenging 2020's all round UK Consumer Champion & Finance Guru.

*Is Martin Lewis a Qualified Financial Adviser?

Having been regularly on our TV's for many years now - Some people may also ask, is the Martin Lewis a qualified financial adviser? The short answer is 'No he isn't'.

But interestingly, many people often turn to Martin's advice more than a real IFA. However, he often does stress the various information he provides - is not fully regulated financial advice.

Important Note: This overview on Money Saving Expert Martin Lewis on Over 60 Life Insurance blog is not a scam fake advert re Martin Lewis recommending our own broker services. As you may be aware he & MSE are fully impartial. Therefore, he does not endorse or support any particular products or providers. Any Martin Lewis Money video's or images shown may also have some out of date information on them - due to the ongoing cost of living crisis. Often these life insurance MoneySavingExpert articles may no longer be personally updated or written by Martin Lewis himself. MSE do state he oversees site content, especially the MSE weekly email. Naturally, although MSE is an independant website finance allows no advertising nor subscription, it may receive a revenue via 'affiliate links' to the top products or providers (which we aren't mentioned)

How much over 60 Life Insurance Martin Lewis?

Martin Lewis suggests for a good rule of thumb in 2026, his Best Life Insurance formula is using 'THE 10 x RULE' ie; aim to cover 10 x the Annual income of the highest earner or the main breadwinner until at least any kids have finished their full-time education or other financial dependants.

We would add IF retired and Over 60, consider also the financial impact on any younger partner and therefore subsequent loss of pension income etc;

What does Martin Lewis say on Over 60 Life Insurance?

'The 10 x RULE' = Formula For Success

However, MSE also suggests that to better help you to calculate a figure that may best work for you & your family based on your affordable monthly budget, it is worth ensuring any life policy should also help to cover these following 4 main finance items:

- Any Outstanding Debts that would need to be paid off eg; include any mortgage loans, unless covered by a separate life policy already

- Immediate Outgoings ie; what your dependants could need to regularly pay

- Future Spending you may have wish to make eg; further education & university fees

- Any Additional Expenses that your death may then trigger eg; funeral & final expenses costs

Note however; this MSE formula doesn't distinguish between does Martin Lewis recommend over 60 life insurance (or whatever age you are) but mainly seems to look logically at those with younger dependant children.

MoneySavingExpert do point out that this 10 x the highest earners annual income may seem a high amount, but they say it is likely to then leave enough money (after the impact of rising inflation) to help cover any increases MSE says for mortgage rate loan repayments, expenses or any ongoing childcare costs.

MSE states it could also go some way to help supplement the incomes of those left behind if they had to unfortunately then leave employment eg; to care for any dependant children or relatives.

Martin Lewis has sadly his own personal family history tragedy here to tell, when he lost his mum at only aged 11. This he has reportedly said it left him unable to leave his home for upto 6 years due to extreme social anxiety as he was growing up ie; he is perhaps commenting here on life insurance from some of his own personal experience background story.

Can you get Senior Life Insurance for the Over 60s?

Yes, all the main UK providers offer similar life insurance cover policies to those in their 60's, so don't worry here.

Even when you are over 60, the need for some form of life insurance protection is perhaps always there. There are currently 3 main types of Over 60 Life Insurance Martin Lewis discusses in their various guides.

Over 60's Life Insurance - 3 Main Options

Over 60's Life Insurance - 3 Main Options

- Over 60 Whole of Life Assurance (Yes > Medical & lifestyle evidence)

- Over 60's Guaranteed Life Cover (No > medical or lifestyle evidence)

- Term Life Insurance Over 60 (Yes > Medical & lifestyle evidence)

*Over 60 Whole Life Assurance (Medical Evidence)

General Key Features

- Whole of Life Assurance means you covered - even if you live until 125

- Policy is underwritten insurance Insurers ask medical lifestyle questions before offering terms

- Terminal Illness is often included for free on whole of life assurance plans

- This means you have 12 months to live, so pays out earlier 'death insurance claim' in advance

- Could involve GP reports & medical tests before agreeing underwriting terms

- Best deals usually available for those who have no adverse health or lifestyle issues

- Age at entry available up to late 80's dependant on Insurers

- If you have medical issues eg; high blood pressure or cholesterol Insurers may still offer cover

- Immediate coverage then with no initial exclusion periods before a whole of life insurance claim

- Suicide exclusion clauses may initially apply on whole life insurance for over 60s

- Own life, dual life or joint life insurance 60 and over upon death or terminal illness

- Plan options for fixed or reviewable premiums & must be paid for rest of life ie; until a claim

- Premiums maybe investment-backed ie; reviewable or guaranteed fixed

*Over 60 Whole Life Assurance (No Medical Evidence)

General Key Features

- 1 / 2 years exclusion periods before any natural causes death claims

- Usually no in depth medical & lifestyle questions to qualify

- Smoking status affects life insurance for over 60 smokers

- Accidental death claims only for initial exclusion periods

- Refund of premiums only if you died of natural causes during this exclusion period

- Insurers may stop taking premiums from age 90/95 but maintain your over 60 lifecover

- This Guaranteed Over 60 life insurance is whole of life meaning indefinate cover

- Age at entry usually upto 80 dependant on Insurers on a single life basis only

- Providers may limit fixed premiums per plan or total amount of Lifecover per person

- No investment cash in plan surrender values

- Lower life insurance levels generally offered versus other Over 60's plans

- Many use Over 60's plans instead of a prepay funeral plan

- Funeral funding benefit options with some plans

*Over 60 Term Life Insurance (Medical Evidence)

General Key Features

- Term Over 60 Life Insurance is 'underwritten' BUT for a fixed period ie; max available upto age 90

- Unlike whole life assurance you may live out that term period leaving no lifecover after

- Terminal Illness is also included for free on over 60 term life insurance plans

- May have much more affordable costs than whole life assurance as plan runs a defined term

- Age at entry available usually up to 85 dependant on Insurers

- Once underwritten, this life insurance policy has no initial exclusion period before claim

- Suicide exclusion clauses apply on term life insurance for the over 60s

- Premiums usually fixed and have to be paid for life of the policy term with no cash value

- Options of life insurance for the over 60s via own life or joint life policies

- Life Insurance upto age 90 as a 'bills back up plan' instead

Conclusion:

Many of the various Pro's and Con's Life Insurance features MSE comments on, will apply for those types of no medicals Over 60 life cover plans Martin Lewis also reviews on no medical Over 50’s life insurance.

Check out our > Broker Over 60's policies comparison charts...

Is Over 60's Life Insurance enough cover?

Being over 60, you could now be in a more senior position at your UK company? Let's say you typically earned around £50,000pa gross average salary. You are re-married & the main breadwinner.

You intend to carry on working until at least age 70 or upto age 75, as your youngest child may finish university or further education then.

By using that Money Saving Expert principle formula therefore above (ie; 10 x the annual gross income), MSE re life insurance Over 60 says you should maybe consider insuring yourself (assuming after any mortgage, loans & debts are fully repaid) for £500,000 or £1/2 million life insurance.

