Myself

Myself My

My My Income

My Income

Norwich Union Life Insurance (Now Aviva). Review old Norwich Union cover against Aviva broker deals from £5pm.

'Norwich Union Life Insurance' Review

'Norwich Union' Background

Norwich Union was founded back in 1797, when a Norfolk merchant called Thomas Bignold started 'The Norwich Union Society for the Insurance of Houses, Stock and Merchandise from Fire'.

From 1893, it became 'Norwich Union Life Insurance Society' and it grew during the next century into one of the biggest UK Insurers.

In 1997, Norwich Union demutualised and then floated as a PLC on the London Stock Exchange. Back then, it was the first mutually owned British insurer to do so and also lose its mutual status but making it one of Britain's 50 largest companies.

In 2000, Norwich Union merged with CGU; which itself was formed from the merger of General Accident and Commercial Union in 1998. These providers all once had their own large sales forces.

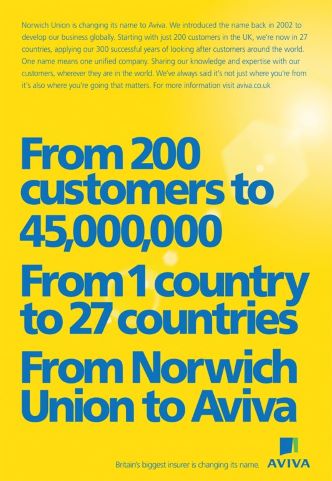

Upon merging, they formed the new CGNU Life Insurance Group, which from 2002 now became part of the new Aviva Group in the UK. The logo was changed but at the time the Norwich Union Insurance brand was initially kept in the UK, as now Aviva Norwich Union.

Their products were sold by both IFA's, brokers and ties to various banks and building societies. 'Norwich Union Aviva' were once a popular proposition in the Uk life insurance & pensions market among leading Uk Life Insurers.

Norwich Union Life Insurance

'Norwich Union to Aviva'

When did Norwich Union become Aviva? Back in 2008, Aviva then announced they were intent on phasing out the 200-year-old UK iconic brand name Norwich Union and would mainly just trade around the globe as just Aviva Insurance.

At the time, there was public amazement that Aviva could drop such a familiar & trusted UK household brand. So the Norwich Union name would suddenly disappear after a public flotation only 10 years or so before.

Aviva decided that if Bruce Willis, Dame Edna Everage, Elle Macpherson, Alice Cooper & Ringo Star could change their names to get ahead, so could they change from Norwich Union to Aviva.

Willis was Walter Bruce Willis, Macpherson was originally Eleanor Gow. Richard Starkey was Starr, Vincent Damon Furnier was Cooper & John Barry Humphries became the pantomime character Dame Edna Everage.

Old Norwich Union Advert

The above Norwich Union Aviva | TV Advert was possibly one of the most expensive due to their number of high profile celebrities?

In a series of TV adverts, these celebrities suggested that they would be just as successful in shelving the 200-year-old brand Norwich Union and relaunching as Aviva. Since then, Aviva merged with Friends Life in 2015.

Both Aviva and Friends Life at the time had a large presence in the UK life insurance protection market. They hoped their new combined strength would help them come to dominate in this sector by economies of scale.

The Aviva story still continues today with Norwich Union, as some of Norwich Union original offices form part of ongoing Aviva administration issues. They still remain a major employer in Norwich area.

Norwich Union Pensions query ? Contact Aviva

Norwich Union Life Insurance | Broker FAQ

Is 'Norwich Union' now part of Aviva?

Is Norwich Union now Aviva? Yes, Aviva still look after Norwich Union Insurance old policy administration as part of their heritage legacy section.

For best Norwich Union contact number, please contact Aviva customer services for any ongoing policy queries eg. Norwich Union Pension Life Insurance or old Norwich Union life insurance policy.

Can you make changes to your old 'Norwich Union' life insurance policy?

In terms of changing your existing Life Insurance policy, often you can request some of the following via Aviva:

- reduce or perhaps extend the period of insurance cover

- decrease or increase the amount of lifecover

- remove indexation option or any specific paid for policy features

- change the collection date of your usual premiums

- take off a life assured from a joint policy eg; if a unmarried couple or new parents sadly split up

These changes could be subject to new Aviva medical underwriting based on your circumstances at the time & may well affect your premiums.

Note: customer services phone number for Norwich Union reviews is via Aviva.

How do I cancel my Life Insurance Policy?

You may cancel your existing 'Norwich Union' plan at any time, if your circumstances change but your life insurance cover would usually then end.

However, if you should cancel the insurance policy, you may not get anything back, if your policy has no cash in values. This also means if your health changed adversely afterwards & you then tried to request a new (now Aviva life insurance) policy is put back onto cover again, this maybe declined.

We suggest you seek professional advice before taking this course of action for Norwich Union contact details & calling any Norwich Union phone number (now Aviva).

Should I put my 'Norwich Union Life Insurance' policy into Trust?

When a life insurance policy isn’t written into trust, it will be paid to the executors of the deceased’s estate.

They will handle the administration, known as probate in N Ireland, England, Wales and confirmation in Scotland. If not, the death insurance benefits will fall into your estate if you died prematurely. If you have not made a will, this can then cause further complications with the life insurance monies.

Until probate is fully granted, no monies can be paid out to those named in the will. On average, this can take upto 6 months. By not placing the plan into trust may also swell up the total estate values, leading to potentially Inheritance Tax IHT issues.

So placing a policy in trust can help to ensure that the policy proceeds go to the correct beneficiaries you decide to nominate at that stage. It can also help avoid possible probate delays & IHT costs.

Ask the Insurers & call Aviva Norwich Union life insurance telephone number to kindly provide their available usual standard protection trust form wordings. Seek legal advice if unsure.

Importance of Disclosure & Claims?

All Insurers are in business to protect, insure & payout. Insurance cover is therefore based on your full disclosure at the time you took the original 'Norwich Union' insurance policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying.

The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless when applying eg; Not disclose if you any familial history of high blood pressure or cholesterol.

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details. They will then assess if your insurance claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers – not 100%).

What if my health or lifestyle changes after I had taken the Life policy out?

Any health or lifestyle changes since, usually does not void your existing 'Norwich Union' life insurance policy, if it wasn’t relevant at that time of initial underwritten insurance application. For example, later on diagnosed diabetic type 2. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your application what you initially disclosed to the Insurers (now Aviva), as this information then stands now and in the future. Please check your original T&C’s.

Article on 'Norwich Union' Life Insurance by Martyn Spencer Financial Adviser (2026)

|