Myself

Myself My

My My Income

My Income

Article on: Over 40 Life Insurance mse

“Over 40 Life Insurance”

How to choose the best ‘Over 40 Life Insurance’ in 2026?

Life Insurance is designed to financially help those left behind – cope with their day to day money worries & the stresses that may often happen when losing a loved one & breadwinner.

For many families with dependents, a suitable ‘Life Insurance Over 40’ = Peace of Mind.

We all may think we are invincible….. But

Once you reach the ‘Big 40’ many Insurers will adopt a slightly different stance to their underwriting. Their age bands may allow a certain level of insurance cover upto age 40 without further medical health evidence. BUT they may do so now you are over age 40.

So, how do you choose in 2026 what’s the best life insurance for over 40 Uk policy cover?

There are many different types of ‘over 40s life insurance‘ policies set up to suit all different sorts of needs. A Lump sum or Income ? Level or Increasing ? Single or Joint Life?

From whole lifecover, term life insurance & critical illness, mortgage protection, family income benefit types of cover. Unsure of the right ‘life insurance for over 40’ policy or how much cover? We can help you arrange your ideal cover.

What’s Martin Lewis Over 40 Life Insurance Policy?

MSE says ‘Thinking about how your family may cope financially if you were to die isn’t a very cheerful topic, BUT it is an Important One’.

The MoneySavingExpert Martin Lewis comments that he does ‘100% recommend Life Insurance’ (whether over 40 or not) especially if you have any dependants.

So Martin Lewis agrees life insurance is important IF anyone is reliant on your Income & would struggle financially without you around ie; an insurable interest.

Martin Lewis life insurance policy says YES it’s a cheap financial lifeline but the ultimate monthly costs choice is always yours.

He also discusses the value in other insurance plans if you were off sick, like income protection & critical illness.

What does MSE Martin Lewis say on Over 40’s Life Insurance?

Martin Lewis for a good rule of thumb in 2023, his Best Life Insurance formula is ‘THE 10 x RULE’ ie; aim to cover 10 x the Annual income of the highest earner & the main breadwinner until at least any kids have finished their full-time education or other dependants.

To help you calculate a figure that works for you, Martin Lewis Life Insurance policy says it’s worth ensuring any life insurance policies cover:

- Outstanding Debts: that need to be paid off eg; mortgage unless covered by a separate plan

- Immediate Outgoings: regular bills dependants would need to pay

- Future Spending: you may have wished to make eg; university fees

- Additional Expenses: a death may trigger eg; funeral costs

Martin Lewis also suggests being the Money Expert – that you “NEVER BLINDLY BUY DIRECT” expensive policy offers either via your Bank or One Insurer ie; Shop around or use a Broker.

Lastly, MoneySavingExpert also said generally remember, not all insurers plans are featured on insurance comparison sites. As brokers, we would also agree here – so let us help you shop around for your best broker deals.

In terms of the large range of Life Insurance policies available, Money Saving Expert are fully impartial with all their best buy reviews. As you maybe aware, neither Martin nor MSE never endorse products.

Note: Yes, they mention individual products & services on MSE site, but they make it very clear don’t ‘support’ them.

How much Life Insurance do I need if over 40?

How much Life Insurance do I need in my 40’s? As Life Insurance Brokers, this simple ‘3 reasons formula‘ cover you may wish to consider in an ideal world if looking to get over 40 life insurance.

- LUMP SUM – Repay a Mortgage / Loan / Debts – Often your largest outgoings

- INCOME – Provide for your Family – To help cover ongoing monthly bills / lifestyle / holidays

- LUMP SUM – Help cover Funeral costs & Back up plan – Those final expense costs

However, the Martin Lewis Life Insurance formula in 2026 instead simply suggests just covering 10 x salary of main breadwinner – after payment of mortgage & debts. Is that enough?

Using that principle, if you earned £40,000pa gross, Martin Lewis says you should maybe consider insuring yourself (after any debts, mortgages & loans are fully repaid) for say £400,000 cover life insurance (ie; 10 x the annual gross income).