Interestingly, Money Saving Expert 'people also ask' here simply recommends insuring your gross income of £50,000pa & not net after tax income in this Over 60 Life Insurance Money Saving Expert 10 x rule example.

Following on from this simple Life Insurance Martin Lewis example formula above, if you then actually worked for the next 10 years from aged 60 until your intended retirement age 70, you could potentially earn over £1/2 million gross ie; £50,000pa salary x 10 years [or more with any future inflation wage rises].

As such, like the 10 x £50,000 gross salary Martin Lewis life insurance example - you could therefore alternatively protect your family and dependants with either;

- Income = £4,166pm or £50,000pa family income benefit FIB lifecover policy

- Lump sum = £1/2 million level term life insurance policy

- Or a mixture of the 2 policy types over the next 10 years - all dependant on your family circumstances

Neither of these examples also takes into account repaying any say mortgages, loans or debts. So factor those in as well into any over 60 life insurance calculator uk deals.

- You can decide wether you want the cover to be level or inflation linked

- Single plan | 2 x seperate plans | Joint life insurance 1'st claim | Lump Sums or Family Income Benefits options

What's Martin Lewis Over 60 Life Insurance policy?

What does Martin Lewis say concerning Over 60 Life Insurance and does Martin Lewis recommend Over 60 life insurance?

Well MSE recommends when considering any Life Insurance protection cover generally, he suggests these '7 helpful pointers' and need to knows for your family:

'Life Insurance Money Saving Expert' - 7 Main Need to Knows

- Go for Guaranteed Fixed Premiums NOT Reviewable Plan Premiums

- Disclose all Health Conditions & Risks to help avoid any potential non-valid claims

- 2 x single policies may sometimes be better than a joint 1'st claim policy

- Write your life cover policy into trust helps avoid the taxman & probate delays

- Switch & Save on existing cover eg; now quit smoking or health improved

- Your protected under FSCS if the Insurance Broker or an Insurer goes bust

- Over 60 Life Insurance Martin Lewis advice recommends you seek Professional Advice if unsure

Follow this advice & 'Martin Lewis How to save money' on life insurance tips with their MoneySavingExpert '7 Life Insurance Need to Knows'.

*No Dependants (So you don't need over 60's Life Insurance)?

MoneySavingExpert on life insurance says if there is no one you would want the money to go to, then don't bother.

Equally, they also say if you do have dependants' (but there would be little financial impact if you died), then you still might not need any life policy cover.

But if your income (or indeed pension) helps pay the regular bills, mortgage loans, food shopping and more would be a struggle, then life insurance is often a cheap way to solve that.

We would comment as financial advisers, that although you maybe an Over 60's single or have no immediate dependants currently, you could still have a mortgage loan or various ongoing debts & unpaid bills.

If you sadly died with current financial commitments, this means it could then leave your wider family struggling to cope with all the financial burdens you have now left them.

More importantly for us all...even paying for a proper funeral for yourself to now be dealt with. Where are these immediate final costs funds coming from?

Martin Lewis on prepaid funeral plans comments typically funeral costs could total around £10,000 including burial plots and headstones & rising.

Then further stress re creditor claims against the estate from the either the mortgage company, credit card or loan company etc; You may then ask that (even if you are single) is that fair & what you would want for your wider family?

*Poor Health & Over 60's No Medical Life Insurance

Martin Lewis remarks in his reviews that he spent most of the Money Saving Expert Over 50's guide ranting on about the dangers of these no medical style life insurance policies.

However he also points out... don't think every over-50s' policy (or similarly over 60's no medical lifecover plans) are a nightmare for every type of customer.

For example, MSE says if you have an already diagnosed serious medical conditions & shortened life expectancy, these no medicals life cover plans can be a good gamble.

The reason being is because MSE comments you do not need any medicals or health questions... other than smoker status to qualify (even though your life expectancy will be substantially lower).

Martin Lewis advises if you understand what you are doing, plus you have weighed up the risk pros and cons, you can win the no medical questions over 60 life insurance Martin Lewis remarks.

MoneySavingExpert give an Over 60's example where they take someone with poorer health (non-smoker) who at 65 is likely to live maybe another 5 years until age 70.

They say an Over Sixty person could take a typical advertised no medicals plan for less than £75 per month plan, which would pay out over £14,000 on death after the initial waiting periods (whilst they would only have paid in less than £4,500 .

In other words, MSE say they would get a whopping gain of over £10,000. If they died during year three, they say you would still just get back over five times what they have paid. Not a sum to be sniffed at.

Naturally, as brokers we would add that these figures are of less value if you lived longer 10 years plus. Also, as mentioned by us if you are of average to good health, no medical style Over 60's plans are not good value.

As brokers we would advise please don't confuse all these no medicals whole life type schemes - with other whole life plans available that say no medicals are needed...(but then they go on to ask you various medical health questions - to pre-qualify if you would get covered).

So let's look at the Pro's and Cons generally of over 60 insurance policies available with no medical questions versus those asking medical questions...

Over 60's Life Insurance

'NO Medical Questions' versus 'YES Medical Questions'

Over 60's Life Insurance 'NO MEDICAL' Info (Key Features) 'NO MEDICAL' Info (Key Features) | Over 60's Life Insurance 'YES MEDICAL' Info (Key Features) |

| * Poor value if fit & healthy | Ideal if fit & healthy |

| * Wait first 1/2 years before fully insured | Fully insured once terms agreed |

| * Some may include Terminal Illness | Terminal illness benefit included |

| * Accidental death only first 1/2 years | Fully insured once deal agreed |

| * Low lifecover levels available | Higher lifecover levels available |

| * No medical questions | No GP health check | Medical questions | Maybe GP health check |

| * Smoking / Vaping rates affects pricing | Smoking / Vaping rates affects pricing |

| * Short application process | Longer application process |

| * Good value if unfit & unhealthy | Lesser value if unfit & unhealthy |

| * Whole Lifecover | Whole or Term Lifecover |

| * Don't want any advice | Don't mind getting advice |

| * Funeral Funding Options | No Funeral Funding |

| * Miss premiums & plan may end | Miss premiums & plan may end |

| * Restricted premiums | No premium restrictions |

| * No investment risks | No investment risks on guaranteed plans |

| * Inflationary risks if level cover | Option to index your lifecover |

| * 1 provider only choice | Choice of Brokers marketplace |

| * Advertised by a Celebrity | Usually not Celebrity advertised |

| * May get a Free Gift or Pen | May not get a Free Gift or Pen |

| * Could pay in more than premiums | Less likely to pay in more than premiums |

| * No premiums after ages 90/95 | Premiums paid for whole of plan |

Your 60th birthday like your 50th is usually always a cause for a Big Birthday celebration milestone. Hopefully, you have many more active years left & in good health, even though you could be approaching UK state retirement age.

