Myself

Myself My

My My Income

My Income

Article on: ‘Bright Grey’ Insurance

‘Bright Grey Life Insurance’ Review

Bright Grey Insurance – Background History

Royal London Insurance Group originated back in 1861, when their founders met up in a London coffee shop. It is now become one of Britain’s largest friendly society mutual life insurers.

In 2003, Royal London decided to soft launch a specialist new protection provider business. It would be under a unique brand name & they would call it ‘Bright Grey’.

To stand out from the crowd, their logo was a shade of Bright Pink, not Bright Grey. They said it would be different from the usual life insurance marketplace – Being Bright Grey was being different.

At the time, Royal London said it would bring Bright thoughts during people’s Grey Times? At the start of the millennium & with ongoing world issues, maybe they were right?

Royal London analysed the protection market & decided a more simple approach was needed. They would offer menu style products allowing brokers & their clients to pick and choose their bright insurance reviews offering.

Bright Grey would concentrate on both the personal & business marketplace helping brokers, IFA’s and various affinity partners.

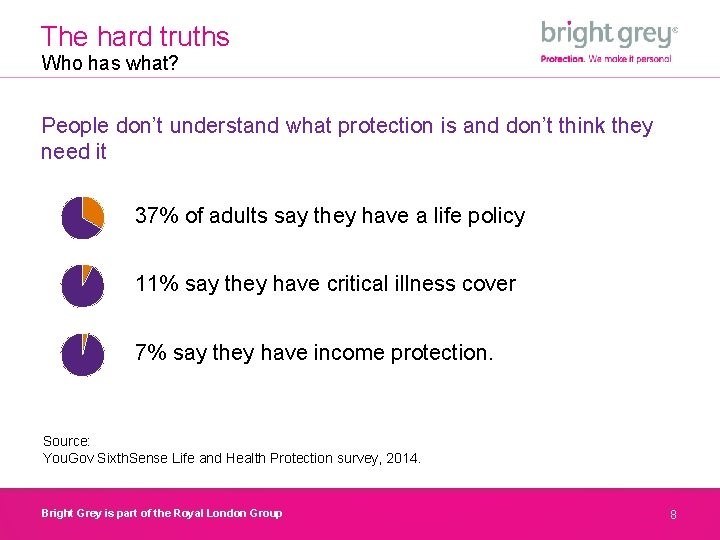

Bright Grey Life Insurance reviews showed they then became a popular proposition in the life insurance market among Uk Life Insurers.

Compare Bright Grey Life Insurance & BrightGrey Critical Illness Cover.

Bright Grey Insurance gave you a Helping Hand

Royal London Bright Grey brand was launched around the ethos that Insurers should be there not to just to help people financially at time of need, but also to support them emotionally. This was a relatively new idea at the time for financial services.

Bright Grey Royal London was going to now offer it’s customers a Helping Hand via a new support service ie; professional counselling, all designed to help people recover. Helping Hand are 3’rd party provider specialist & they made this service available to their policy holder’s immediate family as well.

When you made a claim, Bright Grey assigned your own RedArc nurse adviser, who were an independent advisory service. They also included 2’nd medical opinion plus specialist & complementary therapies. Helping Hand also included general help & advice including, work, money, business & legal.

Royal London still use Helping Hand support services today.

‘Bright Grey’ & Scottish Provident

In 2008, Royal London then acquired the 170+ years old established heritage brand Scottish Provident. They had also acquired United Friendly UAG back in 2000 & several years later Royal Liver, so were used to dealing with older Insurers.

So Royal London now had 2 protection brands, aimed supposedly at 2 different clients but believing each could work & play well alongside each other. Royal London would also now try to adopt their simplistic, stripped back Bright Grey approach, onto the older Scottish Provident brand products.

The life insurance Bright Grey brand was just 5 years old. Would it be looked down on by its new 50 shades of grey, older great relative? Could the old mix & play well with the new, or would it just confuse people ?