Following on from this simple Martin Lewis MSE example formula above, if you then worked for the next 25 years until retirement age 65, you could potentially earn over £1 million gross ie; £40,000pa x 25 years [or more with any future inflationary wage rises].

As such, unlike the 10 x £40,000 gross salary life insurance over 40s example above – you could instead protect your family with either;

- Income = £3,333pm or £40,000pa family income benefit lifecover policy

- Lump sum = £1 million level term life insurance policy [if invested @ 4% return = £40,000pa]

- Or a mixture of the 2 policy types over the next 30 years – all dependant on your family circumstances.

However, as Financial Advisers we are not saying this ‘Money Saving Expert formula’ 10 x salary is therefore a 100% one size fits all scenario ie; This best life insurance for over 40 uk formula is not applicable for everyone’s own personal situation.

- You can decide wether you want the life insurance for 40 and over to be level or inflation linked

- Single plan | 2 x seperate plans | or Joint life over 40 insurance

Types of Life Insurance on Over 40 (2026)

* Term ‘Life Insurance Over 40’ | Level Family

- Term Life Insurance for over 40 are simple plans to operate.

- If you die within that set ‘term’, your family will get the set life insurance lump sums payment.

- Cover is ‘underwritten’ meaning Insurers will ask you medical & lifestyle questions before offering terms

- A Life Assurance term policy will offer cover for a fixed period of time or ‘term’. eg; 20/25/30 years

- You could set up plan upto retirement, any child is independant or even upto age 90

- Because it runs for a set term, it may have more affordable premiums [BUT you may live out that nominated term]

* Critical Illness Insurance

- Designed to pay out on diagnosis & survival of a specified Critical Serious illness where benefits are currently paid out tax free upon claim

- Insurers plan terms vary & may cover between 25-100 different types of serious illness benefits

- Critical Illness coverage usually all include these main 3 claims:- Cancer, Heart Attack & Stroke

- Designed to pay out usually as a lump sum upon diagnosis of dread disease

- Medical evidence may be required & a medical examination for based amounts of cover or those with health issues

- Premiums on critical illness cover may be fixed guaranteed or reviewable

- Money savings expert Martin Lewis on critical illness suggests 10 Year Rule ie; consider cover of 10 years salary

* Decreasing Life | Mortgage Loan Insurance

- Decreasing term life insurance will reduce over the mortgage loan term but the premiums remain level

- It is designed to usually help repay your mortgage, loan or other debt – where that amount owing will reduce over the term

- You can set the % at which the plan reduces at outset eg; If your bank loan is fixed at say 5% for 15 years, then so could the policy

- Level term life insurance at 40 may suit if you have an interest-only mortgage or loan ie; the amount owing stays the same.

- Ideal repayment mortgage coverage for life insurance as it decreases

* Term Life | Family Income Benefit

- A Family Income Benefits [FIB] term policy pays upon death a set monthly income

- The monthly income on a death claim is then just paid for the remaining fixed term of the plan

- Example: £1,750pm FIB policy benefit over 13 years. A death claim comes in year 7

- So it pays £1,750pm for upto 6 years upon a death claim, afterwards the policy ends

- Like decreasing term life cover, as amount death reduces over the term eg; protect child maintenance costs

- FIB is designed to avoid complications & stress of how best to invest a lump sums for income

- Some Insurers allow FIB life insurance for over 40s to be commuted to lump sum option upon claim

* Whole Life Insurance

- Whole of life insurance is unique in the over 40 Life Insurance marketplace.

- It guarantees it will pay out a lump sum whenever you die or diagnosed terminally ill.

- It has no set or fixed time frame unlike term life insurance.

- Guaranteed Life Insurance over 40 as you are covered even if you live to 450 years old !

- Help toward Final Expenses costs ie; Typically sold via Over 50’s or Over 60’s plans

- Insure against possible Inheritance Tax IHT liabilities

- Cover Life insurance to always payout whenever that maybe

- Continuous No Future Health Issues coverage for life insurance

Life Insurance under 40

Whilst some of you reading this may now be just over 40, there are some of you after Life insurance under 40 (as you haven’t quite reached the big four zero milestone just yet).