Those in their 60's could still be in full-time employment, which is useful given the costs of living crisis 2020's affecting us all. Maybe you have no intention of retirement for many years yet?

Therefore, given the rising costs of living, you could still need to consider life insurance to help protect any lost ongoing income or help cover loss of pension rights?

However, apart from looking after their own kids financially growing up, The Bank of Mum and Dad or indeed Grandma & Grandpa - may still need help to pay-off their own existing mortgage payments, outstanding debts or credit cards.

MSE - How to buy Over 60 Life Insurance?

The Money Saving Expert Martin Lewis website is always advising about how to save costs & getting the best value deals.

Whilst this may seem true, the Over 60's life insurance marketplace is more confusing, as it isn't as highly advertised and so focuses instead more on branded Over 50's lifecover plans.

As such therefore sometimes buying what appears to be the cheapest whole of life assurance for example, often could work out the most expensive, in more ways than one.

People in the UK look therefore for his money saving expert advice, searching online to get his Martin Lewis best life insurance for over 60s wisdom & tips.

Noting that as he is not a financial adviser, so he does not personally give advice, just cover the main issues and problem areas.

So firstly for any life insurance over 60 money saving expert hints, let's look at the 3 main ways you can buy life insurance.

1] Execution Only Sales

Money Saving Expert attempts to educate people about many types of financial matters. The normal best advice is to always shop around & if unsure always seek professional advice.

Apart from going direct either online or old fashioned paperwork to the various Insurers for their Over 60's life insurance offerings (which as mentioned - they don't recommend), they suggest the cheapest life insurance option is instead via an online 'execution only' discount broker.

Note: MSE point out that here, you must pay a fee first to that Provider to access their services. For example MSE recommend either using Cavendish online, Moneyworld, Moneyminder.

However, note cheapest here means you also won't get any advice or be speaking to anyone ie; No comeback if what was chosen by yourself, direct via their website, was appropriate to your ongoing situation. For example, you do not include waiver of premium on your protection policy to cover your plan being self employed.

2] Non-Advised Guidance

Then there are other life insurance sales agents they mention who may operate as FCA regulated brokers but via non-advised sales'. Now this part gets abit more confusing.

Although you are now speaking to someone about your life insurance enquiry this time, actually again you won't be getting any advice. You only just get information & guidance from their Sales Agent for you (not them) to make a more informed decision on the policies available you have then chosen to take out

In other words, No real comeback if your chosen Over 60 life insurance plan was later found inappropriate to your longer term care needs.

For example, you take out a life policy upto age 90, which you think is the same as over 60's life cover you have also read about, and the insurers will pay your premiums after that age. You died at age 91 in a care home, and your family are surprised there is no life insurance payout.

There are plenty of large Life Insurance Brokers online offering 'information guidance only' eg; Reassured, Lifesure & Protect Line, mainly operate via non-advised sales.

3] Advice

Finally, there are 'advised brokers or financial advisers', who as the name implies give advice. The Financial Adviser will fully assess your own personal situation, then document this to you in your demands & needs report. They will advise you after their research why they recommended the particular Insurers plans & benefits.

They can either cover & address every aspect of protection needs or alternatively just look at a few particular areas eg; you just wanted to discuss your own over 60 life insurance for now. Later down the line, your adviser could then re-look into any highlighted other protection shortfalls for your partner for example.

There are plenty of Life Insurance Brokers online offering advice. MSE Over 60 Life Insurance Martin Lewis would recommend several that also may offer incentives & vouchers like either Activequote, Howden, Lifesearch.

Over 60 Life Insurance Broker Case Study Example:

The Ups & Downs of the Brownes*

Mr Browne is age 69 next birthday. He's been married for over 35 years, still in reasonable health for his age and now fully retired. He is also nearly 10 years older than his wife, as they keeping reminding each other now.

Mrs Browne is aged 60, a fit and healthy full time housewife. The Browne's have 2 older non-dependant children, who now have proudly given them both 5 lovely grandchildren.

Their 4 bedroom detached home in Hampshire is currently worth around £450,000. They had repaid their initial main mortgage several years ago, but now still have a joint secured home owners loan of around £21,000 outstanding.

Their secured loan was taken out to finance home improvements, plus some extra funds for a 'project'. It was setup via his banks own finance company, and finishes when Mr Browne is in his early 70's.

This project they referred to was their new garage extension. It was built especially for Mr Browne, who had decided to buy an old classic Jaguar car.

The old Jag saloon was in need of some major restoration he admitted to his wife, so it was ideal for when he intended retiring around 65.

Something for him to dream about restoring to its former glory. A great project to tinker & fettle around with alongside his old mates, in their new man cave garage extension.

Once the Jag was fully restored (which may take a while he admitted), he thinks it maybe valued at over £20,000 after checking the prices in some classic car magazines.

The Browne's had also taken out an insurance cover with their loan. The company at the time said it was an obligatory requirement by the financial provider. It was their 'belt and braces policy'.

The finance adviser said it would help ensure the home loan would be protected for all eventualities, should anything happen to either party during the loan term. They then completed their various health & lifestyle questions to get insured.

The Browne's had an existing joint life insurance, which they took out when both kids were young. So far as Mr Browne was aware, this would still more than adequately cover this amount and plenty more extra.

However, he couldn't find any of the original life insurance paperwork. He thought the uk life insurers had probably changed their name, or been taken over, or something like that anyway.

Anyway, the main thing was the Browne's felt they have more than enough value in their home without needing equity release on the property, although house prices in the area seemed to be flat lining.

The finance adviser at the time who helped on this loan, had suggested also that they may now wish to consider legally splitting up their property into 'tenants in common'.

The adviser said put simply, it may potentially help to reduce the future financial impact of any prospective care home fees, under local authority means testing.

It all sounded like a good idea. He remembered reading about this exact topic in various Readers Digest finance articles, whilst waiting in their doctors surgery. So they agreed and this was all signed, sealed & done.

The reason behind why they had taken a secured bank loan out in the first place, was because they once originally had alot more in their savings & investments. This once totalled well over £160,000.

Most of this monies was an inheritance received from their respective parents properties, when they had sadly both died.

They had hoped the inheritance sum was actually going to be alot more. However, their parents had finally both been taken into care for their last few years mainly due to late onset dementia.

That difficult period was also made far more complicated to manage at that time, because neither sets of parents had arranged any powers of attorney or made wills.

Nevertheless, after paying their late parents various care home fees & costs, this had all mounted upto nearly £150,000 (or in other words - alot of money).

One evening, whilst finally sorting out their inheritance with their other family members, the Browne's were watching a late night film on TV together.

During the numerous TV advert breaks, several times he spotted one from a legal claims company going on about being mis-sold PPI, whatever that was.

Then suddenly a few days later he received a mailshot sales letter in the post asking 'if they had ever taken out PPI with a loan or other finance?' If so, they said it could have been mis-sold.

Coincidentally, it was sent from that same legal claims company he'd seen on the TV. He thought that sounded exactly like what they had signed upto with their banks finance company.