Over the coming years, Bright Grey tried hard to please its audience with their individual message & unique style. However, things had to give between the 2 brands as the market conditions changed.

……….

……….

What did Bright Grey Life Insurance become?

Unfortunately, by 2015 Royal London decided that the answer was ‘No’ to keeping on the Bright Grey Insurance brand. It meant that they would drop both Bright Grey & Scottish Provident brands & then simplify the message to just one brand name, Royal London.

At that time they said ‘it is the quality of our service and our products that are a measure of our strength, not what colour our logo is’. So this Bright Grey story sadly fizzled out – not Bright but abit Grey.

Bright Grey Life Insurance Review | Broker FAQ

*Is Bright Grey still part of Royal London Insurance?

Yes, they deal with old life insurance Bright Grey Royal London policy administration. Please contact Royal London customer services for any ongoing policy queries eg; Bright Grey lifestyle protection plan included some of these old menu policies for personal & business cover.

- Bright Grey Income Protection Insurance

- Bright Grey Critical Illness Cover

- Bright Grey Relevant Life Business Cover

*Can you make changes to your existing Life Insurance?

In terms of changing your existing ‘Bright Grey Insurance’ policy, often you can request some of the following via Royal London:

- reduce or perhaps extend the period of cover

- decrease or increase the amount of lifecover

- remove indexation option or any specific paid for policy features

- change the collection date of your usual premiums

- take off a life assured from a joint policy eg; if a unmarried couple or new parents sadly split up

These bright gray insurance changes could be subject to new Royal London medical underwriting based on your circumstances at the time & may well affect your premiums.

*How do I cancel my Life Policy?

You may cancel your existing ‘Bright Grey Insurance’ plan at any time, if your circumstances change but your life insurance cover would then end.

However, if you should cancel the insurance policy, you may not get anything back, if your policy has no cash in values. This also means if your health changed adversely afterwards & you then tried to request a new (now Royal London life insurance) policy is put back onto cover again, this maybe declined.

We suggest you seek professional advice before taking this course of action.

*Should I put my Life Insurance ‘Bright Grey’ policy into Trust?

When a life insurance policy isn’t written into trust, it will be paid to the executors of the deceased’s estate. They will handle the administration, known as probate in N Ireland, England, Wales and confirmation in Scotland. If not, the death insurance benefits will fall into your estate if you died prematurely. If you have not made a will, this can then cause further complications with the life insurance monies.

Until probate is fully granted, no monies can be paid out to those named in the will. On average, this can take upto 6 months. By not placing the plan into trust may also swell up the total estate values, leading to potentially Inheritance Tax IHT issues.

So placing a Royal London Bright Grey life insurance policy in trust can help to ensure that the policy proceeds go to the correct beneficiaries you decide to nominate at that stage. It can also help avoid possible probate delays & IHT costs. Ask the Insurers to kindly provide their available standard trust form wordings & seek legal advice if unsure.

*Importance of Disclosure & Claims

All Insurers are in business to protect, insure & payout. Insurance cover is therefore based on your full disclosure at the time you took the original insurance policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying. The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless when applying. eg; Not disclose if you familial history of raised blood pressure or raised cholesterol (even if it costs more). If so, it may not payout !

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details. They will then assess if your insurance claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers – not 100%).

*What if my health or lifestyle changes after I had taken the Life policy out?

Any health or lifestyle changes since, usually does not void your existing ‘Bright Grey Insurance’ policy, if it wasn’t relevant at that time of initial underwritten insurance application. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your life insurance bright grey application what you initially disclosed to the Insurers, as this information then stands now and in the future. Please check your original T&C’s.

Today, Royal London have grown to be one of the major Life Insurers UK selling Life Insurance in United Kingdom (inc NI)

Article on ‘Bright Grey Insurance’ by Martyn Spencer Financial Adviser (2026)

|  |