But most life insurance for under 40 protection policies are generally all the same. The good news is many Insurers may however offer lower risk levels for obtaining their medical evidence for those after life insurance under 40. eg; You could get £400,000 critical life insurance cover without need for a nurse private medical screening.

* ‘Over 40 Life Insurance No Medical’

A life insurance over 40 no medical is available in the following circumstances.

- Insurers will ask you various health & lifestyle application questions

- But they then won’t ask you to take a full medical exam

- Even if you have some health issues like raised blood pressure or cholesterol

- You are still accepted for life insurance cover immediately

- Also ‘no medical’ here means they do not need to write to your GP rather than request you attend a medical

- The Insurers therefore consider you pose a fair underwritten insurance risk

- Many best life insurance for over 40 uk plans include a guaranteed no medical insurability GIO option

- This means you can increase cover usually upto age 55 if you marry, increasing mortgage or salary

- No medical is also needed if you opt for a convertible or renewable plan

- Likewise, no medical is needed annually if your plans increases by indexation

Guaranteed Life Insurance over 40

Over 40 life insurance no medical plans or guaranteed life insurance over 40 are similar to over 50’s lifecover ‘no medical questions‘ (rather than just no medical) are today few & far between in the UK marketplace.

Is the reason you are looking for this type of plan because you have some serious health issues eg; overweight & after life insurance bmi over 40 or other adverse family health risks. In other words, you think you may pose too high a risk to insure for normal insurance over 40?

Note: Typically any basic no medical questions insurance plans have upto 2 years initial exclusion period and so generally offer much lower levels of life insurance to offset the Insurers risk.

Life Insurance over 45

For some Insurers Life Insurance over 45 means all the same life protection products but now a slightly higher risk levels for getting medical evidence. So, you may now come into their next underwriting insurance ages bracket ie; ‘over 45 to 50’ eg; You could get £275,000 critical life insurance cover without need for a nurse private medical screening.

Also, some budget life insurance providers may wish your term life insurance for over 45 to now end within a certain time frame eg; at age 70. If unsure about which over 45 life insurance, please contact us for broker help.

‘Life Insurance for over 40’ | Broker FAQ

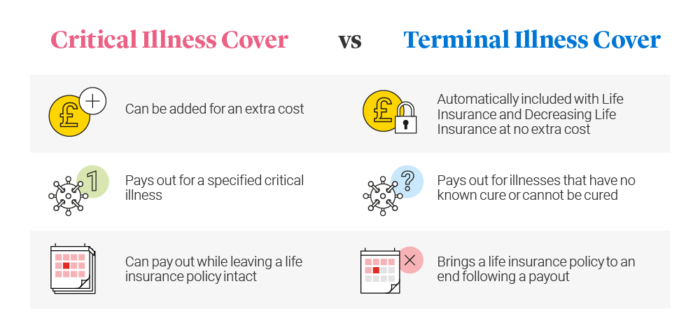

Is Terminal Illness the same as Critical Illness?

- NO is the answer. Terminal Illness on a over 40’s life insurance plan – means you sadly have less than 12 months to live

- Terminal Illness is often included for free as part of your cover life insurance benefits

- Once agreed, the Insurers claim team will then payout the life insurance earlier ‘death claim’ in advance ie; incurable illness

- Critical Illness however is ‘paid for’ underwritten benefit, claimed upon survival & recovery. It often covers a large range of benefits

- Benefits for lifecover and critical illness payouts may include types of cancers, heart disease, stroke, multiple sclerosis, diabetes, parkinsons etc;

What’s Waiver of Premium on Life Insurance?

- Waiver of premium helps protect your policy premiums if off work re accident, sickness or hospitalisation

- Some Insurers may also waiver your premium if off work through pregnancy or redundancy for 6 months

- Premiums are usually waived after deferral period of 4/8/13/26 weeks

- The Insurers then pay your premium until you get back to work or potentially until a claim to plan end

- So it works similar to income protection benefit on the life insurance on over 40 policy

- Many Insurers may charge you extra for this benefit, however for some its standard inclusive

- The cost for this benefit is often small, in relation to help protecting the large amounts of life insurance

Joint | Dual Life vs Single Over 40’s Life Insurance?