If so, the PPI claims company letter advised he could receive £1,000's they said if they were mis-sold the policy & with no upfront costs. He missed the bit that said if successful, they would then take off their own 40% professional adviser fees.

He filled in their forms anyway to say 'Yes, he was mis-sold' when taking out their home improvement loan. If he got it, that extra money would always be useful for his classic car rebuild.

He thought well why not, unsure if it was or wasn't mis-sold. But whatever, this claims company would investigate. Their existing cover had seemed quite expensive anyway, chatting to his friends about it.

Compared to what his old mates had said they were paying for their own life insurances, that also came with free terminal critical illness cover.

They told him their plans would pay out they thought, if they were ever diagnosed as having suffered a critical terminal illness, or some wording like that.

Within several months the banks finance company offered him a final settlement figure, mainly under the technicality that their insurance policy sold was advisory but not obligatory.

He was less pleased when he got a cheque back for only just over £1,300. This was the net amount they said, after deduction of their 40% professional fees.

However, after banking the cheque (the exact payouts amounts he never mentioned to his wife) was all then quickly spent on more expensive classic Jag parts off ebay.

A few weeks later, they then received a letter from the Providers to say they had now cancelled their loan insurance protection policy. He didn't realize that would also happen in this process.

Around that time Mr Browne had then seen his banks own IFA department about their parents inheritance monies, funds that were still sitting in a current account for the last few months.

The IFA was introduced to him via the Bank Manager. The manager initially explained that the IFA was an impartial broker, a sort of middleman to help him get the best financial deals available in the whole of market ie; not tied to one company.

The IFA Broker then discussed his overall family situation with him. He recommended that he consider carefully investing say £100,000 plus, across multiple blue chip companies they said, to fully spread the investment risk.

These as they pointed out, were all well known industry brands & respected financial names he had heard of. That made good business sense he agreed & would suit the risk profiles the adviser mentioned.

Then they suggested that due to that near 10 years age difference between himself and his wife, he really should consider looking at life insurance now & as he was well over 60.

The adviser said this was especially important once he retired, and lost any company benefits he may once have had. Then matter of factly pointed out that on average life expectancy, women do live longer than us men.

Mr Browne said he had some existing joint life insurance, but it now seems he had probably stopping paying the policy premiums around the time when they had repaid their initial mortgage.

So they suggested he could always take a small tax efficient income off the investment monies anyway, which could then help typically pay toward any life insurance premiums.

'Spread your Eggs' & 'Milk the Cow' were the strange farming expressions the IFA used ie; spread the risk & use some of the potential investment returns towards helping protect his wife & ultimately children's and grand kids inheritance.

He said it made good overall financial planning and they would review everything at least annually, if not 6 monthly. That did make sense he agreed, having sat there now for nearly 1 hour.

He soberly listened to all this initial advice plus their fees & costs involved, should he decide to proceed via their IFA.

However, at the back of his mind he then remembered reading about & watching all those adverts for Equitable Life, promoting proudly that they did not pay commissions to middle men.

As such, he decided maybe they were probably a much safer better to put all their money and savings into instead. Also but more importantly, to avoid paying commission fees to any middlemen, as their Equitable Life advertising said.

One of the blokes down the pub said they had used them before & said they were good, plus their upfront costs seemed much cheaper, as their adverts promoted.

So, he now made an appointment with them to discuss investments. A few days later, a very well spoken & smartly dressed chap from Equitable Life turned up at their home (in a new Mercedes coupe he noted).

After showing him impressive performance figures from their glossy sales & marketing folder of what his savings could do if it grew at say 5% or 10% over the next 5 or 10 years. He then agreed to invest £125,000 all with them.

The Equitable Life chap never really discussed anything to do with their overall financial situation, like pensions or life insurances. He was much more focused on seeking his investment monies.

Mrs Browne didn't really understand finance, so just bought them both cups of tea & biscuits, keeping out of the way whilst the 2 men chatted.

The chap said their Company would send them an annual investment statement in the post to track the performance, should he wish to review this yearly (but there was no obligation he said).

All the impressive looking Equitable Life brochures & new policy document paperwork turned up a few weeks later in their post.

For safety he then revisited his bank. He asked them to now keep a secure hold on these investment documents in the banks safe deposit.

He carefully tried to avoid the eyes of their IFA, as he completed all of their safe custody keeping paperwork with the banking clerk.

However, having invested all this money with them instead of via their IFA, unfortunately only just a few months later - the Equitable Life went bust.

The TV, radio and newspapers was full of this ongoing saga day after day. Mr Browne hoped this would be easily resolved by someone, or maybe the Government would intervene was the speculation.

That sales person chap in the Mercedes sports car that came round to their house, when he tried calling him to ask what was going on, it seems his phone number was now not working.

Laying in bed at night, he tossed and turned. He rued the fact that he had put nearly 100% of their family inheritance all with them.

He proudly didn't wish to discuss it further with Mrs Browne, who didn't know what to say either.

He was depressingly then advised after waiting months & months, they would be lucky if they got back a miserly £5,000 Equitable Life compensation as an investment victim!

Looking back, Mr Browne had worked hard for over 40 years as a senior electrical engineer, mainly working for several large companies. These employers had provided him benefits like employee sickpay, medical cover, death in service at 4 x salary etc;

He had also accumulated various workplace pensions over his lifetime, and they were a mixture of all different types of schemes. This he'd ensured that if he died in service, his wife would get all the money.

Mr Browne once laughingly remembered he had told his wife 'back in the day' over a couple of glasses of wine, that he would be worth more dead than alive.

He didn't really understand pensions, but if possible as he moved around employers he would consolidate and move these pensions across to their latest new company schemes.

When Mr Browne had finally retired aged 65, he had now been diagnosed with both raised blood pressure & cholesterol, but this was all under control with medication.

As he was now 65, various Providers mailing letters turned up regularly in their post offering him their no medical life insurance free gift deals.

As such, he decided to revisit his banks financial adviser (a different one than before luckily) for some general advice at retirement. He didn't mention anything to do with Equitable Life.

This person from his bank asked him about what he intended to do now to fill his days in retirement. He explained he had a classic Jag to restore, and the 2 blokes then chatted for a while on this subject.

He had also spoken to the banks adviser about his various pensions and the retirement options & choices.

After listening, he decided he would take all his works pension as a monthly level enhanced annuity of £1,200pm in his sole name (rather than a joint life annuity) with Mrs Browne, and non-inflation linked.

The reason being that should he have chosen to take the annuity in their joint names, or inflation index linked, he was made aware that he may get a much lower regular monthly income deal of around £750pm.

Currently therefore Mr Browne was now getting both his state pension and work pension incomes.

Together these pensions all totalled around £2,000pm net into his account, to help buffer their family coffers in retirement. More importantly, to keep the wolves from their family door he thought.

Mr Browne's pension income was paid into his sole bank account. From this amount, he then paid all their regular monthly household bills of around £1,250pm.

He usually gave his wife at least £100 per week cash in hand spends, as was family traditional. Mr & Mrs Browne had always maintained separate bank and savings accounts.

Many of their old friends seemed to have had similar finance arrangements with their partners.

Then the adviser switched subjects & turned to the benefits of having some life insurance in his 60's, making Powers of Attorney and Wills & Trusts also.

However although Mrs Browne was much younger, he decided all this wasn't necessary yet to think about. Yes, he had just retired... but they were much too young still.

One Friday afternoon, all the Lads had all gone down to the pub for a drink. They discussed the costs so far and progress (or lack of) on the classic Jag & to eat some fish and chips.

They also chatted & mentioned about all those various morning TV finance programme's now being retired & try to watch the pennies.

Like that bloke Money Saving Expert Martin Lewis on Life insurance did. Also various silver surfers useful guides & website tips on saving energy costs.

Plus those constant TV adverts, with old celebrities banging on & on about those over 50's life cover plans, or prepaid funeral plans and cremations.

All seemed to offer various free gift incentives. But as one of the lads Yorkshire parents had always told his friend's son...Young Lad, You Don't get Owt for Nowt.

They weren't critically ill, or on deaths' doors (all miserable subjects), so they all laughed about this over another pint.

Free Gift Deals...There must be a catch!

Mr Browne felt secure enough now that all was reasonably okay financially, after the Equitable Life mess up. He still had over £35,000 in savings plus a guaranteed regular pension income, and which his wife would all get if he died...Job done.

However, on his last birthday his own bank sent him yet again another timely mailshot - about how old he was getting. It was promoting their guaranteed over 60's life insurance no medicals cover. Plus a free M&S gift voucher offer if he took one out.

Mr Browne thought there was no harm done as he was still just in his 60's, and now having a few pre-existing medical health conditions of his own.

So he filled in their paperwork, ticked a few boxes and dropped it back to the bank when he was next in town. This Over 60's no medicals life policy was going to cost around £40pm for just over £7,000 life cover.

He didn't want to talk to anyone about it and if it was a good idea. Or check if it was a money saving expert life insurance best option for his age, as he was too busy. He had quickly glossed over reading all their life insurance small print & exclusions in the plans T&C's.

But he did like the idea of the free M&S gift voucher, which they said he would finally get after making several months payments (which he would use toward buying a present for his wife on her next birthday).

When the paperwork finally turned up in the post, he chucked it all into his office man drawers, alongside all the other mountains of household bills, post & stuff. One day he would get around to sorting it all out.

He didn't get around to mentioning it to Mrs Browne, as their financial conversations had dried up since they had lost all that money. Plus she was not feeling very cheerful that day, but he would do in due course.

They didn't really discuss money matters much anyway now, other than argue about the costs of his classic Jaguar parts that he seemed to constantly buy off ebay all the time.

Overall though, things were going okay financially for Mr & Mrs Browne in his retirement...regular holiday breaks, theatre visits and some occasional meals out with their friends.

Several months later the Browne's were actually eating out with some of their friends at a local Chinese restaurant. They usually split these bills being all retired. They asked him how he was getting on with his classic Jaguar restoration.

He admitted to them, that it was actually taking alot longer to complete & fully restore the car than he'd initially thought.

At the back of his mind though, he conceded that it had all become abit of a money pit. Once he had the time to really properly inspect the car having first bought it home, the old Jag was actually in much worse condition mechanically & cosmetically.

He got up to go to the toilet whilst thinking over this, when he suddenly clutched his chest as had a heart attack and collapsed. Mrs Browne rushed over panicking, and their friends called 999 immediately.

He was then picked up by ambulance and driven to the nearest hospital. Turning up there afterwards as a nervous wreck, she was then told by the doctors that Mr Browne may now be there for several months in intensive care.

They told her he had just suffered a major cardiac arrest, and was now currently drifting in and out of a coma. He will then also require heart surgery, maybe several stents but they weren't sure as yet.

Her 2 children, the grand kids, all their close friends & her surrounding family all rallied around to help & support Mrs Browne emotionally during this difficult time period.

Over coffee one morning, she admitted to some of their friends that neither had got around to sorting out power of attorney or making wills (like their parents hadn't either)...as it was still on their 'to do list'' being so young.

Their friends said similarly that they must really do this important legal exercise...but never seemed to find the time.

Also, she always thought that like her mum had once assuredly said to her over afternoon tea...Don't worry Luv "what was his (being married) was then all legally hers if either died - and vica versa".

Mrs Browne now wandering around her large empty house felt she may need to possibly adjust some of their home layout.

She thought this mainly so her husband didn't have to climb their steep staircase, whilst he was slowly recovering from his heart attack.

Yes, she was going to put in some stair lifts. All ready for when he hopefully returned back home soon from the hospital. But after checking, these were not cheap to buy or install.

So rather than maybe use some of her own savings, Mrs Browne plucked up the courage and decided to visit her husbands bank instead. Fortunately, all his pensions still came into his account.

She needed to tell them he was seriously ill in hospital but on his return home, she was going to install the stair lift to make it easier for him to get upstairs.

Once she got there, she patiently waited in their long customer services queue. When it was finally her turn, she began to explain her situation fully to the bank official in their small office cubicle.

Only to be abruptly told by the rude bank clerk that as it wasn't a joint account and as she didn't have lasting power of attorney - she wasn't entitled to access any of his bank account or details.

Neither would the bank give her any personal information (under GDPR data protection they said). The bank did make a note on their files.

Later on when she got home again, she told his old work colleague's what had happened and they sympathised with her plight.

They kindly suggested she may also advise his works pensions scheme meantime as a precaution, being that he was now critically ill.

Mrs Browne tried to regularly visited him in hospital over the ensuing weeks, even though sometimes he was back into a coma. She was soon racking up their expensive NHS hospital car park fees.

After nearly 8 weeks, he finally fully woke up from his ongoing coma. The hospital then moved him from their intensive care ward to another one, and so things were hopefully finally looking up at last.

He had now been in the NHS hospital for almost 3 months. He also had several heart stents fitted & the doctors seem reasonably pleased with the results so far.

As he was slowly improving now, she hoped for him to go back home shortly. The doctors advised her though that he may take a while to fully recover though.

He mustn't also too much physical activity, like say lifting heavy car parts on his old Jaguar car he was restoring they said.

After another hospital visit, his health seemed stable & whilst driving home again, she amusingly thought they probably needed his bed because he was annoying the nurses & other patients talking about his classic Jag.

Unfortunately, the hospital sadly called her early that very next morning. They said that due to various health complications overnight, Mr Browne had regrettably just passed away.

In total & utter shock and disbelief, she then called around her family and friends immediately to tell them in tears. She was very grateful for all their support at this difficult time again.

What to do now, where to start, it was all mind blowing...

She couldn't remember whether his final wishes were to be buried or cremated, as everything was a total and utter blur. She searched high and low for his will in his office man drawers.