- A joint life 1’st death insurance policy may pay out on the death or claim on that 1’st policyholder. Then it ends.

- Joint life insurance 2’nd death policy pays on last death eg; This may usually be used for Inheritance Tax IHT cover

- Single life insurance at 40 plans are setup on the sole life & death of a policyholder

- Some people may often setup a joint life plan to repay a joint mortgage

- Family life Insurance cover may be setup either joint life 1’st death or 2 x single policies or ‘dual life’

What does putting a Life Insurance Into Trust mean?

- Putting your life insurance on over 40 policy into ‘trust’ ensures it should go direct to you nominated beneficiaries via the trustees

- It may also help to avoid probate delays & inheritance tax – by falling outside your estate

- This applies even if you have made a valid will

- Without a suitable trust, the policy could fall back into your estate

- Inheritance tax is currently 40%. So it could be for larger estates, the life insurance payout is then reduced by this amount

- Most Insurers do supply free a good range of generic life insurance trusts, ideal for many client situations

Level or Increasing Insurance?

- Level term policies always stay at that fixed amount & so will the premium

- Increasing cover plans may adjust annually to help offset increasing yearly living costs & rising bills

- The cover increase maybe via retail price index RPI; annual earnings AEI; a fixed amount eg; 5%

- Another benefit of increasing cover life insurance is Insurers may increase without further medical evidence

Covid-19 & ‘Life Insurance Over 40′

- Insurers will ask in the last few months have tested positive or had recent contact with anyone with symptoms

- If so, you may have to await your full recovery and be fully OK before you can re-apply

- Standard rates for over 40 insurance may apply after any self-isolation period & assuming no other health issues

- Any refusal to be vaccinated, will not affect consideration payment of a claim

- Receiving a COVID-19 vaccination or side effects will not impact on your life insurance for 40 year olds

- Should Covid 19 lead to death, Insurers will approach any claim as normal

Which is the Best Life Insurance for over 40 (2023)?

- There is no set answer to this question, as given this type of over 40 life insurance, the devil is really in the detail.

- What type of policy is actually required ie; cover for your Mortgage, Family, Funeral Costs, Inheritance Tax etc ;

- Or if you have health issues, your job or pastimes are all considered high risk then each Insurer may cost this differently

- So the cheapest policy quote isn’t necessarily the best, as it may have age costed annually reviewed increasing premiums

- Ignore advertised Life Insurance with Free Gifts deals, as they generally could be £1,000’s more lifetime expensive

- Likewise the most expensive policy isn’t always the best, it could be unsuitable to your individual case circumstances or budget

Importance of Disclosure & Claims?

All Insurers are in business to protect, insure & payout. Insurance cover is therefore based on your full disclosure at the time you took the original policy out ie; being 100% as honest & accurate as possible. It is not always easy to remember all your historic health details when applying.

The Consumer Insurance Act 2013 says you must not be acting careless, deliberate or reckless when applying. If so, it may not payout ! eg; If you vape, then you must tell them you are still smoking on your over 40s life insurance (even if it may cost the same as having quit smoking cigarettes).

Should you make a claim, your Insurers will send you a claim form for you to complete. Once received back, they will usually contact your GP to confirm any health details. They will then assess if your insurance over 40 claim is valid and cross check if you originally disclosed all the correct details. If you look at most Insurers recent claims payout, you will see that it is Good (but like most Insurers cover life insurance is not 100%).

What if my health lifestyle changes after I have taken the policy out?

Any health or lifestyle changes since, usually does not void your existing life insurance for over 40s, if it wasn’t relevant at that time of initial underwritten insurance application. It maybe the Insurers request GP reports when you originally apply, to check any health details disclosed. Likewise they may not.

So take care to doubly re-check on your life insurance for 40 and over application what you initially disclosed to the Insurers, as this information then stands now and in the future. Please check your original T&C’s.

In conclusion, unsure what’s the best life insurance for a 40 year old? Please get a free online quote or Contact us for broker help.

Article on ‘Over 40 Life Insurance’ by Martyn Spencer Financial Adviser (2026)

For reassurance re health for men & women – we review many of the best Life Insurers selling Life Insurance in UK (inc NI)