She couldn't even remember or find if out if he had or hadn't even made a will.... If so, where was it?

Unsure as far as she was aware, he may have once mentioned the subject but he hadn't made any prepaid funeral arrangements either.

There was sadly therefore no guidance for her, as for Mr Browne's specific final requests plus arranging for his death certificate etc; etc;

She decided in a stressed out grieving mess after chatting with her 2 children, that he was to be buried with a suitable headstone near to his own parents and family.

The local funeral directors she visited said this would cost them all over £5,500 in total with a limousine, something befitting for him & to celebrate his life they said.

Then there was all those flowers, plus the wake, catering and drinks afterwards over at his favourite local club, which all came to another £1,500 ie; £7,000 overall.

Once things started to settle down a few weeks after the funeral (which she had paid upfront from her own ISA savings account), it all still seemed like a bad nightmare.

So after the shock of everything, Mrs Browne suddenly became aware that there were now some pressing financial matters. All issues that she had suitably avoided & discussing with her children whilst grieving.

Unsure exactly what to do when someone dies, his old work colleague's reminded her she should write to Mr Browne works pensions scheme asap, to tell them sadly he had died.

Interim, she also now had to work out how best to notify all those providers that they paid all their regular bills to. Those matters had all been sorted out by her late husband.

In a daze, she then visited the local government office department to advise of her late husband's death, along with his death certificate.

She wanted to know exactly what her state pension entitlements were. More importantly, to now see what amount of Widow’s Pension she could automatically get.

Mrs Browne waited in the long queue. When it was her turn, only to then be told by the government clerk - that this 'widows pension benefit' no longer even existed.

As she was well under state pension age herself, she was advised this had now been replaced by a Bereavement Support Payment, which she may now receive.

They formally said that as her husband had just died (which they offered their sincere condolences), his full state pension would now also stop.

However, she herself may be eligible instead to apply to the Government bereavement benefits scheme. She may then receive a lump sum, followed by regular payments for up to 18 months...

They advised her the most she can get from UK Govt bereavement support is:

- a one-off payment of £2,500

- 18 monthly payments of £100pm

This money (not any higher amounts, as she had no dependant children or wasn't pregnant) she was told could be used to help toward manage her regular monthly bills. This she knew totalled around £1,250pm.

The government clerk then formally advised this money would help cover other vital spending they said during this distressing time.

They ask if Mr Browne had any life insurance policies on himself to help her out, which she replied she didn't think so.

Mrs Browne then asked what happens after 18 months, would she get her own state pension? They said No...given her age, she realised she could have to wait over 5 years plus for that.

She asked how much state pension she may get, as she had been a housewife for all those years. When they told her, she realised it wouldn't even cover her normal household bills.

Having taken her only late husbands death certificate for own their records, she asked for it back. They then said they needed it for their administration, but suggested she now ideally would need to order up some more.

So in complete distress going home and after asking friends what to do when someone dies and some more death planning, she then ordered several more up...but at a cost.

Unfortunately, she then had to wait several weeks for these copy death certificates to turn up in the post, due to various ongoing local government strikes.

Mrs Browne then plucked up the courage again and re-visited her late husband's bank along with his copy death certificates, some of his recent bank statements and his credit cards.

She hoped to try and access the money they had, and more importantly his bank account, which her 2 children thought she should be able do.

Their local town Bank had now closed, so she had to drive 15 miles to the bigger bank branch in the next town. As she had not made an appointment, they made her wait 1/2 hour before being able to explain her predicament.

Only to be told by the Bank's official this time again, whilst looking at his death certificate, sadly it was still not her money. All his money legally they said was to be held (as part of his estate were their words).

His current & savings accounts plus his credit cards were now all frozen by the bank, once they had just found out he had died.

So now she couldn't access anything of his, and this timing issue was now also compounded as he hadn't made a will either. She then asked about all the regular household bills that was paid from his account.

Mrs Browne was then stunned to be advised by the bank adviser that not only his state pension but now his works pension income had also stopped being paid immediately upon his death.

The bank said maybe it was because his works pension had been taken in his sole name, and perhaps with no guarantees for her on his death. She was therefore not entitled to receive any pension inheritance.

They then pointed out looking at their computer records at the date of his death - it seems they had a joint secured loan but with the banks finance company.

The banks employee asked if there was by chance any loan insurance protection secured against the joint loan. Or something that they maybe held elsewhere.

She said No, well not now. It appeared that they once had some protection cover provided via the bank, but a claims company had advised if their PPI was mis-sold. From then onwards it had apparently been cancelled...

Given this was all going on in the papers & TV at the time, she said they had jumped onto the PPI bandwagon. So the Insurers had settled their claim, but then also ended their joint loan protection cover.

The bank employee looking up on their computer records, then said to her it wasn't called PPI they once had. It was actually they called their Gold Standard CCI & PHI Mortgage Loan cover policy.

The Browne's they said were sold a comprehensive combined critical cover insurance CCI protection with life insurance plus PHI permanent health insurance.

It was their 'belt and braces policy' and not their cheaper basic life insurance with TI cover. They said that meant the cheaper one pays out on earlier diagnosed terminal illness or death only.

This policy they once had seems it could have paid out upon either Mr Browne's coma, heart attack or upon his death. It then would have fully repaid their whole outstanding loan.

Mrs Browne listened to these various jargon phrases like PPI, CCI, PHI or TI insurance cover but didn't know what to say, as they all sounded so similar.

They sympathize with her but explain that the regular home loan payments must still be made, otherwise they could legally repossess her property as Martin Lewis on secured loans comments.

It also seems there was some paperwork from Mr Browne still held on their safe custody banking records. She asked was this her late husband's final will & testament by any chance.

But after the clerk sent somebody off to recheck, they said it was actually relating to an old joint life insurance. There was definitely no wills lodged for a Mr Browne on their bank records though.

Importance of Making a Will

After getting her hopes up again & double checking also however, it looked like he had stopped paying the life insurance premiums on their old policy a long while ago, for whatever reasons.

The kindly bank official then pointed out re-looking at his existing direct debits, that it did seem that he had still been fortunately making regular payment to the Bank's Life Insurance company. It was for their Over 60's lifecover plan.

This was getting all too stressful for Mrs Browne, not knowing what this insurance was or wasn't and if still valid.

He luckily then offered to call up their customer services department for her. She sat nervously waiting, fingers crossed whilst they investigated further.

After holding onto the phone line for 10 minutes listening to music, the clerk waited to get through & speak to somebody in the Insurers customer death claims section.

Once through, the Insurers advised them that a full claim for the £7,000 life insurance wasn't unfortunately possible due to their T&C's.

The reason they explained was because Mr Browne had just died due to natural causes during their initial no medicals 2 years inception period.

He hadn't died due to an accident, which they said if he had 'during that 2 years period only' would have made a potential larger life insurance claim possible of £21,000 ie; 3 x £7,000 life cover amount.

The clerk realised that roughly amount could have also potentially repaid their bank's finance company homeowner loan.

The insurers said however as such she would only be entitled to refund of all his monthly life insurance premiums already paid to date, plus interest of course.

This all amounted to just over £325....but would all be paid back into his estate again they advised. They said he had ticked their box to not place the plan benefits into trust.

Neither had he fully filled in the part of their form to nominate any beneficiaries either. Although he had ticked the relevant box to do so, but for some reason then left the rest blank.

As a kicker, they then whispered to the bank official that unfortunately he had sadly not paid the policy premiums long enough to even get any free gift vouchers.

The bank clerk explained most of this to her, sympathetically missing out some of the parts like where Mr Browne hadn't filled in the forms correctly & no gift vouchers.

In shock and now embarrassed, she asked if the bank would kindly offer her say a short term bank loan.

However, they said as she already held a joint loan with their own finance company and didn't bank with them directly, they apologized but declined to offer her any new deal. They suggested she visit her own bank or building society.

When she finally left their offices, their official then contacted the banks finance company about their joint secured home improvement loan.

They were aware Mr Browne had some savings & investments. But these could all be locked up for a while though re probate. Supposedly it now seems he hadn't made a valid last will & testament.

The staff chatted to each other & suggested they now write to her and offer condolences on Mr Browne's death, and also enclose a new direct debit mandate.

They suggested perhaps then re-diarising several months later again, if they had not received their regular monthly loan payments, for whatever reason.

Then, if in arrears (worse case scenario) look to maybe consider starting repossession proceedings. As their officials said to each other at the time... 'the bank was not a charity,' which they added was harsh but true.

Mrs Browne returned home in a daze yet again, collapsed on the sofa and opened up a bottle of wine. She tried to think whom she needed to also speak to next.

All the normal regular bills like gas, electric and utilities were also still held in her late husbands name, so she would now have to contact them all & to advise of her husbands death.

She sat down with her 2 children after all this stress & shock and now realised that she was soon going to be in financial difficulties. They suggested she seek some free advice with the local Citizens Advice Bureau.

As Mr Browne hadn't made a valid will it seems she could find (so died intestate) she desperately needed someone knowledgeable to help discuss her overall situation. Mrs Browne then visits them along with her children to ask their advice.

Once she sat down with the Citizens Advice person, they ask if her late husband had made a will. She said 'No'. Or they ask, had he taken out any life insurance.

Before hearing her reply, they also then ask if she was aware if any life insurance policy he had was written into a trust - because that would be very helpful to her still then.

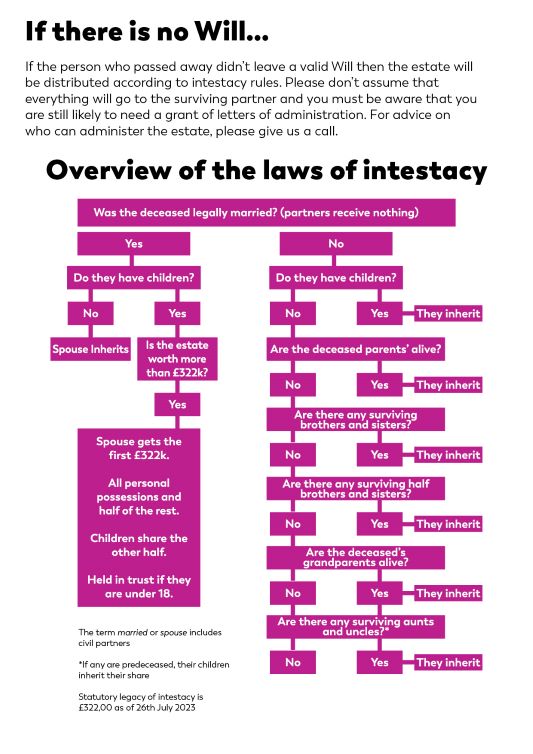

They then proceed to tell her anyway currently these are the legal UK Intestacy rules ie; if there is no Will...

She may be entitled to inherit as follows...

- If there is a surviving partner they inherit the first £322,000 plus personal possessions

- They can also have half of the rest if above £322,000

- Children may then inherit the remaining half from the estate if this is valued at over £322,000

- When there are two or more children, they will inherit in equal shares above £322,000

After listening to her, Mrs Browne's 2 children and usefully for them their 5 young children (her grand kids) now realize they could potentially request they legally inherit something from their Dad, (even if this put their own mother in financial difficulties).

Mrs Browne decided in desperation as she listened, that she was going to have to sell their joint property and either buy somewhere cheaper or rent.

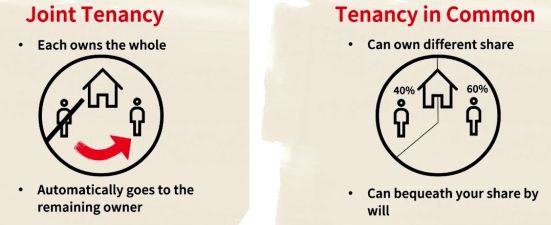

They then asked her if their property was held beneficial joint tenancies or tenants in common.

When she advised them what they had done a few years ago, they then said that if the 2 partners are tenants in common, the surviving partner does not automatically inherit the other person's share.

They pointed out if the partners were beneficial joint tenants at the time of the death, when the first partner dies, the surviving partner will automatically inherit the other partner's share of their property.

However, as Mr Browne hadn't made a will and the property was held tenants in common, she was now caught in a Legal Catch 22 mess.

She realized she couldn't afford to appoint their usual solicitors and their expensive fees, so looked instead to affordable any legal advice Citizens Advice suggests instead via a charity.

That morning a letter had also turned up from the HMRC taxman addressed to Mr Browne, which she opens to find he has an outstanding tax bill to pay.

In desperation she also spoke to friends to even check if inheritance tax is due for example on their main property but believes she is exempt from IHT she thinks & hopes.

So Mrs Browne must now apply for letters of administration herself to the probate registry as an 'administrator' of her late husband's estate instead. The nightmare continues.

She couldn't do anything now currently anyway. Citizens Advice has told her Probate & Letters of Administration without a will typically may take 9-12 months to fully settle an estate.

However, it can sometimes take longer they said. For example, if there is an issue with any property or other assets to sell, complex Income & Capital Gains Tax, Inheritance affairs to resolve.

Or there are complications regarding the personal representatives or beneficiaries of the estate ie; explaining to her 2 children not to currently claim any rightful inheritance because of intestacy rules.

That afternoon she calls up a local classic car garage and mentions about her late husbands classic Jaguar locked up in their garage extension.

They make an appointment to come around eagerly to view it, but suggest she would have to await due legal process before considering selling any classic car.

Once viewed, they then said in its current state of restoration, it was probably only worth around £7,000 (not £25,000). Or perhaps be sold for spares or repairs to a classic Jaguar enthusiast they said.

Or more poignantly she thought similar to Mr Browne's final funeral costs. Meanwhile, all those bills would continue to quickly mount up...

Over 60's Life Insurance Case Study Conclusion:

What you think may happen Legally & Financially if someone dies whether in their 60's or not - Could be entirely different in reality...

- Over 60's Life Insurance Martin Lewis would agree may help alleviate financial distress

- MSE says writing a life insurance into a suitable trust may help avoid probate delays

- Although married, not making a will can create real financial issues upon death

- State benefits are limited for widows and widowers

- The surviving partner could still live on for another say 20+ years

- Have to then cope emotionally and financially on their own

- Sole bank account & savings on death can cause immediate access problems

- Your surviving partner may not get some or any pension benefits on death

- Powers of Attorney are useful as you get older to protect yourself legally

Martin Lewis advice on Over 60 life insurance & ours is apart from sadly losing a loved one & breadwinner, this real hidden income threat is what could be lost if the main earner died prematurely and their affairs are not in order.

NOTE: *Many of these sad finance story tales in this fictional The Ups & Downs of the Brownes case study - have all actually happened to several clients we have dealt with over the years...

Over 60 Life Insurance Martin Lewis?

If you are looking into taking out Over 60 Life Insurance Martin Lewis specifically doesn't really explore the reasons behind you for looking at getting life cover, mainly just the best deals available.

For example, you maybe just want a small lump sum to just pay towards your funeral or small legacy? So this lifecover must payout 'whenever you die.'

Insurers will therefore charge accordingly for this 'unknown time frame' offering for their whole of life assurance policies.

However for others over 60, they may already have a funeral plan or suitable investments set aside? Instead, they now just want to help provide their partner & family with a larger backup plan fund and which ideally runs well into their retirement.

Some UK Insurers could maybe still provide you an alternative over 60's life insurance value proposition. Those who would just like their life insurance cover to last well into their retirement, to help protect their ongoing lifestyle and joint bills.

For anyone after over 60 life insurance Martin Lewis does not comment here, so as brokers we are often requested for a range of cost effective alternatives...

Term Life Insurance Over 60 Money Saving Expert?

In their main guide to Life Insurance Money Saving Expert focuses on either term life insurance mainly for younger families with dependant children & over 60's no medical life cover plans for say funerals.

But what happens if you don't have younger dependants, who may decide to leave home in say 10 years time? You want cover to something that will run well into retirement & that is affordable when being on pensions

A Term life insurance upto age 90 - sometimes could be as much as 1/2 the cost of a whole life insurance Over 60's comparison.

The reason being that 'it may not payout' - as you could outlive the known plan time frame. eg; You live to age 95.

Many UK Life Insurers offer life insurance terms upto to age 90, others may stop at age 85 or sooner dependant on their deals.

Note: That average life expectancy in the UK is currently around age 80. Women however statistically live longer than men. However, life insurance rates are the same for both due to EU gender neutral rates applied since 2012.

As long as you feel that a term life policy ''backup plan" realistically is not needed after these ages, then this could be a different over 60's life insurance alternative to whole of life assurance?

Contact us for a Comparison Term Life Quote >>

Over 60 - So Should I Cancel my Over 50's Plan?

Now you are into your 60's (as you may read this) you could already have had running for several years or more a no medical over 50's life cover policy?

For Martin Lewis on life insurance over 50 plans being cancelled, he points out that the answer isn't that simple, especially if you have read his pro's and con's.

As he points out you are locked in, so if you stop paying now, or miss a payment all your past contributions will likely be lost. Some life insurance companies have adjusted their philosophy here during the Covid Pandemic.

Note; Most of these Over 50 life insurance no medical schemes have no cash in values if you stop premium payments - unlike some old fashioned endowment policies.

Many Insurers Over 50's plan premiums may only usually stop being taken after say age 90 (see their policy T&C's).

Indeed, any regular payment contracts MSE may have recommended via their Over 50's switching tips to save you money. (but that is often the same principle whenever you replace most insurances).

He also says this often is dependant on your health. If you've got poorer health now, you can play the odds, and so your existing over-50s' no medical questions plans can still provide valuable cover in your 60's.

Alternatively, as brokers we do come across clients in their 60's, whose existing life policies may end say in a few years time.

They are unsure whether to keep them going to the end...and then start a new policy. Or concerned should their health change interim (so struggle to then get affordable life cover), start up a new over 60 life insurance policy now.

We would add that as you are also probably some years older now since you took out the cover, the price of any new underwritten life insurance does increase alot more into your sixties.

Unsure - Contact us for a Comparison Over 60 Life Insurance Quote >>

Martin Lewis Life Insurance for Over 60s & Complaints

Should you wish to complain about your over 60 life insurance company MSE have given you a free complaints tool link to a website called Resolver.

Their tool they say helps you to manage your complaint, should you have one and need to monitor it.

Money Saving Expert do say if the insurance company doesn't play ball, it can also help if you wish to escalate your complaint then contact for the free Financial Ombudsman Service.

'Over 60 Life Insurance Martin Lewis' Conclusion

As mentioned already therefore, re those looking for Martin Lewis life insurance for over 60s plans advice, he is not a big fan of the packaged no medical style of life insurance.

Check the above Pro’s and Cons chart for our own Martin Lewis Over 60 life insurance comparison analysis. Over 60’s no medical lifecover plans are as MSE mentions maybe only ideal for people who do have serious health issues thus a shortened life expectancy.

Alternatively, some who don’t want to answer any lifestyle questions or maybe just like the idea of a free gift?

Martin Lewis best life insurance for over 60s again should note that most no medical lifecover plans may usually have upto initial 1/2 years waiting period before any full death claim.

This means if you did die of natural causes during this ''initial period', the Insurers will not payout fully (other than usually return premiums plus interest) unless if died due to an accident.

Any full medical questions underwritten lifecover will alternatively potentially offer you cover immediately, without this 1/2 years waiting periods.

These other life insurance plans usually also will offer much higher lifecover amounts but for a similar monthly cost. They are also often used for those concerned about Funeral Costs, Family Protection & Inheritance Tax Planning.

Ultimately though, you pay’s your money and takes your choice of perhaps one or all product over 60 or over 65 insurance life cover combinations. How much can you afford to set aside each week to help protect yourself, family and loved ones ?

If you can afford it, my own thoughts aside from what does Martin Lewis say about life insurance for those insurers offering plans for those over sixty, are ideally following these same principles as mentioned above.

- Lump Sum > Repay any mortgage loan & debts, funeral costs

- Income > Help cover your ongoing monthly bills & expenses

- Lump Sum > Back up for holidays, education, emergencies

Take care of Yourself, Family and Loved Ones. ![]()

Article on 'Over 60s Life Insurance Martin Lewis' Guide by Martyn Spencer Financial Adviser August 2026

For reassurance re health for men & women – we review many of the best Life Insurers selling Over 60 Life Insurance in UK (inc NI)

*Any comments & views expressed on this Over 60 Life Insurance Martin Lewis Money Saving Expert review are for generic information only. They are not personalized advice or necessarily reflect MSE views.